Behind Stablecoins: Why Washington suddenly has a special liking for the US dollar stablecoin

Reprinted from jinse

06/04/2025·13DAuthor: Sumanth Neppalli, author of Decentralised.co; Translation: Golden Finance xiaozou

In July 1944, representatives from 44 allies gathered in the rural ski town of Bretton Woods, New Hampshire to redesign the global monetary system. They peg the currencies of various countries to the US dollar, while the US pegs the US dollar to gold. This system designed by British economist Keynes opened an era of stable exchange rate and frictionless trade.

Let's imagine that summit as a GitHub project: the White House forked the code base, the Treasury Secretary submitted a pull request, and the Treasury Secretary quickly clicked and merged, hard-coded the US dollar into every future trade cycle. Stablecoins are the merged commit in today's digital age - while the rest of the world is still debugging their own code bases to try to build a future without dollars.

Within 72 hours after Trump returned to the Oval Office of the White House, he signed an executive order containing a directive that sounds more like a crypto-tweet (CT) fanfiction than fiscal policy: “ Promote and protect the sovereignty of the dollar, including through globally legal, dollar-backed stablecoins. ”

Congress then introduced the GENIUS Act (Innovation Act for Guiding and Establishing the U.S. Stablecoin National Innovation Act)—the first bill to set basic rules for the stablecoin framework and encourage global payments with stablecoin.

The bill has been submitted to the Senate for consideration through debate and may vote this month. Staff believe that the Democratic coalition's recommendations have been included in the latest draft and the bill is expected to be passed.

But why did Washington suddenly have a special liking for stablecoins? Is this just a political show, or is there a deeper strategic layout hidden behind it?

1. Why overseas demand remains vital

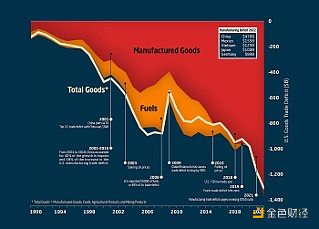

Since the 1990s, the United States has outsourced manufacturing to China, Japan, Germany and Gulf countries, with each batch of imported goods being paid in newly issued US dollars. As imports exceed exports for a long time, the United States continues to maintain a huge trade deficit. The trade deficit is the difference between a country's total import and export.

These dollars put exporting countries in a dilemma: converting the dollar into its own currency will push up the exchange rate, weaken product competitiveness and damage their exports. Therefore, central banks of various countries chose to absorb the US dollar and switch to US Treasury bonds to realize capital circulation without disrupting the foreign exchange market. This move not only yields Treasury bonds, but also has a credit risk that is almost the same as holding idle US dollars.

This mechanism forms a cycle of self-reinforcement: earn US dollars from exports to the United States → invest in US bonds to obtain interest → maintain the weakness of the local currency to continuously expand exports. This "supplier financing cycle" formed with exporters contributed about a quarter of the US $36 trillion in debt, locking in key advantages. If the cycle is broken through a long-term trade war, the cheapest financing channels in the United States will gradually dry up.

Deficit financing mechanism: U.S. government spending continues to exceed tax revenue, forming a structural budget deficit. Share the deficit pressure by selling treasury bonds overseas: short-term treasury bonds mature within one year, and long-term treasury bonds reach 20-30 years.

Low interest rate effect: High demand for Treasury bonds drives down yields (interest rates). When major buyers such as China push up the price of Treasury bonds, yields drop, thereby reducing financing costs for governments, businesses and consumers. This low-cost funding not only maintains economic growth but also supports expansionary fiscal policies.

The cornerstone of the dollar 's hegemony: The status of the dollar's reserve currency depends on global confidence in US assets. Foreign holdings of U.S. bonds symbolize trust in the U.S. economy and ensure that the U.S. dollar maintains its dominance in international trade, oil pricing and foreign exchange reserves. This privilege allows the United States to raise funds at extremely low costs and exert economic influence around the world.

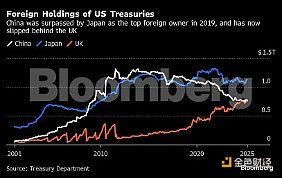

If this demand is lost, the United States will face soaring financing costs, depreciation of the dollar's exchange rate and a recession of geopolitical influence. Crisis warning has already emerged. When Warren Buffett stepped down, he admitted that he was most worried about the imminent dollar crisis. The United States has lost the AAA credit rating of the three major rating agencies for the first time in a century - this is the "gold certification" of the bond market, which means that the debt security rating has reached its peak. After the downgrade, the U.S. Treasury Department had to raise yields to attract buyers, and interest expenses would also rise as national debt continues to soar.

