Is a stablecoin a new financial system or will it be replaced?

Reprinted from panewslab

03/09/2025·2MAuthor: @DiogenesCasares

Compilation: Vernacular Blockchain

Stablecoins account for two-thirds of on-chain transaction volume, whether it is used for redemption, DeFi transactions, or simple transfer payments. Initially, stablecoins gained attention through Tether, the first widely used stablecoin. The original intention of Tether was to solve the problem that Bitfinex users cannot easily use fiat currency due to bank account restrictions. Bitfinex creates USDTether and promises 1:1 to be backed by USD. Since then, Tether has spread rapidly, and traders use USDT to conduct arbitrage trading between different trading platforms. Compared to traditional bank wire transfers that take several days to complete, Tether transactions can be confirmed in just a few blocks (minutes), making USDT an advantageous payment tool in the crypto market.

However, while stablecoins were originally intended to address specific problems in the cryptocurrency ecosystem, they have long gone beyond their original uses, becoming the core driver of daily capital transfers, and are increasingly used to earn income and facilitate real-world transactions. Currently, the total market value of stablecoins accounts for about 5% of the cryptocurrency market. If we consider companies that manage these stablecoins, or blockchain networks like Tron, which rely mainly on stablecoins usage, the overall market share of stablecoins has reached nearly 8%.

Despite the rapid growth of stablecoins, there is relatively limited content on why stablecoins are so popular. Tens of millions of users are replacing traditional financial systems with stablecoins, but little is known about its true drivers. In addition, there are very few research on platforms and projects that support the development of the stablecoin ecosystem and different user groups. Therefore, this article will explore in-depth why stablecoins are so popular, who are the main players in the stablecoin space, and which user groups are driving this trend, and analyze how stablecoins are gradually becoming the next stage of currency evolution.

1. A brief history of the US dollar

What do you think of when you mention “money”? cash? Dollar? Price tags in supermarkets? Or taxes? In these scenarios, money is essentially a conventional unit of measurement used to measure the value of various different, heterogeneous goods and services.

At first, money was in the form of shells and salt, which then evolved into copper coins, silver coins, gold coins, and today's US dollar/fiat currency.

1) Let's focus on the US dollar

The US dollar (and modern fiat currency, which is issued by the government and not supported by physical assets) has gone through several stages of development. In the United States, the original dollar notes (bills issued by banks) were private. At that time, banks could print money freely, and this model was somewhat similar to Hong Kong's Hong Kong dollar (HKD) system. However, due to many problems with this model, the government eventually intervened and took over the issuance of the US dollar, while passing laws to stipulate that the US dollar is tied to gold.

In 1871, Western Union used telegrams to complete the first wire transfer, achieving a breakthrough in the transfer of funds without moving a large amount of paper money. This innovation greatly improves the efficiency of the financial system because it eliminates the physical limitations of money circulation and makes the entire financial system more efficient.

2) A brief history of the development of the US dollar

1913: The Federal Reserve System was established and began to regulate the issuance and monetary policy of the US dollar.

1971: Nixon terminated the gold standard, the US dollar no longer pegged to gold, and turned into a free floating monetary system.

1950: The world's first credit card was born, opening the era of non-cash payments.

1973: SWIFT (Global Banking Finance and Telecommunications Association) payment network was established to make US dollar transactions faster and global.

1983: The first digital bank account was established at Stanford Federal Credit Union, which started the digitalization process of banks.

1999: PayPal was born, enabling a pure digital payment method without a bank account.

