Ethereum RWA burst: regulatory changes and a new growth engine

Reprinted from jinse

06/03/2025·14DAuthor: Sam @IOSG

TL;DR:

-

Take the stablecoin bill as an introduction to the public's recent attention and discussion on RWA, and then start talking about RWA on Ethereum

-

Data analysis (zksync can be used as a highlight)

-

What impact will the emergence of Etherealize have on Ethereum?

-

Ethereum's stablecoin issuance and DeFi have always had a strong moat. Combined with the new US policies, can traditional finance and DeFi be organically linked through RWA? As the most trusted and decentralized blockchain, we continue to be optimistic about where Ethereum is.

Act catalysis and market attention

Against the backdrop of the rapid evolution of the traditional financial and regulatory environment, the recent adoption of the GENIUS Act has rekindled market interest in RWA. In addition to stablecoins and major legislative progress, the RWA field has quietly reached several important milestones: continued strong growth trends and a series of eye-catching breakthroughs - such as Kraken's launch of tokenized stocks and ETFs, Robinhood's proposal to the U.S. Securities and Exchange Commission (SEC) to grant token assets equal status with traditional assets, Centrifuge's issuance of US$400 million decentralized JTRSY funds on Solana, etc.

At a time when market attention is unprecedented and wider adoption of traditional finance is just around the corner, it is crucial to take a deep look at the current RWA landscape—especially the status of leading platforms such as Ethereum—in the face of this. RWA based on Ethereum has shown an astonishing month-on-month growth rate, often maintaining a double-digit high; the growth rate in 2025 is faster than the single-digit months in 2024. Another key factor driving this momentum is Etherealize as a catalyst for regulatory development and the Ethereum Foundation’s list of RWA as a strategic priority. At this critical node, this article will explore the development trends of RWA on Ethereum and its Layer-2 network in depth.

RWA Ecosystem Map, IOSG

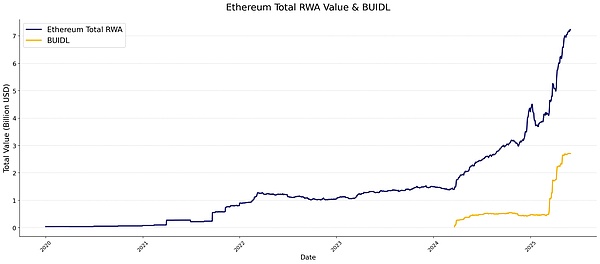

Data Analysis: Ethereum RWA Growth Panorama

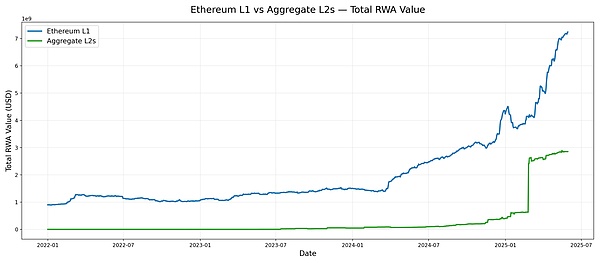

The data clearly shows that Ethereum's RWA value has entered a clear growth cycle. Looking at the total value trend of Ethereum non-stable currency RWA, its long-term trajectory is eye-catching - it has remained in the range of US$1-2 billion for many years until it entered a stage of rapid growth in April 2024. This growth momentum continues to accelerate in 2025. The core driver comes from BlackRock's BUIDL fund, which is currently worth US$2.7 billion. As shown in the orange trend line, BUIDL has shown parabolic growth itself since March 2025, strongly driving the overall expansion of the Ethereum RWA ecosystem.