If traditional buyers start to withdraw from the Treasury bond market, who will digest the newly issued trillions of dollars of debt? Washington's bet is that regulated, fully reserved stablecoins will open up new channels. The GENIUS Act forces stablecoin issuers to buy short-term government bonds, which explains why the government is open to the digital dollar while making tough trade statements.

2. The revelation of the Eurodollar system

Such financial innovations are not new to the United States. The $1.7 trillion Eurodollar system has also gone through a process from full boycott to full acceptance. The Euro dollar refers to the dollar deposits deposited in overseas banks (mainly in Europe) and is not subject to U.S. bank regulation.

The Euro dollar was born in the 1950s, when the Soviet Union deposited the dollar into European banks to avoid US jurisdiction. By 1970, its market size had reached US$50 billion, a 50-fold increase in ten years. The United States was initially skeptical, and French Treasury Secretary Destin once called it a "hydra monster." After the 1973 oil crisis, these concerns were temporarily put on hold when OPEC actions quadrupled global oil trade in months - the world needs the dollar as a medium of stable trade.

The Euro dollar system strengthens the United States' ability to project non- force influence. As international trade and the Bretton Woods system consolidate the dollar hegemony, the system continues to expand. Although EuroDollar is only used for foreign entities payments, all transactions are subject to settlement by Bank of America through a global network of agency banking.

This creates a strong leverage for U.S. national security goals: officials can not only block transactions within the United States, but also kick bad actors out of the global dollar system. As the United States acts as a clearing center, it can track the flow of funds and impose financial sanctions on the country.

3. Stablecoin: Digital upgrade of US dollar

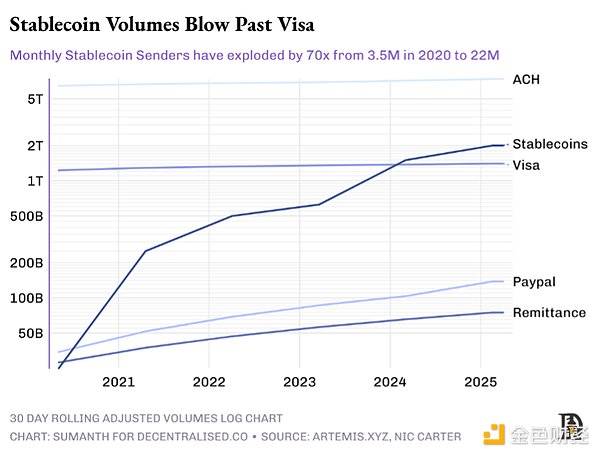

Stablecoins are contemporary Euro Dollars equipped with open blockchain browsers. The US dollar is no longer stored in London vaults, but is "tokenized" through blockchain. This convenience brings true scale: the on- chain US dollar token settlement amount will reach US$15 trillion in 2024, slightly exceeding the Visa network. Of the US$245 billion stablecoins currently in circulation, 90% are fully collateralized US dollar stablecoins.

As investors want to lock in returns and avoid market cyclical fluctuations, demand for stablecoins is increasing day by day. Unlike cryptocurrencies’ fierce market cycles, stablecoin activity continues to grow, indicating that its use is far beyond the scope of transactions.

The earliest demand came in 2014, when Chinese cryptocurrency exchanges needed non-bank dollar settlement solutions. They chose Realcoin, a US dollar token based on the Bitcoin Omni protocol (later renamed Tether). Tether initially conducted fiat currency channel connections through the Taiwan Bank network until Wells Fargo terminated its agency relationship with these banks due to regulatory pressure. In 2021, the U.S. Commodity Futures Trading Commission (CFTC) fined Tether $41 million for failing to fully collateral on the grounds of false reserves.

Tether's operating model is a classic banking method: absorb deposits → invest in floating deposits → earn interest rate spreads. It converts about 80% of its issuance reserves into U.S. Treasury bonds, and with a short-term Treasury yield of 5%, the annual income of $120 billion in holdings can reach $6 billion. Tether achieved a net profit of US$13 billion in 2024, while Goldman Sachs achieved a net profit of US$14.28 billion during the same period - but the former had only 100 employees (average profit of US$130 million), while the latter had 46,000 employees (average US$310,000).

