Crypto payment cards are in chaos, a business that is difficult to last?

Reprinted from chaincatcher

05/15/2025·23DAuthor: Web3 Farmer Frank

How many "U cards" do you have now?

From the early Dupay, OneKey Card, to Cards launched by exchanges Bitget and Bybit, to Infini, Morph and SafePal’s crypto payment card services, even Coinbase and MetaMask have entered the market. Since this year, crypto payment cards (U cards) targeting PayFi narratives have almost become the standard for Web3 projects.

Under the new round of players' encirclement, various U cards have been widely promoted and tweets and evaluation information, which once reminds people of the colorful shared bicycles on the streets. The wide range of options have also diverged the market's focus from usability, gradually refining it into a comparison choice for registration/use threshold, rate and other dimensions, trying to find the king of cost-effectiveness in the "Card Sea".

However, if you look at it for a long time, you will find that the U-Card track is prosperous on the surface and still cannot conceal its fragility at the bottom. To put it bluntly, the life cycle of a U card is sometimes not necessarily longer than some meme coins : there are countless cases of running away, shutting down, and card replacement. Most of the crypto payment card players in the previous wave have long disappeared.

The reason is simple, safe and compliant, and it is always the sword of Damocles hanging over the heads of all U cards. In addition to relying heavily on channel banks ' willingness to comply with the crypto business, U cards themselves also have natural architectural flaws - the custody rights of the fund pool are in the hands of service providers, which is a great test of operational capabilities and ethical standards . If there is a problem with any partner bank or service provider, users may become innocent cannon fodder...

As for the current "100 Regiment War", the cost of U cards at the bottom is mostly converged, and user experience often depends on subsidies, high interest rates and other measures. However, these short-term incentives obviously cannot build true long-term competitiveness. Once subsidies decline, in the face of homogeneous card-binding consumption services, it is difficult for users to tell which brand will have long-term loyalty.

Therefore, as the traditional U card model gradually exposed the ceiling, some crypto payment card services began to emerge, and some interesting attempts were carried out from multiple dimensions such as financial management and bank accounts:

For example, the "card + financial management" form of the celebrity project Infini provides custodial interest-generating income for the Crypto assets deposited by users through on-chain DeFi configuration; the "card + bank account" form of the old wallet SafePal allows users to truly hold a Swiss bank account with their own real name, realizing the overseas brokerage/CEX deposit and withdrawal experience under the EUR/SCHF framework.

Objectively speaking, whether the broader "card+" service in the future can truly break out of the cycle and become an exception remains to be further tested by the market, but it is certain that only those crypto payment card projects that can balance security, compliance and user experience may be able to break the curse of "short life" in this "chaotic era".

Encrypted payment cards, hard to say "evergreen"

Why can U cards transform from a niche track into a "hot commodity" that everyone competes for?

There are only two core reasons behind it.

First of all, under the background of "bear market" when writing, "bull market" when publishing, "when you see this article, "when you see this article,"), crypto payment cards are actually a good business that can both make publicity and traffic : not only have a clear profit model and stable cash flow, but also significantly improve user activity and community stickiness.

After all, one of the biggest pain points for Web3 players, especially mainland Chinese players, is the deposit and withdrawal: how to directly use the Crypto in your hands for daily consumption payments, and if you convert the Fiat in your hands to Crypto in compliance and convenience, it has always been a natural implementation scenario with strong demand.

Therefore, for Web3 projects that urgently need to expand their business boundaries, they are almost happy to enter this track regardless of whether they were originally strongly related to the PayFi track, which also makes U Card a rare "deterministic business" and the best business development port in the eyes of many Web3 projects.

Secondly, in addition to market demand, the entry and issuance threshold for crypto payment cards is not high, which is also an important factor that attracts many project parties . They are usually issued by Web3 project parties (such as Infini and Bybit mentioned in the article) and traditional financial institutions (banks and other card issuing institutions), presenting a three-level structure of "card organization-card issuing institutions-Web3 projects".