RWA.xyz, IOSG

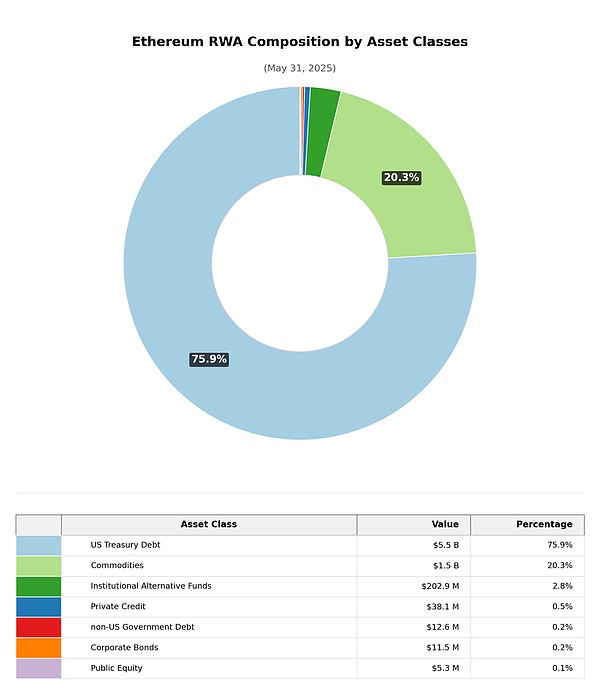

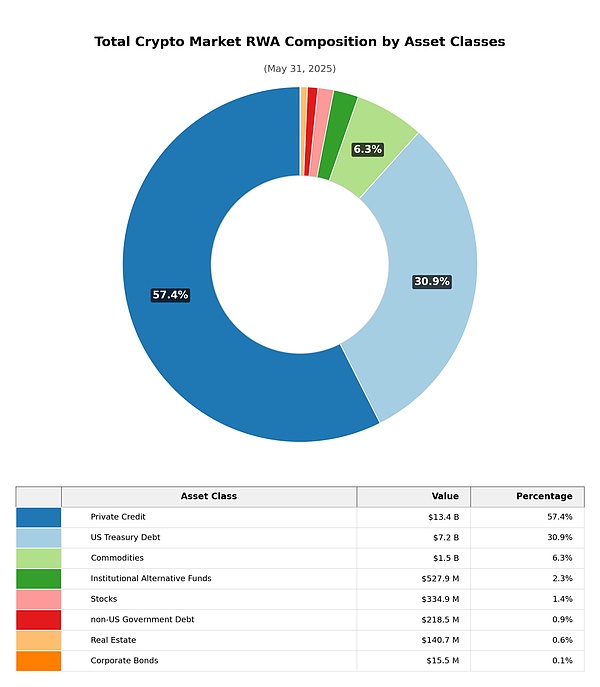

Divided by asset class (except stablecoins), the market value of real-world assets (RWA) on Ethereum is highly concentrated in two main categories: Treasury bond projects (75.9%) and commodity categories (mainly gold, 20.3%), with other categories accounting for a small share. In contrast, private equity credit accounts for the highest proportion of RWA market value composition in the entire crypto market (57.4%), followed by treasury bond projects (30.9%).