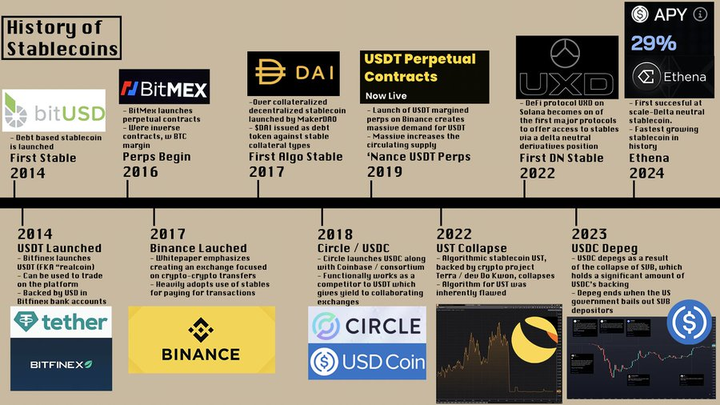

2014: Tether launched the first dollar-backed stablecoin (USDT), laying the foundation for today’s stablecoin market.

All of this development has brought us to the current era of stablecoin.

This short historical review, most importantly, reveals to us the fact that the form of money and the way we use it is always changing.

Nowadays, whether it’s PayPal, cash, Zelle or bank transfer, it’s completely feasible (although if you transfer with a traditional bank, you might get weird eyes thrown). In developing countries, and even in more and more developed countries, this trend also applies to stablecoins.

Personally, I pay my salary with stablecoins, and I used to exchange stablecoins for cash. Now I even prefer to use stablecoins instead of bank accounts to save, and use @HyperliquidX's HLP, AAVE, Morpho, and @StreamDeFi to manage funds.

In our world, traditional financial systems often put heavy burdens on the most vulnerable groups. Capital controls, the monopoly status of banks and high fees have become the norm. In such an environment, stablecoins have become a powerful tool for financial freedom - it not only makes cross-border currency transfer more convenient, but is also gradually used to directly pay for goods and services.

To understand how stablecoins can succeed in such a short time, we must first figure out why stablecoins can beat the traditional financial system.

2. Stablecoin vs. Bank transfer: One city, two stories

The essence of a stablecoin is a token supported by fiat currencies such as the US dollar or the euro.

Many readers who read this article may be from developed countries in North America, Europe or Asia, where financial systems are relatively efficient, smooth and stable. In the United States, there are PayPal and Zelle, in Europe, SEPA, and in Asia, various financial technology companies are emerging one after another, the most well-known of which are Alipay and WeChat Pay.

In these areas, people are used to putting their money in the bank without worrying about the balance in their accounts disappearing the next day or the hyperinflation. Small transfers can usually be completed quickly, and even large amounts of capital flows may take longer, but they are not unbearable. In addition, most businesses force customers to use local banking systems because this is considered safer and more convenient.

However, another part of the world is a completely different reality.

In Argentina, bank deposits have been forcibly misappropriated by the government many times, and their own currency is also one of the worst-performing currencies in history.

In Nigeria, the official exchange rate and the black market exchange rate are seriously disconnected, and it is extremely difficult for funds to enter and exit the country - ironically, this also applies in Argentina.

In the Middle East, bank accounts may be freezed by the government, resulting in many ordinary people (especially people without political backgrounds) not daring to deposit most of their current assets into the bank and can only choose other ways to deposit funds.

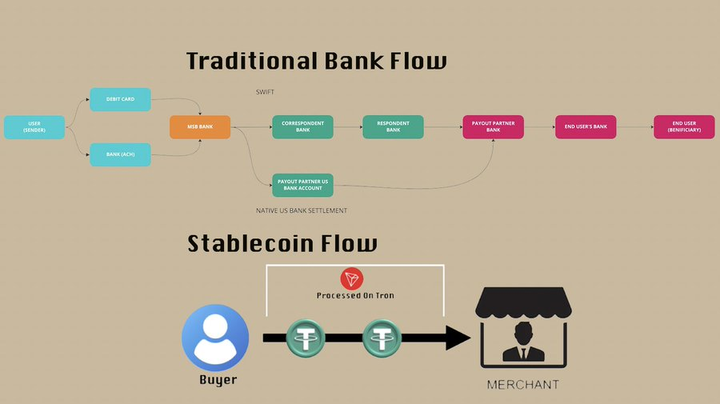

It is not just that there are risks in holding funds, but transferring and remittance are often more difficult. SWIFT (Global Banking Finance and Telecommunications Association) has expensive cross-border transfers and cumbersome processes, and in these countries, most people do not have bank accounts at all for the aforementioned reasons.