Source: @yuxiaoyu111

Take the common Mastercard U cards on the market as an example:

- Card organization : It is Mastercard, and the card BIN number segment (the first six digits of the bank card) is the core resource of the payment system, which is directly authorized by the card organization to first-level card issuing institutions (such as licensed banks and electronic currency institutions);

- Level 1 card issuing institutions : Licensed financial institutions such as the DCS Bank in Singapore (DeCard) are responsible for compliance-level fund custody and card BIN management;

- Web3 project party : As secondary card issuers, they cannot directly obtain card BIN, and can only obtain technical authorization through cooperation with first-level institutions, and be responsible for the product design and operation of the user side;

Among them, the first-level card issuing institutions play a key role in the entire chain, responsible for connecting with card organizations, mastering consumption data, and handling risk control affairs, such as freezing and card blocking. The Web3 project party focuses on brand building and user operations, and builds a business model for traffic conversion.

However, this is the risk point. Once a secondary card issuer is reported to have violated regulations (such as money laundering, unknown capital flow, etc.), the card organization or regulatory agency may directly punish it. Even if there is no direct violation, some banks may tighten the cooperation gap due to regulatory pressure or risk control considerations.

This has led to the risk of shutting down related U card services at any time, and it also explains why so many "U card" projects that have emerged have very few that can survive a year and a half.

Of course, there is another deeper problem, which is the risk of fund security, because under this architecture, most U cards are essentially prepaid cards that recharge first and then consume. Users first recharge funds to the project party, and what they obtain is only the "consumption amount" based on the recharge record, rather than the independent custody of real assets.

This is no different from the fitness cards and supermarket recharge cards we are familiar with. For example, if you spend 5,000 yuan in a gym to apply for a deposit value card, the funds will go directly to the gym's bank account. The gym promises that you will deduct each purchase from the credit limit in the card, but there is no independent 5,000 yuan in cash stored in the card, but it forms a "fund pool" with the recharge funds of other members.

The gym may use this fund pool to pay rent, purchase equipment, or even invest in other branches. However, if the gym goes bankrupt due to poor management one day, or the boss runs away with the money, your stored value card amount will become "waste paper", because you have never really owned "5,000 yuan of your own", but only have "debt claims" to the gym.

The same is true for U cards. If you recharge 100 USDT/USDC, it is directly transferred to the unified on-chain fund pool controlled by the secondary card issuer. The "fiat currency limit" obtained by each user is only a sub-account of the project party under the company account opened by the issuing agency based on the recharge situation. It is only used for payment and settlement. There is no actual fiat currency deposit in the card - you can use it for consumption, but you cannot transfer freely.

In other words, most of the Crypto assets recharged by users flow directly into the project party’s chain accounts, rather than the real bank account system. The corresponding fiat currency side does not independently open an account with the same name for users, but only allocates consumption quotas through a unified account. Your "quota" is essentially just a string of numbers. Whether it can be fulfilled depends entirely on the platform’s survival ability and willingness to repay.

This model means that the safety and stability of the entire system are almost entirely dependent on the project party's moral standards and risk control capabilities.

When the accumulated user funds reach a certain scale, if the project party experiences moral risks (such as misappropriation of funds, running away with the money), or risk control fails (faulting of capital chain, hacker attacks, and inability to deal with large-scale runs), user assets will face the risk of losses or even unrecoverable (online U card run-off cases emerge in endlessly).

Currently on the market, most of the U card products launched by the exchange or the crypto payment cards for celebrity reputation projects are prepaid cards, so it is difficult to do long-term business. Of course, U cards issued by platforms with good reputation and compliance capabilities can reduce risks to a certain extent.

"Card+" service: new variables for encrypted payment cards?

Because of this, more and more project parties are no longer satisfied with a single U card service, but are actively seeking to transform to a direction with more financial attributes and long-term value.