Contenders try to build trust through transparency. Circle releases USDC audit reports every month, listing the casting and redemption records in detail. Even so, the industry still relies on issuer credit endorsement. The Silicon Valley bank crash in March 2023 caused Circle's $3.3 billion reserves to be trapped, and USDC fell to $0.88 for a time, and it was not until the Federal Reserve intervened to provide a bottom line.

Washington is setting up a system of rules. The GENIUS Act clearly requires:

100% reserves must be high-quality current assets such as treasury bonds/reverse repurchases (HQLA);

Real-time audit verification is achieved through licensed oracles;

Regulatory interface: issuer-level freezing function, FATF rules compliance;

Compliant stablecoins can be supported by the Fed's main account and reverse repurchase liquidity.

A graphic designer in Berlin now needs neither a US account nor a German bank or SWIFT file to hold US dollars—as long as Europe does not enforce digital euros, you can take a selfie with a KYC in Gmail account. Funds are flowing from bank ledgers to wallet applications, and the companies that control these applications will be like global banks without branches.

If the bill comes into effect, there will be a choice in the existing issuance: either register in the United States for quarterly audits, anti- money laundering reviews and reserve certificates, or watch the US trading platform turn to compliant tokens. The majority of USDC collateral has been placed in the Circle of SEC's regulatory monetary funds, which obviously occupies a better position.

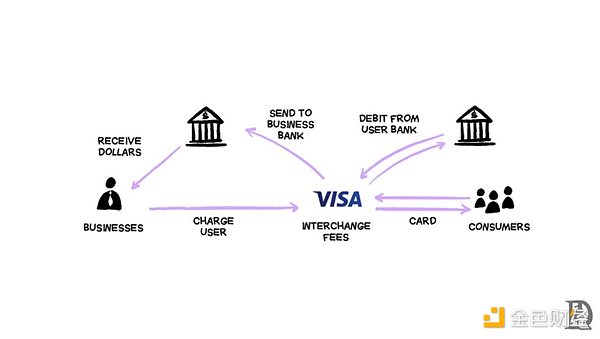

But Circle will not enjoy this blue ocean alone. Technology giants and Wall Street have every reason to join the market - imagine Apple Pay launching "iDollars": you can earn profits by rechargeing $1,000 and spending in all scenarios that support contactless payments. The yield of idle funds is far beyond the existing card swipe fee, and it completely bypasses traditional middlemen. This may be the reason why Apple terminated its cooperation with Goldman Sachs credit card: When payments are completed in on-chain USD, the original 3% transaction fee will be reduced to the blockchain network fee denominated by points.

Large banks such as Bank of America, Citigroup, JPMorgan Chase and Wells Fargo have begun exploring joint issuance of stablecoins. The GENIUS Act prohibits issuance from allocating interest income to users, which has given banking lobby groups a sigh of relief. This model is essentially a super cheap checking account: instant, global and never-stop.

It is no surprise that the hasty layout of traditional payment giants: Mastercard and Visa have launched stablecoin settlement networks, PayPal has issued its own stablecoins, and Stripe has completed the largest crypto acquisition to date (acquisition of Bridge) this year. They know that change is coming.