As for alternatives like Western Union, although cross-border remittances are able to be completed, they usually charge extremely high handling fees (you can check out their fee calculator). Worse, they tend to settle at official exchange rates, which are usually much higher than the actual market exchange rate, resulting in users taking huge "invisible" fees.

Stablecoins enable people to hold funds outside of the local financial system because they are global in nature and rely on blockchain for transfers rather than local banking servers. This feature stems from their historical background—cryptocurrency trading platforms have faced challenges due to their difficulty in opening bank accounts, handling large-scale deposits and withdrawals, and cross-trading platform transfers.

One of the most famous cases is Japan. Due to the cumbersome bureaucracy and strict capital controls of the Japanese banking system, there has been a long-term arbitrage space between global cryptocurrency prices and Japanese local prices.

In 2017, BN announced in its white paper that its trading platform will only support stablecoin-cryptocurrency trading pairs to speed up settlement. This move directly promoted the transfer of market trading volume to stablecoin trading pairs. In 2019, BN launched the USDT perpetual contract, allowing users to trade margins using USDT instead of BTC, further consolidating the dominance of stablecoins. Today, stablecoins have become recognized as the underlying asset in the cryptocurrency market, and this acceptance is gradually expanding to application scenarios outside of cryptocurrencies.

3. Stablecoin vs. Fintech: Solutions to Speed, Innovation and Global

Financial Problems

If we look at the speed of transactions, innovative design and ability to solve global financial problems, stablecoins are significantly different from Fintech.

So far, the main contribution of fintech is to optimize and beautify existing payment infrastructure rather than revolutionizing its underlying architecture. Essentially, they just add a layer of "paint" to the traditional financial system, but do not solve their inherent inefficiency and complexity. Stablecoins are the most significant change in the global financial system in 50 years.

Fast, reliable and transparent: The transfer speed of stablecoins is far higher than that of traditional banking systems, and it also has on-chain verifiability, making capital flow more efficient.

Low-cost remittances: Compared with traditional payment methods such as bank wire transfers or Western Union, stablecoins almost eliminate high fees (although this also means losing some of the guarantees provided by the traditional financial system).

Competitors for cash and payment processors: Stablecoins can not only replace cash, but also compete with payment processing agencies such as Western Union, while being safer and longer than cash.

Can't be easily damaged or stolen: Stablecoins won't disappear like cash due to floods, fires or thefts and can be exchanged for local currency at any time.

Transaction fees are extremely low: The transfer cost of stablecoins depends on the blockchain network, but is usually less than $2 and is a fixed fee, much lower than the handling fee for traditional payment systems such as Western Union (usually between 0.65% and above 4%).

All this shows that stablecoins are not only dominant in the cryptocurrency field, but are also challenging the foundations of the traditional financial system.

Once stablecoins are widely accepted and gradually mature, they will inevitably fill the gap in the global financial system that traditional financial institutions have not yet covered. As stablecoins continue to become popular, financial services and complex products surrounding them are also growing rapidly.

For example, @MountainUSDM has introduced RWA (real-world asset) gains on multiple platforms in Argentina, while @ethena_labs allows users to profit from exposure-free Delta-neutral transactions without relying on traditional banking systems or trading platforms to host.

Today, the purpose of stablecoins is far beyond simple payment processing or safe-haven preservation, and more and more people are starting to use stablecoins to earn profits, even for local payments. As this trend develops, stablecoins are gradually becoming an important part of global financial planning and are even included in the balance sheet of enterprises.

It is worth noting that many users of stablecoins do not even know that they are using encryption technology - this is the huge breakthrough made in recent years around stablecoin product innovation. Major companies continue to optimize user experience, making the usage of stablecoins more seamless and intuitive, further promoting their global adoption.