RWA.xyz, IOSG

RWA.xyz, IOSG

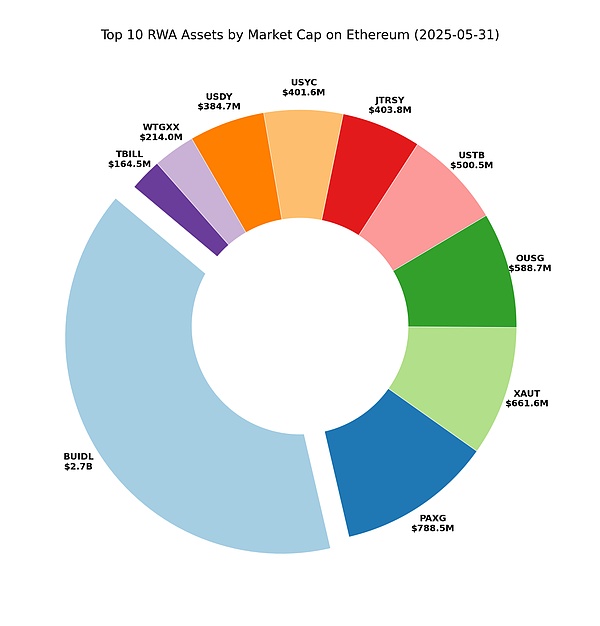

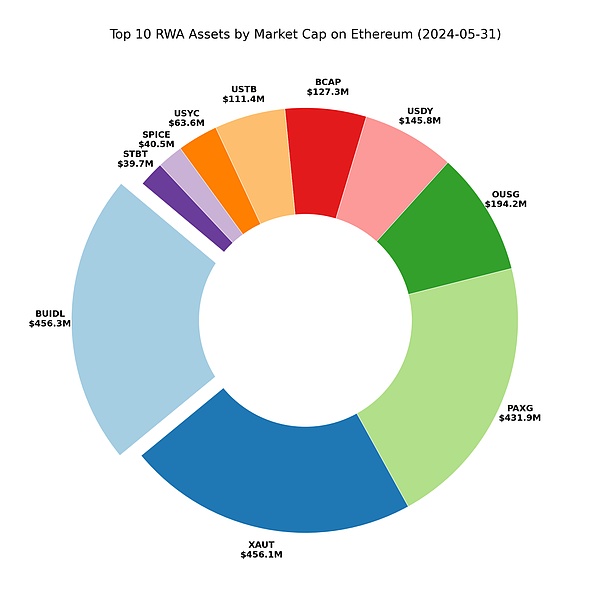

Further focus on Ethereum RWA's leading assets, the pie chart clearly reveals the dominance of BUIDL. Looking back a year ago, it can be seen that at that time, the scale of BUIDL was still comparable to that of PAXG, XAUT and other products, and now it has formed a significant surpass. Although the top ten leading projects are basically stable, the growth rate of treasury bond products is significantly ahead of gold products, and the market share continues to expand.

RWA.xyz, IOSG

RWA.xyz, IOSG

From the protocol dimension, the current leaders are mainly stablecoin issuers

- the top four protocols are Tether, Circle, MakerDAO (Dai stablecoin system) and Ethena. It is worth noting that the total value of the securitization agreement Securities has significantly surpassed some stablecoin projects such as FDUSD and USDC, and has jumped to the forefront. Other securities agreements that are among the top ten include Ondo and Superstate.

RWA.xyz, IOSG

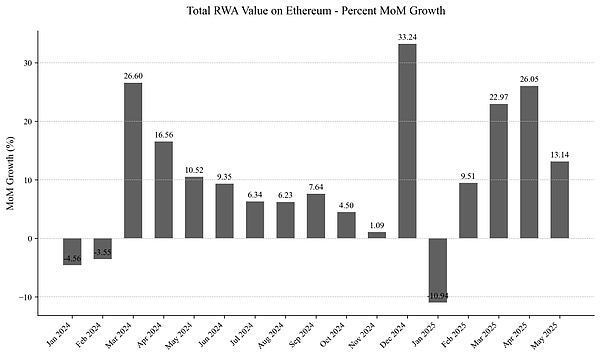

Focusing on monthly data from 2024 to date, the growth wave began in April 2024, achieving a staggering increase of 26.6% that month - contributing a quarter of the total RWA growth in Ethereum in a single month. This momentum continues to the next three months. Although it slowed slightly between August and December 2024, the network still maintained an increase of about US$200 million per month (momentum growth rate is about 5% and annualized by more than 60%.

The growth rate exploded again in January 2025, soaring by 33.2% month-on- month. After a brief pullback in February, Ethereum maintained double-digit growth for four consecutive months, with the month-on-month increase in April and May both exceeding the 20% mark.

RWA.xyz, IOSG

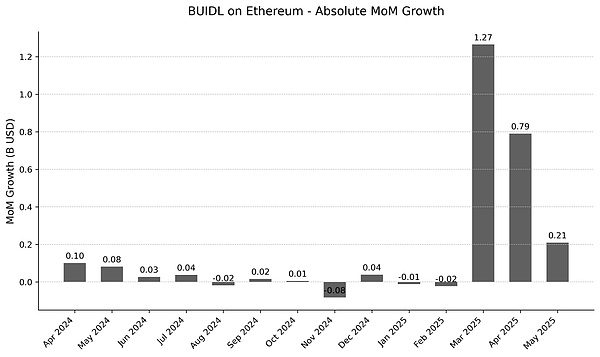

BUIDL

With BUIDL rapidly rising into the largest market value project in the Ethereum RWA ecosystem, the careful analysis of its growth path is crucial. The month-on-month growth rate chart reveals: As of March 2025, the indicator remained relatively stable, and then showed an explosive jump in March 2025. However, the latest May data showed that the ultra-high-speed growth trend slowed down slightly, but there was still a rise of US$210 million, a month- on-month increase of 8.38%. Development in the next few months is a key observation window - it is necessary to track whether its growth rate continues to slow down, or continues to increase explosively.

