Ethena's moat

Reprinted from jinse

05/26/2025·13DAuthor: Ponyo, researcher of Four Pillars; Translation: Golden Finance xiaozou

Have you tried eating instant noodles on a roller coaster? This may sound ridiculous, but it is the best metaphor for Ethena Labs' daily performance – a team of only 26 people firmly maintaining the $1 anchor of the $5 billion market capitalization stablecoin USDe amid the ongoing turmoil in the crypto market. This article will reveal Ethena's moat, analyze its core mechanisms that are difficult to replicate, and explain its strategic path to promote USDe's circulation to exceed US$25 billion.

1. Precision machines that hedge billions of fluctuations

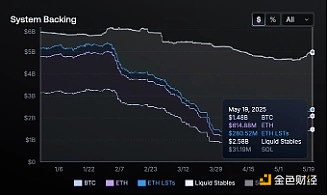

Stablecoins seem boring (1 dollar is 1 dollar), but Ethena has hidden mystery. It does not rely on bank dollar reserves, but builds a collateral pool through ETH, BTC, SOL, ETH current pledged tokens (LSTs), stablecoins and USDtb, USDtb, 1.44 billion Treasury bond tokens, and continues to short hedge in the derivatives market. When the price of a collateralized asset fluctuates, the profit and loss of the corresponding short position will offset the risk in real time.

If ETH soars by 5% lead to an imbalance in hedging ratio, it may instantly expose the exposure of tens of millions of dollars; when the market collapses at 3 a.m., the risk control system must immediately rebalance the mortgage or close the position - the fault tolerance rate is nearly zero. But in the roller coaster market in 2023-2024 , Ethena handled billions of dollars in hedging every day but never deaned, lost positions or had a mortgage gap, and even remained unscathed when Bybit was hacked.

Traditional hedge funds may require traders across the floor to cope with this volatility, and Ethena uses minimalist teams to achieve zero accident operations.

A few months after its launch, it has become the largest counterparty of many top exchanges. Its hedging traffic can even affect the market depth, but it has been rarely noticed because USDe has always "operated as usual".

The truth about high yields: Ethena provides double-digit annualized returns when the market is bullish . Some people think of the tragedy of Terra/LUNA ' s 20% Anchor agreement, but the essential difference is that Ethena ' s returns come from the real market inefficiency (staking income + perpetual contract positive fund rate, etc.), rather than printing coins out of thin air or unsustainable subsidies.

2. How the Delta neutral strategy works

Users deposit ETH worth US$1,000 and can mint USDes equivalent value, and the agreement automatically opens equal futures short orders. When ETH falls, short profits offset collateral depreciation, and when ETH rises, collateral appreciation makes up for short losses, and ultimately maintains the stability of the net value of the US dollar. When the long leverage of the perpetual market is too high, Ethena, which holds short positions, can also charge a capital fee rate, allowing USDe to naturally generate double-digit returns in the bull market - no need for treasury subsidies.

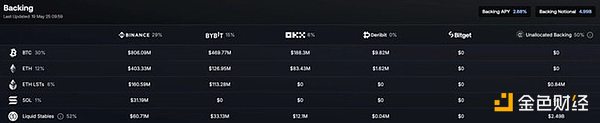

To avoid single-point risks, Ethena distributes short positions among Binance, Bybit, OKX and even decentralized perpetual agreements. The latest governance proposal shows that Hyperliquid will be connected to achieve dynamic hedging of liquidity optimality.

In order to handle uninterrupted adjustments, Ethena and the trading team deployed a high-frequency trading-level automation system, and real-time rebalancing of multi-platform collateral ensures that USDe stands firm in extreme fluctuations.

The agreement also uses over-collateral to deal with the plunge and suspends minting when risks are too high. Through custody solutions such as Copper and Fireblocks, assets are always in real-time controllable, avoiding stranded on exchange hot wallets. If the exchange breaks down, Ethena can quickly withdraw the mortgage to eliminate single point of failure.

3. Unreplicable moat

Ethena's model seems replicable on paper (delta hedges crypto assets, earns capital rates, earns profits), but in fact the agreement has established a strong moat enough to stop imitators.

One of the key obstacles is trust and credit: Ethena hedges billions of dollars in off-market positions through institutional-level agreements with custodians and mainstream trading platforms (Binance Ceffu, OKX). Most small projects simply cannot easily access these institutions and negotiate to support millions of dollars in short positions with minimum exchange mortgage rates – a authority that requires institutional-level legal, compliance and operational rigor.