4. Companies that are promoting the popularization of stablecoins

The main stablecoin projects are the companies that issue these stablecoins. These include:

USDC issuer @Circle

USDT's issuer @Tether_to

DAI/USDS issuer @SkyEcosystem

PYUSD, jointly launched by @PayPal and @Paxos

Of course, there are many unmentioned stablecoins, but the above are the most important payment uses stablecoins. These companies usually have bank accounts, receive traditional bank wire transfers, and convert these funds into stablecoins to provide them to users.

1) Stablecoin capital operation model

Stablecoin issuers will hold the funds deposited by the user and charge users an extremely low fee (usually 1-10 basis points). Users can transfer these assets at any time, while the issuer earns interest through funds in the bank account (i.e., "floating returns" or "return rates" in the DeFi context).

Trading companies play an important role in this process, responsible for handling the conversion of fiat and stablecoins on a large scale. As more and more trading platforms begin to crack down on users who only use stablecoins to deposit and withdraw funds but do not pay transaction fees, the role of trading companies in this market is becoming increasingly critical.

Trading companies often offer better prices than local trading platforms, further improving the efficiency and competitiveness of stablecoins.

As all major trading companies compete fiercely in this market, they continuously optimize liquidity and services to make stablecoins trading smoother.

Stablecoin issuers earn interest in the process rather than charging users high fees, which is also the core of their business model.

It is worth mentioning that the pattern of @SkyEcosystem (formerly Maker) is different.

SkyEcosystem adopts a hybrid model with its stablecoin USDS backed by a variety of collateral assets, including other currencies reserves.

Users can deposit these collateral assets and lend USDS at a pre-determined interest rate.

They can choose to deposit the "Save Rate Module" (similar to risk-free interest rates), or borrow USDS on platforms such as @MorphoLabs and @Aave, or simply hold USDS.

This model allows users to choose safer gain options or take higher risks for higher returns.

2) User growth of stablecoins: not directly targeted to consumers

Currently, most major stablecoin issuers do not directly target ordinary consumers, but provide stablecoin support indirectly through different financial service companies. This model is similar to MasterCard - it works with banks but does not directly connect to end users.

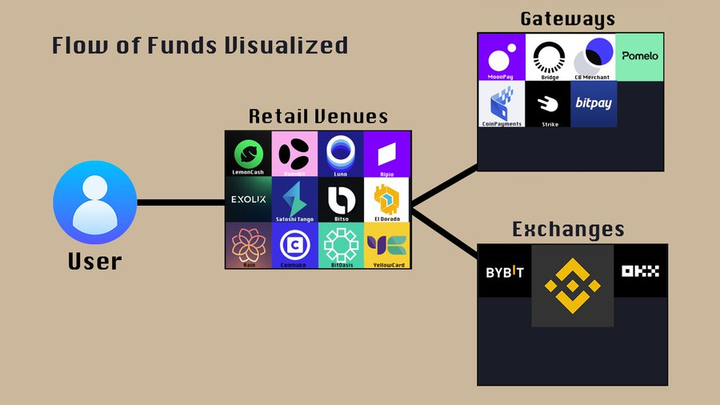

You may rarely hear names like @LemonCash, @Bitso, @Buenbit, @Belo, @Rippio in the crypto community (CT), but they play an important role in the stablecoin trading market. For example:

The above-mentioned Argentina trading platforms alone have more than 20 million KYC certified users, almost half of the number of Coinbase users, while the population of Argentina is only 1/7 of that of the United States.

Lemon Cash traded $5 billion in 2023, with a large proportion of which are stablecoins-stablecoin trading, or ARS (Argentine Peso)-stablecoin trading.

These platforms act as an entrance to most non-peer to-peer stablecoin transactions, and they themselves also have a large amount of crypto trading volume and stablecoin deposits. However, except for Rippio, most platforms do not have their own order book, but rely on the order routing system to complete transactions.

This model is very similar to Robinhood – Robinhood is not a real trading platform, but is priced through liquidity providers (Market Makers). I call these platforms the **"Retail Venues" because their focus is on optimizing user experience and retail products, rather than building their own trading platform infrastructure.

Robinhood's API does not allow high-frequency traders or market makers to use because its target users are not professional traders, but ordinary investors.