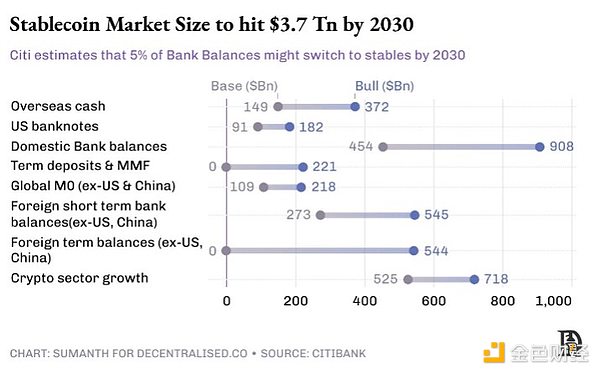

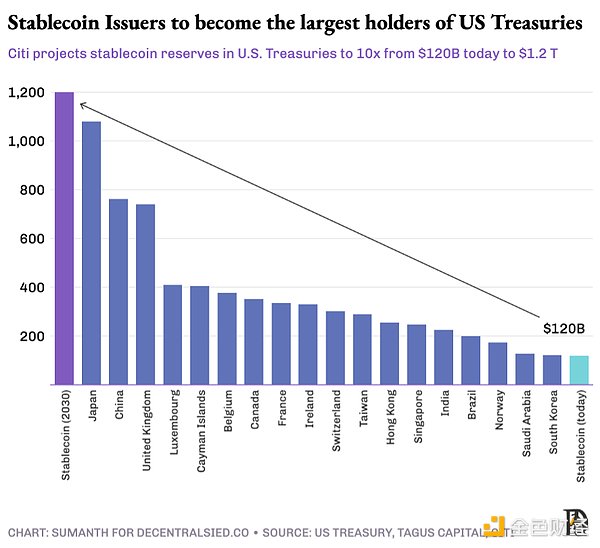

Washington is also aware of it. Citibank predicts that the stablecoin market size will grow six times to $1.6 trillion in 2030 under the benchmark scenario. Research by the US Treasury Department shows that the number may exceed $2 trillion in 2028. If the GENIUS Act mandates 80% of reserves to allocate Treasury bonds, the "stable US dollar" will replace China and Japan as the largest holders of US bonds.

4. Assets are queued up

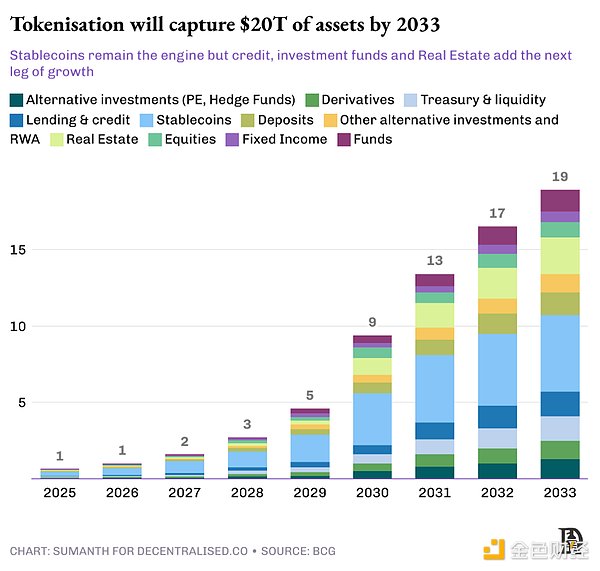

With the popularity of "dollar stablecoins", they will become liquidity that drives the entire token economy. Once cash is tokenized, people will perform off-chain routine operations at the speed of the Internet (rather than banking): savings, lending, collateral. These never-ending liquidity will continue to look for the next tokenization goal, bringing more "real-world assets" (RWA) into blockchain and giving equal advantages.

24/7 All-weather settlement : The traditional T+2 settlement cycle will be completely outdated, and blockchain verifiers can confirm transactions within minutes (rather than days). For example, Singapore traders can purchase tokenized New York apartments at 6pm local time and get ownership confirmation before dinner.

Programmability : Smart contracts embed behavioral logic directly into assets. This makes it possible to make complex financial operations: coupon payment, distribution rights, and asset-level compliance parameter settings can be automatically executed.

Composability : Tokenized Treasury bonds can be used as collateral for loans, and can also automatically distribute interest income between multiple holders. An expensive beachfront villa can be split into 50 interests and rented to hotel operators that manage reservations through Airbnb.

Transparency : The 2008 financial crisis stems in part from opacity in the derivatives market. Regulators can now monitor on-chain mortgage rates in real time, track systemic risks, and observe market dynamics without waiting for quarterly reports.

The main obstacle is regulation. The protection mechanisms of traditional exchanges are all gained by painful lessons, and investors know what kind of protection they can obtain. Taking "Black Monday" in 1987 as an example: The Dow Jones Industrial Average plummeted 22% in a single day, only because price fluctuations triggered the automatic selling of the program, triggering a chain reaction. The SEC's solution is a circuit breaker mechanism - suspending trading allows investors to reassess the situation. Now the New York Stock Exchange stipulates that a decline of 7% will be suspended for 15 minutes.