RWA.xyz, IOSG

The explosive growth of BUIDL stems from multiple factors. Growth mainly comes from institutional demand, and product competitiveness is the key driver of success: including 24/7 operation, faster settlement speeds than traditional finance, and high returns under the compliance framework. It is worth noting that DeFi integration is enabling synergies and opening up more utility, such as Ethena Labs’ USDtb product—which has 90% of its reserves powered by BUIDL. At the same time, BUIDL's awareness as a high-quality collateral continues to increase, and the sBUIDL launched by Securitize further unlocks the DeFi integration scenario.

The asset distribution of BUIDL is highly concentrated: about 93% is concentrated on the Ethereum main network, and the scale of other ecological chains is difficult to reach. At the same time, with the continuous expansion of asset management scale, BUIDL's monthly dividends have set new highs, with dividends reaching US$4.17 million in March 2025, and soaring to US$7.9 million by May.

BUIDL distribution, screenshot from RWA.xyz

Stable Coin

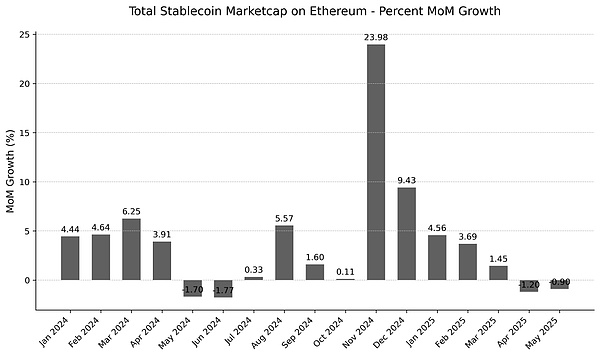

Given that the GENIUS Act will have a structural impact on the stablecoin regulatory framework, it is of great forward-looking to systematically examine the development trajectory of the Ethereum stablecoin market. Since 2024, the total market value of the sector has continued to show a steady upward trend. Although the growth rate is slightly flat compared with other RWA sub-sectors, it still maintains a resilient monthly growth rhythm.

RWA.xyz, IOSG

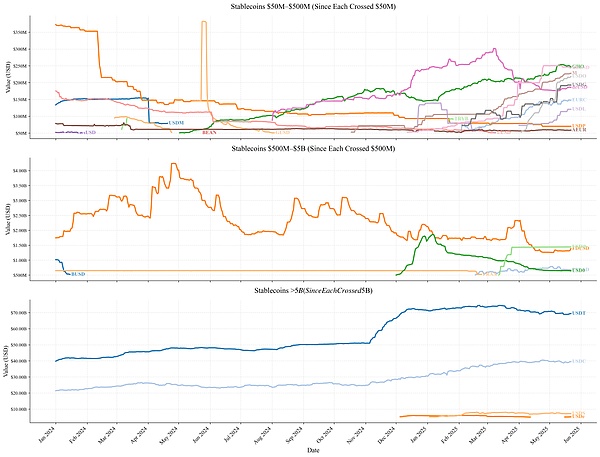

Of the small projects (<$500 million), most projects in early 2024 experienced continuous contraction. However, near the end of 2024, the market value of most projects continued to rise, and the market value of GHO, M, and USDO continued to grow. At the same time, a number of new stablecoin projects have emerged, with a market value of more than 50M. The Ethereum stablecoin ecosystem projects are more diverse, and small-cap projects have continued to flourish since 2025.

Medium-sized projects ($500 million-5 billion) were only FDUSD and FRAX in 2024; BUSD fell sharply from $1 billion in January 2024 to less than $500 million in March due to its termination of issuance. But in 2025, USD0 and PYUSD both broke the $500 million threshold, and medium-sized stablecoins are even more diverse.