The same key is multi-platform risk management. Spreading large-scale hedging across multiple exchanges requires real-time analytics comparable to Wall Street's quantitative team. Yes, anyone can replicate the delta hedge on a small scale, but scaling to a $ 5 billion scale (and rebalancing huge collateral across multiple platforms around the clock) is another matter. The required analytical capabilities, automation systems and credit relationships will grow exponentially with scale, making it almost impossible for new entrants to reach the Ethena order overnight.

Furthermore, Ethena does not rely on sustainable risk-free benefits. If the perpetual capital rate turns negative, it shrinks its short position and relies on pledge or stablecoin returns. The reserve mechanism can buffer the long-term negative rate phase, while countless high-yield DeFi protocols collapse when music stops.

The counterparty risk is further minimized because Ethena never deposits all collateral assets directly on a single exchange, but rather keeps the assets through the custodian. If there is an unstable situation on a trading platform, Ethena can quickly close positions and transfer collateral assets to the outside chain to ensure that systemic risks are minimized.

Ultimately, Ethena's actual combat record under extreme fluctuations consolidated its moat. USDe has experienced severe market fluctuations for several months and has not seen a single dean or collapse. This reliability has driven new user adoption, exchange listings, and collaborations among top institutions (from Securitize to BlackRock and Franklin Templeton), creating a trust snowball effect that cannot be replicated by forks. The gap between empty talk delta hedging and the 7×24-hour billion-dollar actual combat is the core of Ethena's standout.

4. Going toward a $ 25 billion path

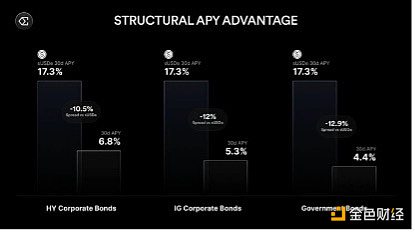

Ethena's growth strategy relies on the co-evolutionary self-circulation ecosystem of currency (USDe), network ("Converge" chain) and exchange/liquidity aggregation. USDe was initially driven by native demands of DeFi (Aave, Pendle, Morpho) and CeFi (Bybit, OKX), and the next phase will launch iUSDe—that is, a regulated version of banks, funds and corporate treasury that require a compliance framework. Even if it only attracts a small share of the huge bond market in traditional finance, it can push the stablecoin circulation to $25 billion or even higher.

What drives this growth is the arbitrage mechanism between on-chain capital rates and traditional interest rates. As long as there is a significant return difference, funds will flow from the low-interest rate market to the high- interest rate market until they are equilibrium. USDe thus becomes the hub point connecting cryptocurrency returns and macro benchmarks.

Meanwhile, Ethena is developing a Telegram-based application that provides high-yield dollar savings services to ordinary users through a user-friendly interface, bringing hundreds of millions of funds into sUSDe. In terms of infrastructure, the Converge chain will weave DeFi and CeFi tracks together, so each new integration will amplify the liquidity and utility of USDe during a continuous growth cycle.

It is worth noting that the returns of sUSDe are negatively correlated with real interest rates, which was proven in the fourth quarter of 2024: At that time, the Federal Reserve cut interest rates by 75 basis points, and the yield on funds jumped from about 8% to more than 20%, highlighting that the decline in macro interest rates can greatly enhance Ethena's yield potential.

This is not a slow, gradual process, but a circular expansion model: wider adoption enhances USDe's liquidity and earning potential, thereby attracting larger institutions, driving further growth in supply and a more solid anchor.

5. Looking forward to the future

Ethena is not the first stablecoin to promise high returns or tout innovation paths. What's unique is that it truly fulfills its promise - always anchoring USDe stably at $1 during the most violent market turmoil. Behind the scenes, it operates like a top organization: shorting perpetual contracts and managing pledge collateral. What ordinary holders feel is just a "stable and always reliable" US dollar tool.

It is no easy task to move from 5 billion to 25 billion US dollars. Strict regulatory reviews, expanded risk exposure to counterpartys, and potential liquidity crises may all bring new challenges. But Ethena's multi-asset mortgage pool (including US$1.44 billion USDtb), powerful automation systems and rigorous risk control systems make it more responsive than most projects.

Ultimately, Ethena is showing how it tames the volatility of the crypto market with a disciplined delta neutral strategy on an amazing scale. This outlines a future picture: USDe will become the core of all financial fields - from the permissionless borders of DeFi, the trading terminals of CeFi, to the trillion-level bond market of traditional finance.