Asset tokenization is not technically difficult, and the issuer only needs to guarantee the actual asset rights corresponding to the token. The real challenge is to ensure that the underlying system can enforce all offline applicable rules: this includes wallet-level whitelists, national identity verification, cross-border KYC/AML, citizen holding caps, real-time sanctions screening and other functions that must be written into code.

The European Crypto Asset Market Supervision Act (MiCA) provides a complete regulatory framework for digital assets, while the Singapore Payment Services Act is the starting point for Asia. However, the global regulatory landscape is still fragmented.

This process is almost bound to be carried out in waves. The first phase will give priority to high-liquid and low-risk financial instruments, such as money market funds and short-term corporate bonds. The operational benefits brought by instant settlement are immediate and the compliance process is relatively simple.

The second stage will move towards the high-end risk-return curve, covering high-yield varieties such as private equity credit, structured financial products and long-term bonds. The value of this stage is not only in improving efficiency, but also in releasing liquidity and composability.

The third phase will achieve a qualitative leap and expand to illiquid asset classes: private equity, hedge funds, infrastructure and real estate mortgage debt. To achieve this goal, it is necessary to achieve universal recognition of tokenized assets as collateral and to establish a cross-industry technology stack that can serve these assets. Banks and financial institutions need to provide credit while escrowing these real-world assets (RWAs) as collateral.

Although the pace of chain-up of different asset classes varies, the development direction is already clear. Each wave of new "stable dollar" liquidity is pushing the token economy to a higher stage.

(1) Stablecoin pattern

The US dollar-anchored token market is showing a duopoly pattern, with Tether (USDT) and Circle (USDC) accounting for a total of 82% of the market share. Both are fiat-collateralized stablecoins – the euro stablecoin operates the same principle, supporting each token in circulation by storing the euro in the bank.

In addition to the fiat currency model, developers are exploring two experimental solutions to try to achieve decentralized anchoring without relying on off-chain custodians:

Crypto Asset Collateral Stablecoins: Use other cryptocurrencies as reserves, usually over-collateralized to resist price fluctuations. MakerDAO is the banner of the field, with $6 billion in DAI issued. After experiencing the bear market in 2022, Maker quietly converted more than half of the collateral into tokenized treasury bonds and short-term bonds, which not only smoothed ETH volatility but also obtained returns. Currently, this part of the allocation contributes about 50% of the agreement's revenue.

Algorithmic stablecoins: This type of stablecoins does not rely on any collateral, but maintains anchoring through an algorithmic minting-destruction mechanism. Terra's stablecoin UST once reached a market capitalization of US$20 billion, but it caused a run due to a collapse in confidence in the event of deaning. Although new projects such as Ethena will reach $5 billion through innovative models, it will take time for the field to gain wide recognition.

If Washington only grants the full fiat-collateralized stablecoin "qualified stablecoin" certification, other types may be forced to abandon the "dollar" logo in their names to comply with regulation. The fate of algorithmic stablecoins is still unclear - the GENIUS Act requires the Ministry of Finance to conduct a one-year study of these agreements before making a final decision.

(2) Money market tools

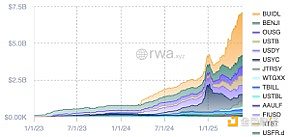

Money market tools cover high-liquidity short-term assets such as treasury bonds, cash and repurchase agreements. On-chain funds achieve "tokenization" by encapsulating ownership stakes into ERC-20 or SPL tokens. This carrier supports 7×24-hour redemption, automatic income distribution, seamless payment docking and convenient collateral management.

Asset management companies still retain the original compliance framework (anti-money laundering/identity verification, qualified investor restrictions), but the settlement time has been reduced from several days to minutes.

BlackRock's USD Institutional Digital Liquidity Fund (BUIDL) is a market leader. The agency appointed SEC-registered transfer agency Securitize to handle KYC access, token minting/destruction, FATCA/CRS tax compliance reporting and shareholder roster maintenance. Investors need at least $5 million of investable assets to qualify, but once they are on the whitelist, they can subscribe, redeem or transfer tokens 24/7 - a flexibility that traditional money market funds cannot provide.

BUIDL's asset management scale has grown to about US$2.5 billion, distributed among more than 70 whitelist holders on five blockchains. About 80% of the funds are allocated to short-term treasury bonds (mainly 1-3 months term), 10% is invested in longer-term treasury bonds, and the remaining part remains in cash positions.