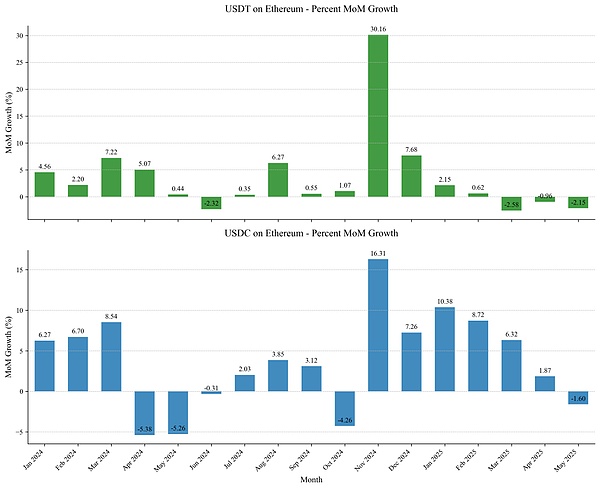

The top stablecoins (>$5 billion) continue to be dominated by USDT and USDC: USDT stabilized at USD 40 billion for most of 2024, jumped to USD 70 billion in early December, and then gradually stabilized until its recent decline in market value; USDC steadily grew from USD 22 billion in January 2024 to USD 38 billion in May 2025. At the beginning of 2025, USDS and USDe both exceeded US$5 billion, but USDT and USDC are still far ahead in terms of shareholding.

RWA.xyz, IOSG

USDT and USDC occupy an absolute dominant position, directly affecting the entire stablecoin ecosystem.

The growth in November 2024 is particularly worthy of attention: USDT surged by 30.16% month-on-month in the month, and USDC achieved a 16.31% growth. The surge has continued to grow for several months, with USDC growing more steadily in the subsequent months, with monthly growth above 5%. According to the issuer's disclosure: Tether attributed this to "the influx of collateral assets by the exchange and institutional trading stations to cope with the surge in expected trading volume"; Circle emphasized that "USDC circulation increased by 78% year-on-year... In addition to user demand, it also stems from the reconstruction of market confidence and the improvement of the standard system generated by emerging stablecoin regulatory rules."

However, market momentum has changed significantly recently - USDT on-chain Ethereum chain has stagnated growth in the past four months, and USDC has declined for the first time in May 2025 after more than a month of growth. This phenomenon may mark the market's transition to a new cycle.

RWA.xyz, IOSG

L2 Ecology

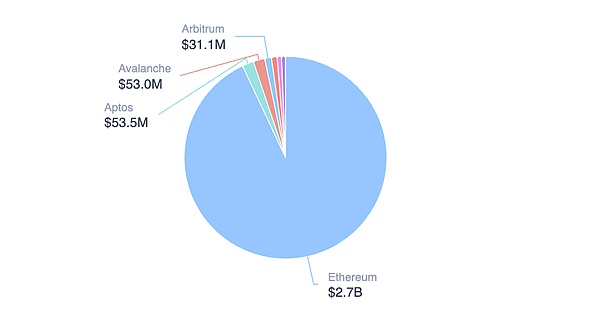

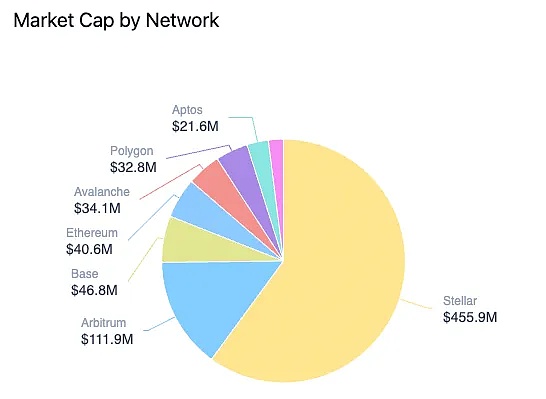

In the broader RWA ecosystem, Ethereum maintains absolute dominance with a market share of 59.23%, excluding stablecoins, but it still faces key challenges.