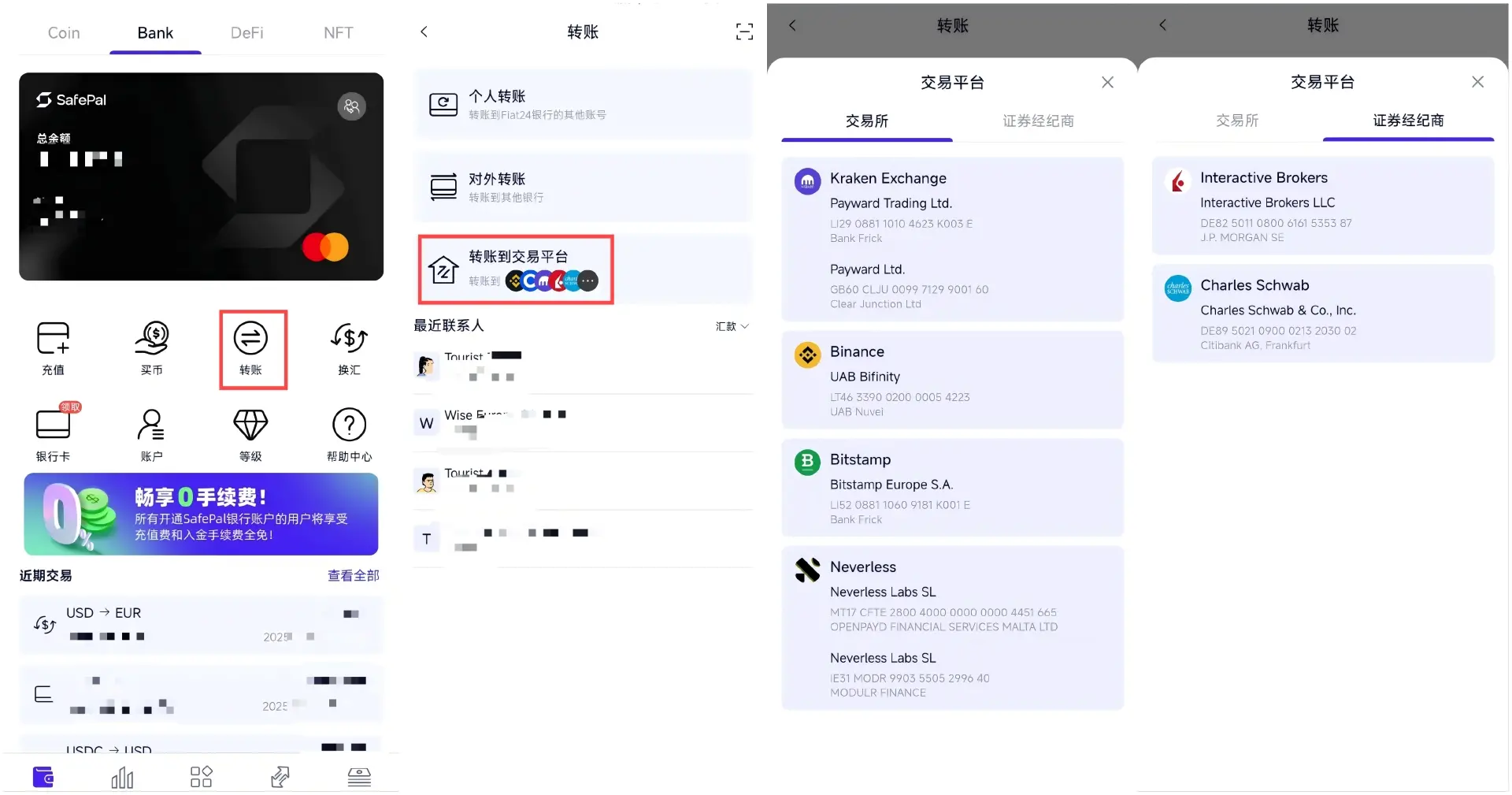

For example, Bitget and SafePal no longer focus on the simple "U card" business by investing in crypto-friendly banks with financial licenses (such as DCS and Fiat24), but instead start to lay out the comprehensive financial service system of "card + bank account" and break out of the business scope of a single consumer tool.

Taking SafePal as an example, it disclosed its strategic investment in Swiss compliant bank Fiat24 at the beginning of 2024, and officially launched personal Swiss bank accounts and joint Mastercard services for users in mainland China at the end of last year. The author also tested and experienced this "U card" service form.

Simply put, the biggest advantage of this "non-U card" model is that it fundamentally solves the fund security problems existing in traditional U cards - users directly hold bank accounts of the same name, and funds enter the real banking system, rather than deposited in the project party 's fund pool, effectively reducing the risks of running away, running and redemption.

Even if there are problems with the Web3 project itself in extreme cases, users can still withdraw funds independently through the banking system. This fund independence and security are incomparable to the traditional U card model.