Products such as Ondo (OUSG) operate as an investment management pool, allocating funds to the tokenized money market fund portfolio of institutions such as BlackRock, Franklin Templeton, and WisdomTree, and providing free deposit and exit channels with stablecoins.

Although the scale of $10 billion is insignificant in the face of the $26 trillion treasury bond market, its symbolic significance is extremely important: Wall Street’s top asset management institutions are choosing public chains as distribution channels.

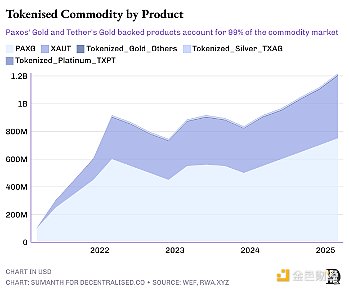

(3) Commodities

The tokenization of hard assets is driving these markets to transform into all-weather, click-to-trade platforms. Paxos Gold (PAXG) and Tether Gold (XAUT) allow anyone to buy a tokenized share of gold bars; Venezuela's 1 PETRO anchors 1 barrel of crude oil; small pilot projects have linked token supply to soybeans, corn and even carbon credits.

The current model still relies on traditional infrastructure: gold bars are stored in vaults, crude oil is stored in oil tank areas, and auditing agencies sign reserve reports on a monthly basis. This custody bottleneck creates a concentrated risk, and physical redemption is often difficult to achieve.

Tokenization not only realizes the ownership of assets, but also makes traditional illiquid physical assets easy to collateral and financing. The scale of this field has reached US$145 billion (almost all endorsed by gold), and compared with the scale of the physical gold market of US$5 trillion, the development space is self-evident.

(4) Lending and Credit

DeFi lending initially appeared in the form of over-collateralized cryptocurrency loans. Users can only lend $100 if they pledge ETH or BTC worth $150, and their operating model is similar to gold mortgage loans. This type of user wants to hold digital assets for a long time to appreciate, and at the same time, they need to pay the bills in liquidity or open new positions. Currently, the loan scale of Aave platform is about US$17 billion, accounting for nearly 65% of the DeFi lending market.

Traditional credit markets are dominated by banks, which underwrite risks through decades of proven risk models and strictly regulated capital buffers. As an emerging asset category, private equity credit has developed in parallel with traditional credit to a global management scale of US$3 trillion. Companies no longer rely solely on banks, but raise funds by issuing high- risk, high-yield loans, which is quite attractive to institutional lenders such as private equity funds and asset management institutions that pursue higher returns.

Introducing this field to the chain can expand the lender group and increase transparency. Smart contracts can realize full-cycle automation of loans: fund issuance and interest collection, while ensuring that liquidation trigger conditions are clearly visible on the chain.

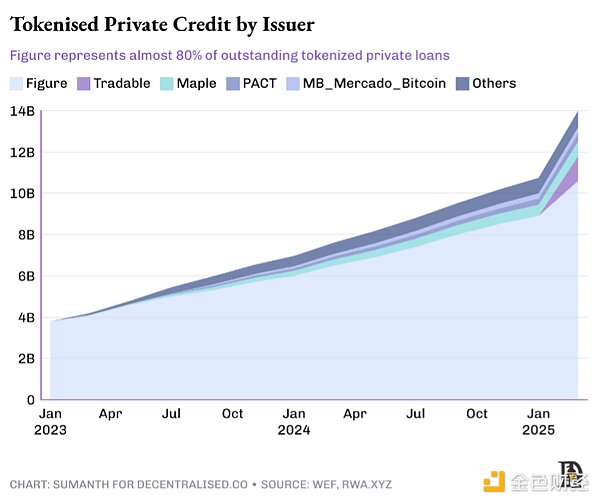

Two models of on-chain private equity credit:

" Retail " direct loan : Platforms such as Figure tokenize home renovation loans and sell spin-off notes to wallets that pursue profits around the world, which can be called the debt version of Kickstarter. Homeowners obtain lower financing costs by splitting the loan into small shares, retail depositors charge coupons on a monthly basis, and the agreement automatically handles the repayment process.