Screenshot from RWA.xyz

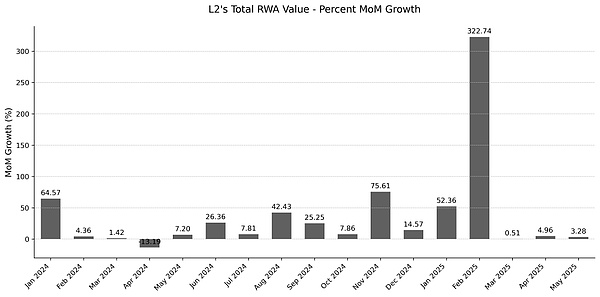

It is worth noting that zkSync jumped second with a single driver of the Tradable project, while Stellar relied entirely on the Franklin Templeton BENJI fund ($455.9 million) to occupy third place. Although the book data of the two public chains RWA are impressive, their structural shortcomings cannot be ignored: the lack of asset diversity and the dependence of a single project.

BENJI's Composition, screenshot from RWA.xyz

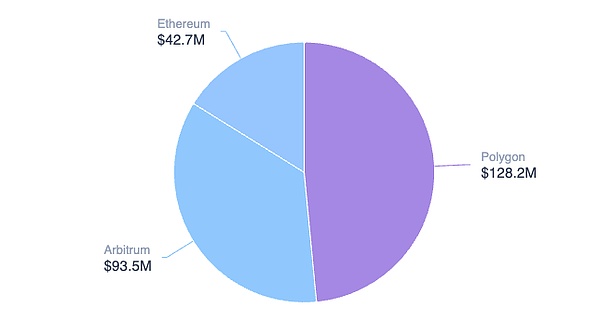

Just like the ecological characteristics shown by zkSync and Stellar, most L2 networks are currently facing the challenge of insufficient ecological diversity - their RWA market value is highly dependent on 1-2 core projects. For example, in Arbitrum: of the total market value of US$256 million, BENJI contributed US$111.9 million (43.7%), while Spiko accounts for US$93.5 million (36.5%), and the two monopolize over 80% of the market value together; Polygon also presents a similar distribution pattern, and the core market value sources are concentrated in the two major projects, Spiko and Mercado Bitcoin.

Spiko's Composition, screenshot from RWA.xyz

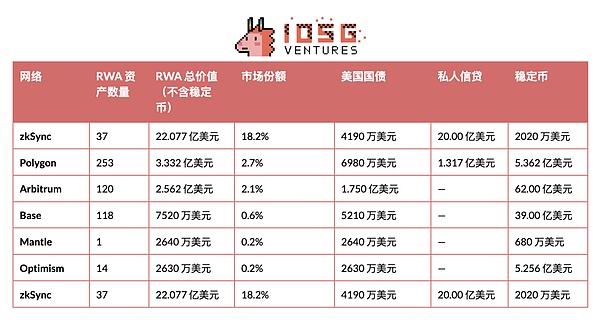

Expanding the vision to the entire L2 ecosystem, the value and market share of RWAs of each network show a significant differentiation (see table below). Except for zkSync, only Polygon and Arbitrum form substantial scale effects, and the rest of L2 are still in the early stage of development. Polygon and Arbitrum’s success relies heavily on a single driver Spiko—the project contributes about one-third of the total RWA value in both networks.

RWA.xyz, IOSG

Looking at the overall RWA market value evolution of Layer-2 network, its growth cycle is not completely synchronized with Layer-1: growth did not start synchronously in mid-2024. The zkSync access to the Tradable project brings a US$2 billion market capitalization growth. But even if this impact is eliminated, the L2 growth trend is still established - since September 2024, the L2 network has continued to maintain double-digit month-on-month growth. In contrast, RWA expansion always showed sporadic and weak characteristics in the previous stage. In summary, the end of 2024 marked a shift in the development of L2 Ecological RWA: it entered a strong growth cycle.

RWA.xyz, IOSG

Etherealize: New Ethereum RWA engine

As a key force driving Ethereum RWA adoption, Etherealize was born out of a deep insight into industry bottlenecks: when protocol-layer breakthroughs fail to effectively translate into physical applications, institutional participation often stagnates. To this end, Etherealize systematically bridges the gap between technological breakthroughs and actual implementation by developing customized tools, building strategic cooperation networks and deeply participating in policy formulation.

