Super agency or business wizard? Looking back at the cross-chain bridge LayerZero from V1 to V2

Reprinted from panewslab

03/10/2025·2MAuthor: Fourteen Lords

introduction

Today, the importance of cross-chain bridges is still self-evident.

However, the torrent of VC infrastructure coins also dimmed after the storm of inscriptions and Meme+AI. When the market is dull, it is more suitable to use objective emotions to examine the evolution of history and take the opportunity to explore the immortal truth behind it.

In 2023, LayerZero quickly rose with its unique "super light node" architecture and became a star project in the cross-chain track. At that time, the valuation was as high as US$3 billion. The LayerZero V2 version launched in 24 years brought 3,000W on-chain cross-chain transactions, and was also a leader in the industry.

Omnichain's vision has attracted many developers and won the favor and investment of top institutions such as Sequoia Capital, a16z, and Binance Labs; but on the other hand, it has also been questioned due to issues such as centralization and security, which has caused heated discussions in the industry.

Some people nicknamed it "technical garbage" and "super intermediary", believing that the V1 version only does frameworks but not practical things" model is "technical garbage, which is essentially just a 2-of-2 multi-signature model. The V2 version itself does not bear the security responsibility of the cross-chain verification network (DVN), and is making a fortune.

Some people also say that LayerZero's business model has entered the past three years, which is surprising and reappears in the contemporary era.

Who is right and who is wrong? Let the Fourteen Lords conduct in-depth analysis of their business model based on the technical solution to evaluate whether their foundation is stable, or is it just a castle in the sky built on the beach?

1. Technical Analysis: Architectural Evolution and Security Assumptions

of LayerZero

1.1. V1: Ultra-light nodes and safety hazards

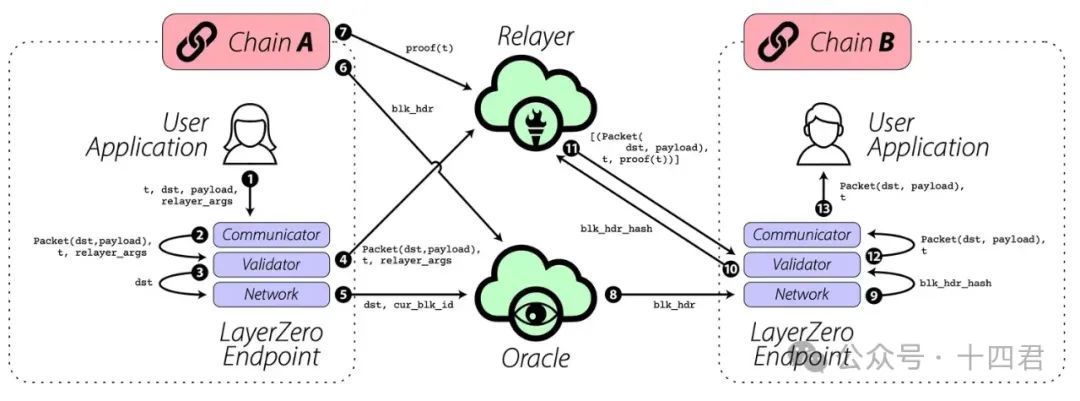

LayerZero V1 (hereinafter referred to as V1) introduces the concept of "Ultra Light Node (ULN)," and its core is to deploy a lightweight endpoint contract on each chain as a message transceiver point, and the two off-chain entities, Oracle and Relayer, jointly complete cross-chain message verification.

[Photo source: LayerZeroV1 version official white paper, used to reflect the linkage between Relayer and Oracle]

Essentially, he passed on the heavy block synchronization and verification computing work to oracles and relays, thus keeping the on-chain contracts minimal.

V1 calls this design the "ultimate trust link separation", which is much lower than other cross-chain bridge architectures because it avoids light nodes in the source chain running in full on the target chain.

So obviously, this "2-of-2" trust model of V1 is an efficiency advantage, but there are also obvious security risks:

- Collusion risk, this "anti-collusion" is entirely based on social trust and economic motivation, and lacks the coercive constraints of crypto-economics

- The boundaries of responsibility are unclear: the oracle and the relay are both off-chain roles, and V1 cannot directly control their operation. If the oracle service goes down and Relayer stops running, cross-chain messages will not be delivered, affecting availability (just as Stargate Bridge was called "cross-chain assassin" due to cost issues, it is essentially a problem with service supply).