Pyse and Glow package solar projects, tokenize power purchase protocols, and handle the entire process from panel installation to meter readings. Investors can directly obtain 15-20% annualized returns from their monthly electricity bills by simply enjoying their success.

Institutional liquidity pool: Private equity credit counters are presented in a transparent form on-chain form. Agreements such as Maple, Goldfinch and Centrifuge package borrower needs into on-chain credit pools managed by professional underwriters. Depositors are mainly qualified investors, DAOs and family offices who can earn both floating returns (7-12%) and track asset performance on public ledgers.

These agreements are committed to reducing operating costs, allowing underwriters to go on the chain for due diligence and complete loans within 24 hours. Qiro adopts the underwriter network model, each underwriter uses an independent credit model, and the analysis work will receive corresponding rewards. Due to the high risk of default, the growth rate in this field is lower than that of mortgage loans. When a breach occurs, the agreement cannot use traditional collection methods such as court orders, and traditional collection agencies must be used, resulting in an increase in disposal costs.

As underwriters, auditors and collection agencies continue to go on the chain, market operating costs will continue to decline, and lenders' fund pool will also be significantly deepened.

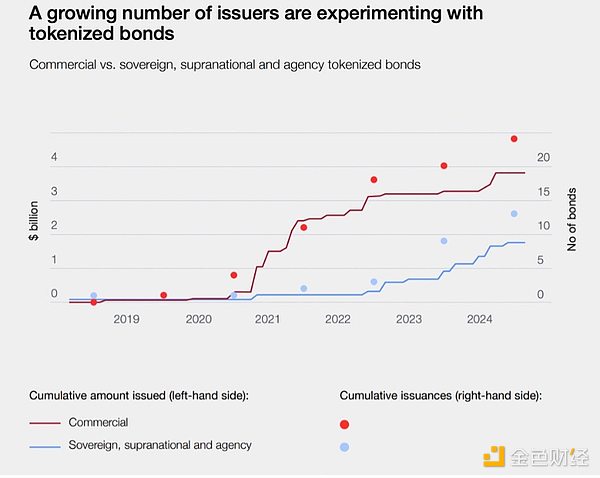

(5) Tokenized bonds

Bonds and loans are both debt instruments, but there are differences in structure, degree of standardization and issuance and transaction methods. Loans are one-to-one agreements, while bonds are one-to-many financing tools. Bonds are in a fixed format—for example, bonds with a face rate of 5% and a 10-year maturity are easier to rated and traded in the secondary market. As a public tool regulated by markets, bonds are usually rated by institutions such as Moody's.

Bonds are often used to meet large-scale, long-term capital needs. Governments, utilities and blue chip companies raise budget funds, build factories or obtain bridge loans by issuing bonds. Investors charge interest regularly and recover their principal upon maturity. This asset class has an astonishing scale: it is nominal value of approximately US$140 trillion as of 2023, equivalent to 1.5 times the total global stock market value.

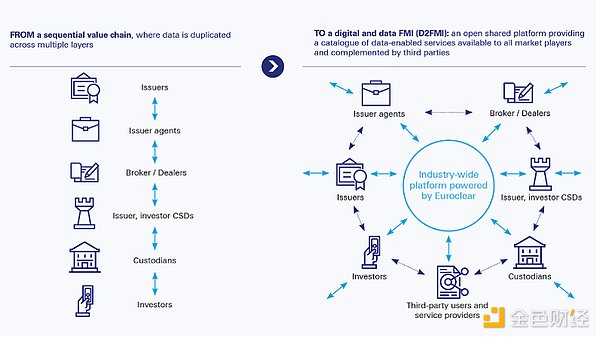

The current market is still operating on outdated infrastructure designed in the 1970s. Clearing agencies such as the European Clearing House (Euroclear) and the American Depositary Trust and Clearing Company (DTCC) need to be transferred through multiple custodians, resulting in transaction delays and forming a T+2 settlement system. Smart contract bonds can achieve atomic settlement in seconds, and automatically pay dividends to thousands of wallets at the same time, with built-in compliance logic and access to the global liquidity pool.

Each bond issuance can save 40-60 basis points of operating costs, and the financial supervisor can also obtain a 24-hour secondary market without paying for exchange listing fees. As the core European settlement and custody channel, Euroclear hosts 40 trillion euros of assets, connecting more than 2,000 institutions to 50 markets. The agency is developing a blockchain-based issuer-broker-custodial settlement platform aimed at eliminating duplicate operations, reducing risks, and providing customers with real-time digital workflows.

