Bankless: Why Lido’s bull fundamentals have never been stronger

Reprinted from jinse

01/02/2025·4MAuthor: Jack Inabinet, Bankless; Compiler: Tao Zhu, Golden Finance

The rise of re-staking caused cryptocurrency investors to sell off Ethereum staking giant Lido Finance in the first half of 2024, causing LDO to fall to multi-year lows against ETH.

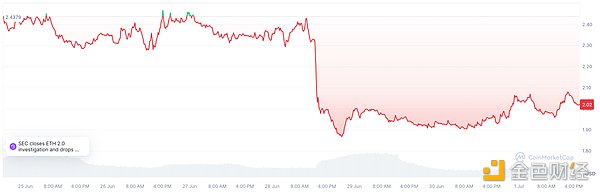

Over the past few weeks, LDO investors have been energized by the prospect that the agreement could upend EigenLayer's dominance. But LDO holders were dealt a heavy blow on Friday when the U.S. Securities and Exchange Commission designated its liquid pledge tokens as unregistered crypto-asset securities in a lawsuit filed against MetaMask creator Consensys.

LDO may have lagged far behind ETH on a year-to-date basis, but today, we'll discuss why LDO's fundamentals have never been stronger.

Re-staking competition

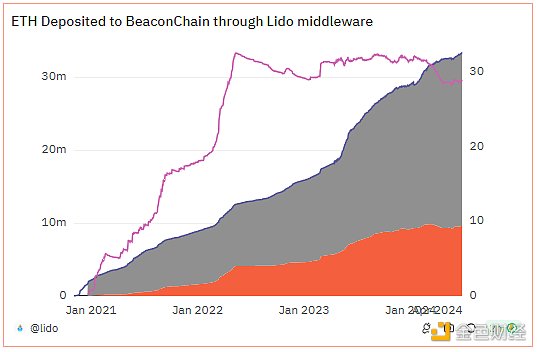

In 2023, Lido was unstoppable, amassing one-third of all staked ETH and doubling the amount of ETH under management.

Throughout the year, Lido's control over the proportion of staked ETH has been threatening to breach 33% - the first of three key thresholds at which staking entities can more easily manipulate consensus - which has sparked outrage among Ethereum users. There is a heated debate between the ecosystem as to whether the ecosystem should enforce staking restrictions on Lido to prevent unnecessary centralization.

In 2024, these contentious conversations have moved to the fringe, while the share of ETH staked by Lido has dropped to a seemingly more acceptable 29% (purple line), the lowest level since April 2022.

While Lido continues to enjoy net ETH inflows, the protocol's market share decline coincides with the emergence of a breakthrough phenomenon that challenges the dominance of its original staking model: staking. Although the restaking service is neither operational nor generating revenue yet, the project that provides meta information by promising future airdrops has quickly become the hottest farm this year.

In just a few months, EigenLayer, ether.fi, Renzo, Puffer, and Kelp have all grown from relative obscurity to trusted protocols with billions of dollars in TVL!

Putting aside the controversial nature of restaking, the appeal of related airdrops is undeniable, and Lido’s restaking competitors have been able to grab market share due to the sheer amount of capital chasing these lucrative airdrops.

The arrival of EigenLayer’s highly anticipated airdrop sparked a second wave of depositor excitement in May, however, the rise of Lido-aligned restaking alternatives threatens to reshape the industry…

symbiotic relationship

Symbiotic’s deposit contract just hit mainnet two weeks ago and has amassed $300 million in deposits since its launch, making it the fastest-growing restaking protocol in June and one of the few protocols in the space to experience TVL inflows this month one!

The protocol is undoubtedly the most credible EigenLayer competitor in existence, as it received seed funding from Paradigm, a well-known crypto venture capital firm, and cyber·Fund, an investment firm that was an early contributor to the Lido DAO.

While Symbiotic is largely a clone of EigenLayer, with plans to provide re- staking services for a variety of assets, this re-staking ecosystem is unique through its close ties to Lido.

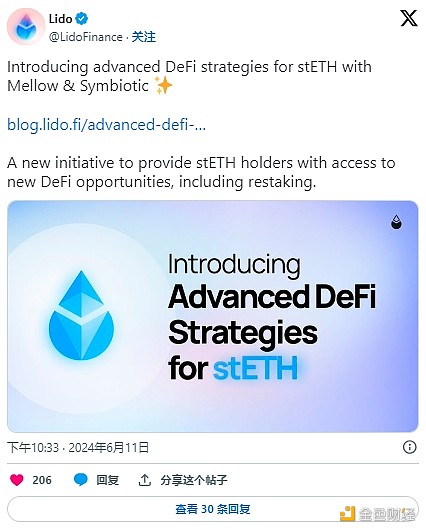

Coinciding with the launch of Symbiotic is Mellow Finance, a re-hypothecation vault management service also backed by cyber·Fund and designated as the first member of the “Lido Alliance”, a status that demonstrates close ties with Lido formal cooperation and recognition.

Unlike the EigenLayer liquidity re-staking model, which encourages users to deposit to independently staking non-Lido re-staking managers, Mellow Finance’s custodial deposit model turns re-staking operators into pure liquidity staking token principals.

Compared to popular liquidity re-staking alternatives, Mellow Finance is able to quickly convert it to LST, thereby better managing the liquidity risks associated with LRT (i.e. the need to withdraw through the Ethereum staking queue in the event of a decoupling) converted to ETH at par); this design also reinforces the implicit winner-take-all dynamics of staking.

Since token liquidity is a key factor in assessing the attractiveness of LST, and Lido holds a massive 60% share of this staking market segment, stETH re- staking through Mellow has clear advantages from a risk-adjusted perspective.

Although stETH holders can only get one airdrop opportunity under the EigenLayer mechanism, they can obtain Mellow and Symbiotic points by utilizing Mellow.

Meanwhile, many EigenLayer restaking projects have already distributed their first round of tokens, diluting the potency of their future rewards and cementing Mellow’s status as a top airdrop farm.

Once existing stETH capital migrates to this opportunity, and the underlying bull case for Symbiotic x Mellow re-staking becomes apparent, EigenLayer's employment capital will most likely flow from the associated LRT to stETH, ultimately triggering a measurable increase in Lido staking market share for the first time in two years growth.

Summarize

The SEC's attempt to designate Lido's stETH as a cryptoasset security poses unresolved risks to unregistered staking services, but the incident may have created a local bottom, leaving little unexpected danger until the pending litigation is decided years later Will destroy LDO.

A business does not need to be attractive to be a sound investment, and while re-staking has become a focus for cryptocurrency investors, staking providers can equally generate fees from depositor earnings, with the added benefit of a reliable revenue stream.

Lido has more than $30 billion worth of ETH under management, with an annual interest rate of 3%, and the protocol currently generates $1 billion in annual revenue at a 10% interest rate, giving the token a price-to-earnings (P/E) ratio of approximately 23x. While this is considered "average" for the stock, such a multiple appears to undervalue LDO given the high growth potential of the crypto industry and the aforementioned Lido-specific tailwinds.

There's no denying that Lido's current 10% management fee for running a low- cost software venture could easily be squeezed if competitors tried to corner the market with low-cost alternatives, however, extensive stETH integration and market-leading liquidity across DeFi Provides Lido with a degree of flexibility to charge additional fees for its services.

Assuming the Symbiotic ecosystem takes off in the coming months, stETH will once again approach the 33% staking concentration threshold, and while this will certainly reignite the debate over whether Ethereum should impose a hard cap on Lido, the decentralized social consensus It will be difficult, if not impossible, to implement such drastic network changes.