- Chain-level risk: It completely relies on the security of each access public chain itself, while LayerZero lacks an arbitration mechanism for intermediate roles.

- V1 Although it claims that Oracle and Relayer are license-free roles and "anyone can run" these nodes, this is not the case in practice. In the voting for the Uniswap cross-chain bridge solution in early 2023, some people questioned the over-centeredness of V1, and prefer the Wormhole with large institutional validators.

1.2 V2: DVN mechanism and its security analysis

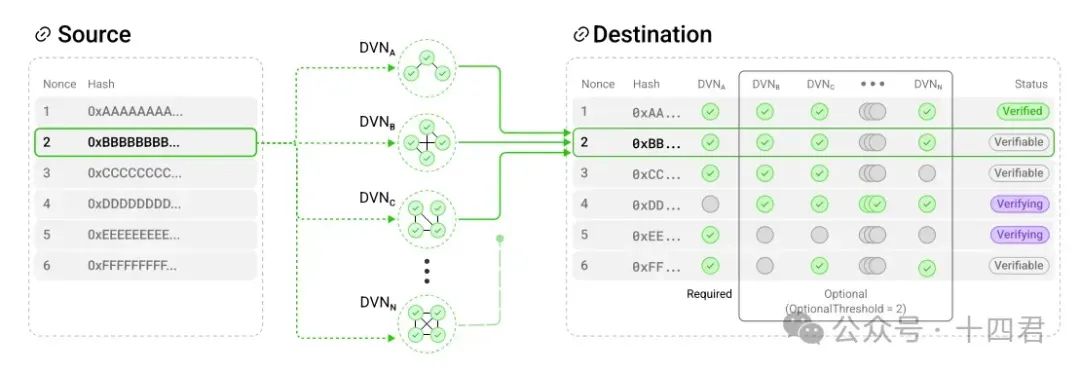

The core change of LayerZero V2 (hereinafter referred to as V2) launched in early 2024 is to introduce the concept of "Decentralized Verifier Network (DVN)" in the verification layer, getting rid of the original model of relying solely on oracle + relay.

[Photo source: LayerZeroV2 version official white paper, used to reflect optional multi-group voting for DVN]

With a network composed of multiple verification nodes for signature confirmation of cross-chain messages, developers can independently select and combine multiple DVNs to verify messages according to application needs, so that security policies are no longer limited to a fixed 2-of-2 model.

Obviously, there are advantages:

- The sources of DVN can be very diverse. According to Irene, LayerZero strategy director, the team can run their own DVN or use other existing cross-chain bridges/networks as DVNs. Even individual teams can do it, which has introduced more independent stakeholders to the system. With more people co-constructing, the cake will naturally be bigger.

- Different cross-chain verification solutions can coexist: whether it is the verifier of the official cross-chain bridge of Arbitrum, the 19 guardians of Wormhole, the PoS nodes of Axelar, or MPC multiple signs, they can all be part of its verification layer.

- User choice of autonomous: You can choose the combination of "Chainlink oracle network + LayerZero Labs DVN + Community DVN"

Is this enough?

No, the user's security depends on the quality and combination strategy of the DVN itself, or the shortest board of the barrel:

- The fragmentation of security strategies may vary greatly from DVN to strength. Some DVNs are behind professional institutional nodes and have pledged tokens, while others may just sign or have a few nodes. There is no unified security standard in the entire network, but a security island where everyone is in charge.

- Although V2 offers multiple DVN options and is recommended for combination, the final option is on the application side. If the developer chooses a weak DVN to verify separately, it will pose risks. From the market perspective, if a single DVN is already strong enough, other DVNs are often seen as redundant, and many projects may tend to use only one (for cost or convenience). Therefore, DVN needs to ensure that the pledge penalty is greater than the stolen value or is supplemented with other deterrence (law, reputation).

- **Introducing multiple DVN combinations also increases system complexity. **Attenders can exploit technical vulnerabilities rather than economic attacks. For example, the design of Nomad bridge is optimistically verified, but the implementation bug caused 190M to be stolen.