Similarly, BuenBit and Lemon will not attract market makers, their main target users are ordinary consumers, rather than professional trading companies or high-frequency traders.

Under this model, the application of stablecoins is entering the global financial system in a low-cost and efficient way, not only affecting the crypto market, but also changing the landscape of the traditional payment and remittance industry.

Next, let’s look at the blockchain where stablecoins actually operate, that is, where stablecoins transfers, transaction records and balances are stored. Currently, the main chains of stablecoin trading include:

@justinsuntron @trondao (Tron)

@binance's BN Smart Chain (BSC)

@solana (Solana)

@0xPolygon (Polygon)

The main purpose of these chains is value transfer and does not necessarily involve DeFi interaction or acquisition of benefits.

Although Ethereum still leads TVL (total locked value), it is not attractive for most stablecoin transactions due to the high transaction costs. Data shows:

92% of USDT transactions occur on the Tron chain.

About 96% of the transaction volume on the Tron network are related to stablecoins.

In contrast, stablecoin transactions still account for a high proportion on Ethereum, but only 70%.

In addition, some new blockchains are trying to handle stablecoin transactions efficiently and at low cost, and one of the notable ones is LaChain.

LaChain is operated by an alliance of Ripio, Num Finance, SenseiNode, Cedalio, Buenbit and FoxBit, mainly targeting users and platforms in Latin America.

This also shows that as the stablecoin market continues to mature, the ecosystem is becoming more complex and diversified.

5. The evolution of stablecoin payment: from cross-border remittance to

local payment

Stablecoins have become the main tool for cross-border remittances, but today, they are increasingly used for local payments.

This involves cryptocurrency payment gateways and payment portals, i.e.:

Convert stablecoins to fiat currency, or

Merchants are allowed to accept payments directly in fiat currency.

For example, a merchant can "accept" crypto payments, but in reality, the cryptocurrency of the transaction is immediately converted into US dollars and settled to the merchant's bank account. Of course, merchants can also directly accept stablecoin payments.

But because there is still a certain friction in the redemption of stablecoins (whether it is time or handling fee costs), there are also a large number of companies working to optimize this process in the market, and the solutions they provide varying from simple and efficient to complex and comprehensive.

Pomelo (https://www.pomelogroup.com/): A platform that supports cryptocurrency debit card payment, allowing users to directly spend with stablecoins.

@zcabrams' Bridge: Provides convenient conversion between stablecoins, between different chains, and between fiat currencies, greatly reducing the friction costs between merchants and payment platforms.

@stripe even acquired Bridge to improve the efficiency of its own payment system.

At present, payment gateways like Bridge are mainly used in scenarios where merchants have not directly accepted USDC or USDT. They will first help users complete the conversion and then charge a certain fee.

With the popularity of stablecoin payments and its lower costs compared to traditional bank cards and banking systems, the utilization rate of stablecoin-stablecoin transactions will continue to increase. In the future, more and more merchants will directly accept stablecoin payments to optimize unit economic benefits and promote stablecoin to build a payment system in the post-bank era.

6. Financialization of stablecoins: How to "add value" of stablecoins

In addition to payments and remittances, more and more companies are exploring how to put stablecoins into use to improve their asset utilization, such as:

Lemon Cash: Provides @aave deposit function, allowing users to deposit funds to earn profits.

@MountainUSDM's USDM: allows stablecoin holders to earn income and has been integrated into trading platforms and payment services in multiple Latin American regions.

Many trading and retail financial platforms regard Stablecoin Yield as a stable source of income, hoping to balance the revenue fluctuations brought about by the market cycle.

Traditional trading platforms rely heavily on transaction fees, which leads their revenue to surge in bull markets, but plummet orders of magnitude in bear markets.

By providing stablecoin deposit income and related services, these platforms can obtain more stable revenue and reduce the impact of market volatility on their profitability.