Companies such as Siemens and UBS have issued on-chain bonds as ECB pilot projects. The Japanese government is also working with Nomura Securities to experiment with bonds on-chain plans.

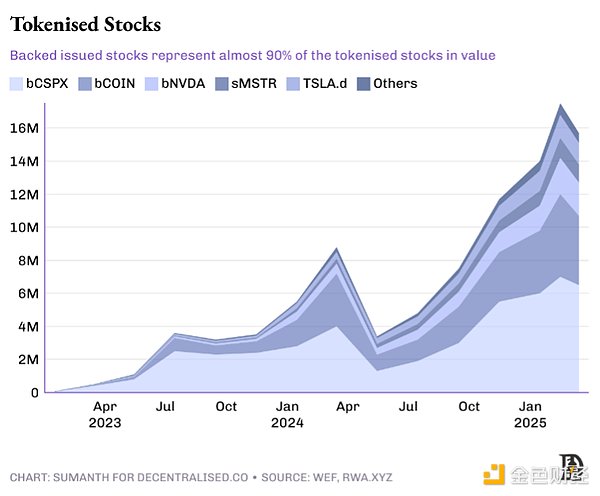

(6) Stock Market

This field naturally has development potential - the stock market itself has already participated by a large number of retail investors, and tokenization can create an "Internet capital market" that operates around the clock.

Regulatory barriers are the main bottleneck. The current custody and settlement rules of the US Securities and Exchange Commission (SEC) were formulated in the pre-blockchain era, and intermediaries were mandatory to participate and maintain the T+2 settlement cycle.

This situation is beginning to loosen. Solana has applied to the SEC for approval of the on-chain stock issuance plan, which includes KYC verification, investor education process, broker custody requirements and instant settlement functions. Robinhood filed an application right after that, claiming to treat tokens representing U.S. Treasury divestiture certificates or Tesla single shares as securities themselves, rather than synthetic derivatives.

The demand in overseas markets is stronger. Thanks to loose controls, foreign investors have held about $19 trillion in U.S. stocks. The traditional path is to invest through local brokerages such as eTrade (need to cooperate with US financial institutions and pay high foreign exchange spreads). Startups such as Backed are offering alternatives—synthesis assets. Backed has purchased target stocks of equivalent value in the US market and has completed a $16 million business. Kraken recently cooperated with it to provide U.S. stock trading services to non-US traders.

(7) Real estate and alternative assets

Real estate is the most severely bound asset class by paper certificates. Each title deed is deposited in the government registration office, and each mortgage document is sealed in the bank vault. Large-scale tokenization is difficult to achieve before the registration agency accepts the hash value as proof of statutory ownership. Currently, only about $2 billion of the 400 trillion US dollars of real estate in the world have been put on the chain.

The UAE is one of the regions leading the change, with $3 billion worth of property deeds completed on-chain registration. In the US market, real estate technology companies such as RealT and Lofty AI have achieved tokenization of residential assets of more than $100 million, and rental income flows directly to digital wallets.

5. Funds are eager to flow

Crypunks view "dollar stablecoins" as a regression to the bank custody and licensing whitelist, while regulators are reluctant to accept permissionless channels that can transfer one billion dollars per block. But the reality is that real adoption is born precisely in the intersection of these two " discomfort zones " .

Crypto purists still complain, just as early Internet purists abhorred TLS certificates issued by centralized institutions. But it is HTTPS technology that allows our parents to use online banking safely. Similarly, US dollar stablecoins and tokenized Treasury bonds may seem "not pure enough", but will be the first time billions of people have silently touched blockchain—through an application that never mentions the word "cryptocurrency".

The Bretton Woods system locks the world into a single currency, and blockchain frees the time shackles of currency. Each asset on-chain shortens settlement time and releases collateral that sleeps in the clearing house, allowing the same dollar to guarantee three transactions before lunch arrives.

We continue to return to the same core view: the speed of currency circulation will eventually become a killer application scenario for encryption technology, and real assets are in line with this theme. The faster the value settlement and the more frequent the funds are deployed, the bigger the market cake will be. When the US dollar, debt and data are all flowing at network speed, the business model will no longer be a transfer fee, but profit from current potential energy.