1.3 How to technically comment on V1 to V2?

First of all, from the perspective of compatibility

V2 is now a well-deserved compatibility king. It can easily access EVM, SVM and even Move systems. Its supporting documents, use cases, developer community, developer relationships (hackson, etc.) are all benchmarks at the industry's leading level. These have made its access difficulty less difficult and eventually become one of the first choices for a large number of new public chains.

Secondly, from the perspective of security

Although V2 provides a stronger security upper limit, the lower limit has also been lowered. After all, it was at least a well-known oracle mechanism in the past.

He became more like a market platform, allowing various verification networks to compete to provide security services.

But from the user's perspective, the issue of liability disputes will arise sooner or later. Now the official claims that it is only a neutral agreement, and the specific security is determined by the DVN selection of the application. Once something happens, the definition of responsibility will be denied by each other.

And just looking at the current V2's "decentralization" banner is still quite wet. DVN seems to have removed a single point, but most applications still tend to use a few DVN combinations officially recommended, and the substantial control of the system is still in the hands of LayerZero and its cooperative institutions.

Unless the DVN network can develop hundreds or thousands of independent validators and ensure honesty through strong economic game mechanisms such as pledge + punishment, LayerZero still cannot escape the fragile shadow of trust model. But at that time, there will be economic returns issues that will in turn affect the motivations of DVNs.

Next, let us continue our research from a business perspective

2. The hidden transformation of cross-chain track

2.1 Macro trends that capital focuses on

Let’s look at the data directly. The following is the financing situation of various tracks in the Web3 field from 2022 to 2024:

Since the track division may not be completely consistent, different statistical amounts may differ. The statistics in this article are only to reflect the trend. It is recommended that the original text be the basis. See the reference link at the end of the article:

Overall:

The sharp decline is Cefi-type facilities. My understanding here is that Cefi still needs financing in 222 years, and those who can make self-produce blood in 23/24 have survived to occupy the market, so they will not be able to compete around the Red Sea anymore, so the overall range has declined.

Web3 games have brought some volume after TG's popularity in 24 years, but from a personal perspective, with the decline in TG's hot spots again, both Gamefi and OnChain are almost falsified by the market, and what fake demands are left is nothing but messy.

I won’t talk about it any other thing. No matter how you look at it, infrastructure actually has the best certainty in the uncertain market.

2.2 Are financing still keen on cross-chain tracks?

As an infrastructure, the most typical one is a cross-chain bridge except for public chains, and its track advantages are very clear:

- With the explosion of multi-chain, cross-chain is a necessity. Whoever can master cross-chain traffic will have the opportunity to become the "highway" toller in the multi-chain world.

- Pain points and opportunities coexist: Cross-chain bridges are known as the key element of Web3 innovation and can stimulate new applications such as cross-chain DeFi, cross-chain NFT, inter-chain identity, etc.; however, cross-chain bridge security accidents occur frequently, and hacked funds account for nearly 70% of the total stolen amount of the entire industry.

- Platform network effect and moat: Capital factors focus on future monopoly or oligopoly potential. If a cross-chain protocol becomes the de facto standard (such as the status of TCP/IP in the Internet era), early investment will reap rich returns. This also explains why a16z, Jump and others are willing to fight against the Uniswap cross-chain bridge choice.

- Cross-chain is not just asset transfer: in traditional cognition, cross-chain bridges are tools for transferring tokens, but the greater capital imagination lies in the prospects of "Arbitrary Message Bridge" (AMB). LayerZero, Hyperlane, etc. are also positioned as full-chain communication protocols

In short, capital's popularity with cross-chain track is the result of the superposition of multiple factors: there are realistic driving forces of demand explosions and pain points to be solved, and there are also strategic considerations for competing for standards under the multi-chain interoperability pattern in the future.

However, in fact, the number of new financings generated by cross-chain bridges in 24 years is very small, but this does not mean that it is no longer popular, but because this track is no longer something new players can eat, and the product form of bridges on the market has also changed.

2.3 The transformation of Party A and Party B in cross-chain bridge

under the multi-chain trend

In the early blockchain era, cross-chain bridges usually appeared as independent service providers. With the development of the multi-chain application ecosystem, the positioning of cross-chain bridges is changing, and they tend to be lower-level services (Party B), integrated into the application or wallet usage experience:

- Cross-chain is gradually back-end, service-oriented, and quasi-interface-oriented. For example, wallets such as MetaMask and OKX integrate bridge aggregators. The bridge no longer directly controls C-end users, but obtains traffic through the B-end (DApp, wallet). This requires that cross-chain solutions must be easy to integrate and modular to meet the needs of the application. Otherwise, the application will choose another service provider, and the cross-chain bridge provider becomes the To B model.