7. What is the future development of stablecoins?

The non-crypto use of stablecoins: expansion of international transfers and payments

The main non-cryptocurrency application of stablecoins is international transfers and is now increasingly used for payments. However, as stablecoins infrastructure continues to improve and gradually become popular, they may also be used for savings, especially in developing countries, this trend has begun to emerge.

A few weeks ago, @tarunchitra told me a story: In Georgia, a convenience store owner would charge customers’ deposits of Georgian Lari (GEL), exchange them for USDT and earn interest, while recording customer balances with a simple paper ledger and drawing a certain handling fee from the interest. In this store, customers can also use the Trust Wallet QR code to pay. It is worth noting that Georgia's banking system is relatively healthy, but this alternative financial model still develops here.

In Argentina, according to the Financial Times (FT), citizens have estimated that the total amount of USD cash held by citizens has exceeded US$200 billion, and these funds are all outside the traditional financial system. If even half of the funds enter the on-chain or crypto ecosystem, the DeFi market size will double and the total market value of stablecoins will increase by about 50% - and this is just the potential of a country. Similar situations also exist in countries such as China, Indonesia, Nigeria, South Africa and India, where the informal economies are huge or there is a certain degree of distrust of the banking system.

More potential use cases of stablecoins As the use of stablecoins increases, its application scenarios are also expanding.

Credit loan: Currently, stablecoins are mainly used for fully mortgaged credit loans, which is extremely rare in the global credit market. However, with new tools introduced by institutions such as Coinbase, KYC certification data may be used in the future to expand the credit market and may introduce a negative credit record mechanism (i.e., unpaid loans will affect credit scores).

Earnings Allocation: Stablecoin Issuers are gradually allowing earnings to be "passed" to holders, for example:

USDC provides 4.7% annualized revenue

Ethena's USDe has dynamic yields, usually over 10%

Cross-fiat currency transactions: Currently, many transactions are beginning to be conducted in a "double-layer conversion" way—for example,

A transaction is first converted into a US dollar stablecoin by local currency, and then

Then exchange it for the target currency (such as Argentine peso or Nigerian naira).

This approach means that users will have to pay two handling fees, but as blockchain technology matures, it may be directly exchanged into the target currency in the future to reduce costs.

As more capital flows into stablecoins, the types of on-chain financial products will be further enriched, making the application of cryptocurrencies more mainstream in daily life.

8. Challenges facing stablecoins

When discussing the future of stablecoins, we also need to face up to some overlooked issues.

- Stablecoins rely on the banking system

Currently, almost all stablecoins rely on bank accounts as their support assets.

But the banking system itself is not absolutely safe, for example:

The USDC briefly deaned due to the banking bank in 2023 due to the collapse of Silicon Valley Bank (SVB), suggesting that even the most trusted stablecoins may face risks from the banking system.

- Stablecoins are widely used to circumvent capital controls and money laundering

If you agree that stablecoins are used to bypass capital controls and evade local currency devaluation, you have actually admitted the fact that under the local legal framework, such behavior may be classified as money laundering.

This is an open secret, but its legal and moral implications are still underexamined.

- The problem of freezing and inability to issue stablecoins

Currently, neither Circle (USDC) nor Tether (USDT) are allowed to reissue stablecoins.

If a user's funds are frozen for legal reasons (such as a crime or found to be stolen money), then the assets will not be returned to the victim, even if the latter holds the court's ruling documents.

This approach is very controversial on the moral level and is even difficult to maintain in the long run.

- Government regulatory pressure & CBDC replacement risk

Governments may demand strengthen regulation of stablecoins to become “sealable”.

In the long run, central bank digital currency (CBDC) may become an official alternative to stablecoins.

This topic covers a wide range and I will discuss it in detail in subsequent articles.

9. A truly decentralized stablecoin may be the solution to the future

In the next few years, government regulatory pressure on stablecoins will promote the development of truly decentralized, privacy-protected stablecoins.

These stablecoins will not be unilaterally frozen or seized by the government and will be completely decentralized.

This could lead to a new financial technology race, and the development of stablecoins could also evolve from regulated financial instruments to truly decentralized currencies.

Of course, this also means a new compliance challenge.