At present, Etherealize mainly promotes the popularization and application of Ethereum RWA through market education, content dissemination, and data panel tools. On the one hand, the team has written and published several in-depth articles about Etherealize itself and the Ethereum ecosystem. At the same time, it has participated in interviews with many well-known podcasts and traditional financial and crypto media, and has made great influence through dialogues with industry opinion leaders. On the other hand, Etherealize actively communicates with regulators, and has held several seminars and seminars on digital asset compliance and supervision issues, and has continued to propose constructive plans on how to standardize the RWA process.

Recently, Vivek Raman, founder of Etherealize, was invited to attend the House Financial Services Committee on the “American Innovation and the Future of Digital Assets” and continued to expand the important role of Ethrealize’s exchanges with regulatory.

At present, Etherealize has only launched a data board on the product side for market education and publicity, but the team explained in the roadmap that it will develop an SDK for institutions, etc., and is recruiting founding engineers. It is worth continuing to pay attention to Etherealize's progress in promoting RWA products.

In the next roadmap, the focus of the second quarter of 2025 is to release an institutional-level SDK, which combines custodial interfaces, compliance processes and gas optimization modules to help banks and asset management institutions build a safe and auditable issuance process, significantly lowering the threshold for traditional financial institutions to participate in Ethereum RWA.

On this basis, a Noir-based enterprise-level wallet pilot project will be launched in the third quarter to ensure that privacy protection reaches the enterprise-level level and meet the confidentiality needs of RWA transactions through the "default privacy" mechanism.

In the fourth quarter, we will focus on the international market: the team plans to establish cooperation with Singapore Digital Port and the Swiss Crypto Valley Association to connect localized product functions and compliance to the regulatory environment and market needs in the Asia-Pacific and Europe region.

At the same time, in order to reduce friction between different Layer-2 networks, the team will take the lead in promoting Rollup standardization and build a unified cross-link port to achieve free flow of assets, thereby integrating RWA under the Ethereum ecosystem to enhance interoperability.

Finally, in order to narrow the gap between traditional financial institutions and blockchain technology, the team will continue to adhere to the 24×7 support model, providing end-to-end professional services throughout the process, from legal document preparation to smart contract deployment.

Ethereum RWA Strategic Moat

First-mover advantage

Traditional financial institutions’ decision-making process is different from DeFi: regulatory review, pilot verification and proof of concept (PoC) will greatly extend the deployment cycle. In the early stage of the project, institutions mostly adhere to a prudent strategy and start expansion after the pilot results are verified. Although BUIDL, the leading Ethereum project, has dominated, it has only experienced explosive growth after nearly a year of accumulation. The core advantage of Ethereum lies in its ecological first- mover status - it had completed experimental cooperation with many top financial institutions long before the rise of the RWA wave.

Ecological accumulation

In addition to institutional cooperation, RWA's ecological maturity requires long-term precipitation. Ethereum to maintain leadership:

-

Broadness: Covering diversified asset issuers and agreement structures

-

Depth: The market value of multiple projects exceeds the order of billions of dollars, forming an economies of scale

The integration process between traditional finance and DeFi continues to deepen. Most RWA projects prioritize the deployment of the Ethereum main network, directly using the mature decentralized lending, market making and derivatives protocols of the Ethereum ecosystem to improve capital efficiency. Recent cases include Ethena's adoption of BUIDL as a reserve asset of 90% of USDtb stablecoins. The GENIUS Act's policy of mandating stablecoin reserves toward U.S. Treasury bonds is promoting the integration of U.S. Treasury bonds, on-chain Treasury bond products and stablecoin agreements. At the same time, the mainstream DeFi protocol incorporates BUIDL into the core collateral system.

Ethereum maintains its advantages in RWA liquidity: the number of active addresses, token types and liquidity depth are all leading. Although the Layer2 ecosystem has uncertainty in its collaboration mechanism, it is still the core path to expand capacity.

Safety

Security is the cornerstone of the RWA ecosystem, and the maturity of smart contract technology is the key. As RWA project logic becomes more complex, smart contracts are also required. In May 2025, the Sui on-chain Cetus protocol was hacked (lossed US$223 million), exposing the fatal risks of oracle manipulation and contract vulnerabilities. Although the chain freezes to recover $162 million, such passive emergency mechanisms highlight the limitations of risk control. In contrast, Ethereum's core advantages lie in a more decentralized architecture, reliable operation records and a prosperous developer ecosystem.