More importantly, this model opens up a wider channel of deposits and withdrawals, and in a sense realizes the seamless connection between TradFi and the Crypto world: taking SafePal & Fiat24's bank account service as an example, users can not only complete free deposits and withdrawals of overseas brokers (such as Interactive Brokers, Schwab Financial Management) and CEX through personal bank accounts, but also transfer funds back to Alipay/WeChat or domestic banks through channels such as Wise (Euro SEPA transfer), to realize the closed loop of asset flow on and off-chain (extended reading " SafePal Practical Manual: Transfer and Remittance Brokers/CEX, the most comprehensive guide to connecting Crypto and TradFi ").

In contrast, most U card products are still in the stage of competition for subsidies and rates. Taking Bybit as an example, it attracts users through a high proportion of cashback strategy, but a 10% or even higher cashback means that the competition for rate is close to the limit. Once the subsidies decline, the serious homogeneous product experience cannot retain users, let alone build true brand loyalty.

This structural contradiction makes it destined to be difficult for most pure U card products to cross cycles, and the broader "card + bank account" model may be the direction for a few projects to break through.

The author also sorted out the crypto payment card products with good reputation in the current market, and made a rough comparison of the account registration threshold, fee structure and compliance functionality during actual use:

From this comparison, we can see that the "card + bank account" model currently adopted by SafePal has significant advantages in fund security, fee rate and functionality, especially in terms of compliance and support capabilities in actual deposit and withdrawal scenarios, it has built a competitive barrier that is difficult to be simply copied.

On the surface, crypto payment cards compete for rate subsidies, but in fact, they compete for who can master truly scarce compliance resources and financial infrastructure. Only players who master licenses and bank-level resources can have the last laugh in the chaos.

New narrative curve from "U card" to "card + bank account"

Starting in 2025, Web3 Payment has somehow reached its narrative turning point.

The biggest difference is that in the past, the entire track focused on crypto payment solutions that focused on 2B enterprise services. Now more and more leading institutions are beginning to enter the 2C consumption scenario. The most representative case is OKX's newly launched OKX Pay, which also directly enters the personal payment market and opens up the mass market with its own traffic and ecological advantages.

From the perspective of development trends, it is only a matter of time before the "pure U card" model is eliminated. The market has gradually evolved from a single payment tool to a comprehensive asset management tool . After all, U cards only achieve "consumption terminal access", but cannot build a complete ecological closed loop of capital flow - for example, when users need to transfer money to Interactive Brokers, 99% of U cards can only remain silent.

Therefore, only by transcending the simple consumption card positioning and integrating savings, investment, remittance and other functions can we grasp the new narrative curve.

Just like the gameplay of SafePal& Fiat24, it allows users to directly invest in Interactive Brokers through their euro accounts, and can also use tools such as Wise to freely remit money to Alipay, realizing the free flow of funds on and off-chain funds, allowing Crypto wallet to have the ability to have almost full-function commercial bank accounts.

From this perspective, Web3 wallets naturally have the ability to manage crypto assets and are the ideal PayFi service carrier . This is also the fundamental reason why OKX Pay and SafePal accelerate the promotion of the "card + bank account" model. They try to provide a new asset management experience that integrates the convenience of virtual cards, compliant bank account security, and decentralized features:

Users can enjoy decentralized features through non-custodial wallets, and can also use Visa and Mastercard networks to make global consumer payments, while also enjoying financial services close to traditional banks (transfers, remittances, deposits and withdrawals), but they still retain the flexibility of crypto assets.

In the future, when crypto assets are further integrated into the global financial system, this model may be the ultimate solution to truly achieve large-scale user growth.

The evolution from "U card" to "card + bank account" has clearly shown the breakthrough of crypto payment cards - finding a new narrative curve, moving from a single consumption tool to a comprehensive asset management entrance.

In the future, the competition will no longer be given more cashbacks by whoever gives, but who can truly open up the last mile between Crypto and TradFi. This market ultimately belongs to those long-termists who can build financial infrastructure and have compliance resources, rather than traffic players who are short-term arbitrage.

Written at the end

Back to the original question: Can crypto payment cards become a sustainable business?

The so-called "short life" essentially reflects the endogenous defects of the business model - excessive reliance on subsidies to drive, lack of compliance moats and real user stickiness. When subsidies fade and supervision becomes stricter, this seemingly lively game will naturally end.

But that doesn't mean the story will end there.

In other words, "short life" may not be fate, but in order to "eternalize", we must re-tell a new business philosophy that conforms to the essence of finance and can travel through cycles.

jinse

jinse

panewslab

panewslab