- Polar differentiation of voice: In the "bridge controls users" mode, the bridge has the final say which chains the bridge can connect to and how much handling fee it charges. If the project party wants to connect to a certain bridge, it often needs to cooperate with its rules, which is still the case on the new chain. However, in large-chain projects, the opposite is true. For example, when Uniswap is deployed in BSC, it chooses a cross-chain bridge solution through governance voting, and the bridge is to bid for it.

There is also a role change. The original V1 version of layerZero relies on a reliable oracle. At this time, the bridge is Party B and the oracle is Party A.

Now that the launch of v2 version has triggered more competition between DVN characters, it has turned layerZero into Party A, and Party B actually performs the bridge verification function. In order to better recommend the position, Party B will naturally change the logic of sharing with Party A.

Building a platform is always more fragrant than building a shop. It is close to transactions and is not contaminated with dust. It has to be said that it is indeed a transformation of layerZero's own business positioning, which has brought the current market voice.

2.4 LayerZero's strategy of joining and connecting

LayerZero has a special positioning. It is a public facility for cross-chain communication, but it is not the ultimate bearer of the business.

As a witness to the 10-year outbreak of mobile Internet platformization, it has to be said that this kind of strategy of using early subsidies to occupy the market and later profits is too familiar!

After platformization, security responsibility has subsided.

As mentioned earlier, LayerZero gives the option to verify security to the user application, that is, "the application has its own security." From a contract perspective, if cross-chain theft occurs, LayerZero Labs can fully claim that they are not involved in asset custody, and the responsibility should be borne by the relevant DVN or application.

Cooperation and win-win replace subsidies: In order to win over applications, many infrastructure projects will carry out incentive plans or subsidies. LayerZero is more inclined to bind interests (such as investing in the other party’s projects or letting the other party invest in itself).

These chains even integrate LayerZero from Eco Fund grant incentive agreements. LayerZero Labs also actively absorbs all parties in financing and cooperation (Coinbase and Binance are both shareholders, not to mention the background parties with a large number of resources such as a16z and circle). This VC lineup has already meant to be recognized by most on-chain ecological entities.

2.5 Why is LayerZero's C round hard to find?

But on the other hand, he has already raised a Series B financing (valued at 3 billion), and two years have passed. So what scale should he use to meet his expectations in the Series C?

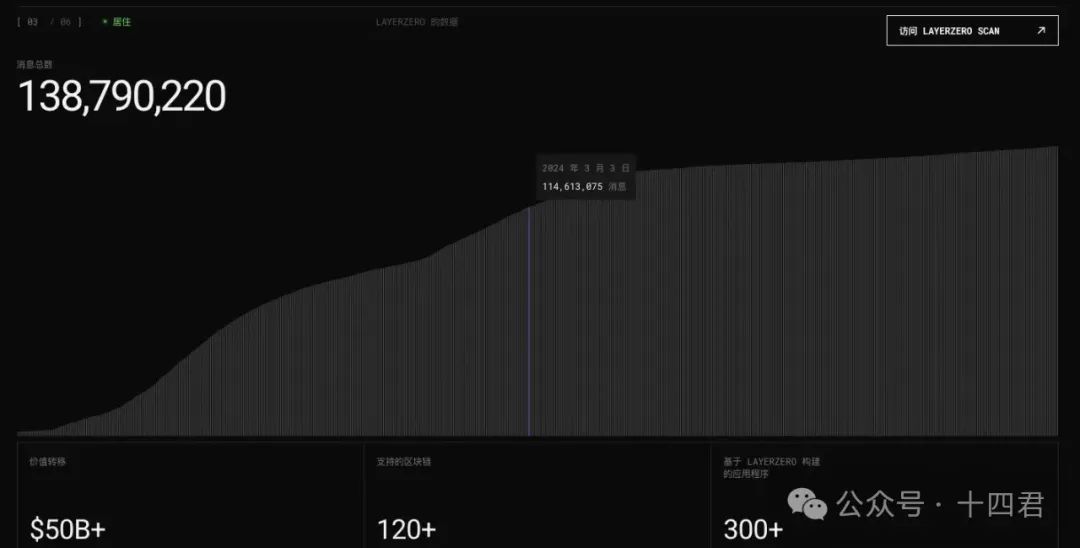

Let’s look at its current transaction size, based on its official data and the value in the middle, compare the number of news 1 year ago:

[Photo source: LayerZero official website]

The latest total number of news is 144 million, and one year ago it was about 114 million. The annual new transaction volume was 30 million, and the annual growth rate was only 26.3%, which is obviously much smoother than in 22/23.

Obviously, the main reason is that the airdrop expectations were greatly digested after issuing the coins, but in any case, issuing the coins is a kind of income, and it is even an overdraft future income, but the project valuation will return to revenue.

However, once the amount of income is calculated, it is embarrassing. First, we can simply estimate the charge based on the number of transactions: 30 million × $0.10=3 million US dollars/year

0.1 knife is a regular bridge with a low amount according to the charging range. If the amount is large, it will take the pledge charging route. The average market Take Rate is 0.05%. In the 23-year data, in the Stargate, the asset cross-chain bridge implemented by LayerZero, users will need to pay a 0.06% handling fee for each use.

Assuming that the total transfer amount of 10 billion in the past year (estimated by transactions compared to total number), the income is US$6 million based on the rate of 60,000 yuan.

Therefore, the combination of the two algorithms makes the gross profit income between 300-600W reasonable. However, considering the actual operational support, it is very likely that it is still in a loss state.

Therefore, even if the cost is completely ignored and based on the highest profit, based on the valuation of US$3 billion, its PE will reach 500 times. You should know that Apple, Amazon and other Internet leaders are only more than 30 years old.

Obviously, in the next round C, there is no way to negotiate a good price in the short term. After all, no one can digest the expectation of 500 times PE.

Conclusion

After two years of writing LayerZero, I can see its breakthrough creativity and also see the phantom of the next generation of cross-chain bridges. Finally, I use objective comments to talk about it as a reference.

From its birth to now, LayerZero has completed the journey of cross-chain bridge from 0 to 1, from following to leading the way in just three years.

It is innovative in the V1 version with "ultra-light nodes", combined with the oracle's simplified version of 2of2, and takes small steps to seize the market.

In the V2 version, it binds the multi-chain ecosystem with a platform strategy of "framework, protocol", and ensures its stability with the clever design of "risk sinking". It is currently the cross-chain protocol with the largest number of chains and chain types on the market, and it is indeed a well-deserved industry leader.

Although critics say that they do not do "dirty work" (DVN verification) but only act as an intermediary, it is undeniable that this is the successful business logic of LayerZero: to be the underlying layer of the most general and stable standards, and leave specific implementations to the market. As the platform, it uses competition from the lower level to convert the revenue from traffic.

This idea does meet the needs of the multi-chain world (the emergence of a large number of new chains urgently requires basic support for cross-chain), and also conforms to the tide of the transformation of the cross-chain bridge role from A to Party B.

Technically, the evolution of LayerZero V1/V2 shows the industry's continuous exploration of balancing security and decentralization, oracle + Relayer model and DVN mechanism, allowing us to reflect on the boundaries of minimizing trust.

The author believes that although the V2 version does not exist now, it does theoretically have the potential to achieve complete decentralization, but the market and users may not have such high decentralized security requirements at high frequency.

From a business perspective, LayerZero's platform strategy is worth studying, focusing on the direction of developer standards to bring the strongest compatibility. Through modularization and standardization, it becomes a torch for everyone to pick up firewood, rather than a stove for burning firewood alone.

This model reduces its own risks. Although it divides profits for DVN, it creates a larger ecological map.

Finally, the PE estimate is just my own opinion without the official announcement of operating costs. Maybe in the future, changes from cross-chain fees to asset management fees may bring a lot of monetization instantly. After all, in any era, traffic is always the king, and monopoly is always huge profits.

[Photo source: coinmarketcap]

Finally, another measurement algorithm is that looking at the market value of the issuing currency circulation, 7b is obviously a fanatical mood. How should 2B be understood now?