Technology evolution

The Ethereum technology roadmap will accelerate RWA development. First, improve L1 performance and make up for the core gap with high-performance public chains. Secondly, promote L2 interoperability and focus on the application layer to open up the docking channel between traditional finance and on-chain RWA.

At the same time, Ethereum's privacy roadmap strengthens security standards and privacy protection mechanisms (such as integrating privacy tools into mainstream wallets, simplifying anti-censorship transaction processes, etc.), provides guarantees for RWA transactions and build an asset confidentiality system that meets institutional-level requirements.

Genius Act: Regulatory Double-edged Sword

While strengthening centralized control, the new stablecoin regulatory system also injects regulatory certainty into the market. Currently, Section 4(6) of the bill does not explicitly allow stablecoin issuance to pay interest to holders, and although the market may give rise to alternatives, there is still uncertainty about this issue. Meanwhile, Genius Act requires stablecoin reserves to be 1:1 high-liquid security assets such as US dollar or U.S. Treasury bonds.

The reserves of USDC stablecoins have been almost allocated to US Treasury bonds, which comply with the new regulations. However, other mainstream issuers must completely reconstruct their reserve structure, otherwise they may be forced to withdraw from the US market. This move will directly affect specific designs such as algorithmic stablecoins and Delta Neutral stablecoins.

By anchoring collateral to U.S. sovereign credit, regulators have gained stronger intervention capabilities (and simultaneously drive Treasury demand), but loopholes in legislation may lead to new systemic risks—as the historical lessons learned from the Commodity Futures Modernization Act of 2000 (CFMA).

On the positive side, the bill’s clear compliance boundaries may accelerate institutional entry: regulatory certainty that banks and asset managers have long sought is met. More large companies and institutions will be licensed to issue stablecoins. For example, joint crypto stablecoin, which several major U.S. banks are discussing, or Meta reconsider the possibility of launching a new stablecoin project.

Ethereum’s resilience: a diverse ecosystem

The resilience of the Ethereum stablecoin ecosystem stems from its diversity. Since the beginning of 2025, the market value of multiple stablecoin issuers has increased significantly, and many new stablecoin projects have emerged, including rich design dimensions: diversified collateral structure, income strategies and governance models. The GENIUS Act enforces the 1:1 reserve requirement for Treasury bonds, which puts compliance pressure on most projects, forcing them to choose: either adjust the reserve structure or temporarily withdraw from the U.S. market.

The resilience of the Ethereum ecosystem distinguishes it from public chains dominated by a few stablecoin/RWA projects - which reduces the risk of homogeneity after projects are generally subject to regulation. The diversified structure forms a natural risk isolation mechanism: even if some stablecoins adjust their strategies due to compliance requirements, projects will continue to promote innovation and maintain the decentralized core, which will not completely become part of the US debt system. However, subsequent developments will also depend on the strategic positioning of the Ethereum Foundation and Etheralize.

Conclusion

Ethereum's RWA ecosystem has experienced explosive growth in the past few months. Among them, BUIDL is the strongest driving force for the development of the RWA in recent days, and a large number of Treasury bond projects have also shown strong growth momentum. Behind the scale expansion, Treasury bond projects have increasingly shown a trend of integrating with Ethereum's existing DeFi and RWA ecosystems, such as BUIDL as collateral for lending or stablecoin projects.

Ethereum still has a significant advantage in the RWA field. Whether it is the first-mover time advantage, security, deep ecological precipitation, grand technical roadmap update, or the strong leadership of BUIDL, the diversification of Layer2 and the deep empowerment of Ethereum, these factors have jointly built the core barrier of Ethereum in the traditional financial chain-up wave.

With the promotion of Genius Act, US dollar credit is accelerating its integration into the on-chain world. This not only brought a larger influx of funds, created more returns and growth opportunities, but also posed a challenge: it made the underlying support of the Ethereum financial system more inclined to fiat currency (USD), thus introducing fiat currency credit risks, and making the on-chain settlement system an extension of the hegemony of the US dollar; the on-chain world is no longer an independent parallel financial system. Against this backdrop of explosive growth, there are also hidden worries. The core lies in Ethereum's exploration of its own positioning

- that is, whether it supports deep binding to the US dollar system.