Usual analysis: Sushi attack on Tether

Reprinted from jinse

12/21/2024·5MWritten by: 0xjs@金财经

"Of The People, By The People, For The People" is the most famous speech by US President Lincoln.

"Of the people, by the people, for the people" is the slogan of Dr. Sun Yat- sen's Three People's Principles.

Once these ideas were put forward, they firmly occupied the people's minds.

In the crypto industry, the same is true for "user sovereignty and community ownership." Crypto projects that do not consider users and communities due to various factors such as first-mover advantage will encounter challenges sooner or later.

During the two-day decline, Usual, a stablecoin protocol targeting USDT/USDC, performed well and attracted the attention of the crypto community.

What is Usual?

According to official documents, Usual is a secure and decentralized fiat stablecoin issuer, aggregating growing RWA tokens (mainly tokenized U.S. Treasury bonds) from Hashnote, BlackRock, Ondo, Mountain Protocol, M^0, etc. , converting them into a permissionless, on-chain verifiable, composable stablecoin USD0. And redistribute ownership and governance rights through the governance token USUAL.

It can be summed up in one sentence, Usual wants to be the on-chain Tether that issues coins.

Usual targets two key issues with USDT/USDC: user ownership and bank bankruptcy risk.

1. User ownership. USDT and USDC are the two largest stablecoins by market capitalization, with USDT having a market capitalization of over US$140 billion and USDC having a market capitalization of over US$42 billion. According to data disclosed by Tether, the issuer of USDT, Tether’s annual profits in 2024 can reach US$10 billion. Circle's annual profits can reach $3 billion. However, all the profits generated by the assets provided by these crypto users were taken away by Tether and Circle, and the users did not have any rights. Usual will not privatize the profits generated by USDT and USDC like Tether and Circle, but will redistribute power and benefits to the community (Of The People, By The People, For The People). 100% of the revenue from the Usual protocol flows into the treasury, 90% of which is distributed to the community through governance tokens.

2. Bank bankruptcy risk. A large part of USDT and USDC is guaranteed by commercial banks. This part brings security and stability risks due to banks' partial reserves. Usual has introduced a new stablecoin issuance method. The underlying assets of its stablecoin are 100% collateralized by short-term U.S. Treasury bonds. It is not linked to the traditional banking system and is far away from the risk of bank bankruptcy.

Usual mainly targets the two gaps of Tether/Circle.

In other words, Usual can be described as a "vampire" attack on USDT/USDC, just like Sushi's "vampire" attack on Uniswap in the DeFi Summer of 2020.

So how does Usual implement it?

Analysis of Usual working mechanism

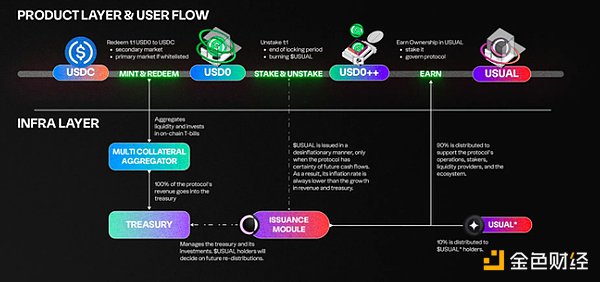

Usual mainly consists of five core tokens: stable currency USD0, LST token USD0++, governance token USUAL, pledged governance token USUALx and founding token USUAL* .

USD0: USD0 is Usual’s stablecoin . Users can exchange USD0 through USDC or USYC at a rate of 1:1.

USD0++: LST tokens generated by USD0++-style USD0 pledge . Holding USD0++ can get USUAL token incentives.

USUAL: USUAL is Usual’s governance token .

USUALx: USUALx can be obtained by staking USUAL . Users holding USUALx can activate governance rights and obtain USUAL rewards. USUALx can conduct voting governance of the Usual protocol, such as the source of collateral for future support.

USUAL*: USUAL* is the founding token of the Usual protocol , allocated to investors, contributors, and advisors, and is given different privileges from the USUA token.

The following figure is a schematic diagram of Usual’s product and user processes:

This is discussed below.

Minting of USD0

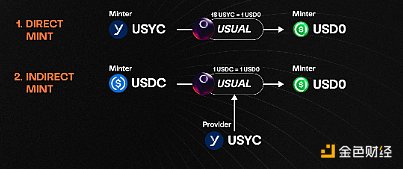

USD0 tokens can be minted through Usual in two ways:

Direct Minting: Earn equivalent USD0 at a 1:1 ratio by depositing eligible RWA into the protocol.

Indirect minting: By depositing USDC (Note: Usual temporarily supports USDC and can be expanded to USDT in the future) into the protocol, USD0 is received at a 1:1 ratio. In this method, a third party called a Collateral Provider (CP) provides the necessary RWA collateral, allowing users to obtain USD0 without directly holding RWA. At the beginning of the protocol launch, all orders below 100,000 USD0 will be redirected to secondary market liquidity.

The above figure takes USD0’s first collateral source USYC as an example. Currently, Usual’s first collateral comes from Hashnote’s USYC . USYC is the on-chain representative of Hashnote International Short Duration Yield Fund (SDYF). SDYF mainly invests in reverse repurchases and short-term U.S. Treasury bonds.

USD0++

USD0++ is the Liquid Staked Token (LST) of USD0. It is a composable token that represents pledged USD0 and functions like a liquid savings account. For every USD0 staked, Usual mints new USUAL tokens and distributes them to users as rewards.

The pledge period of USD0++ is 4 years, and users can cancel the pledge in advance at any time or sell USD0++ on the secondary market at the current price. Users who cancel their pledge early will need to destroy their accumulated USUAL earnings. A portion of the destroyed USUAL will be distributed to USUALx holders.

USD0++ has two parts of income: 1. USUAL token incentives, USD0++ holders can receive daily USUAL token income; 2. Basic interest guarantee, USD0++ holders can obtain income at least equivalent to USD0 collateral income (risk- free) income). But users must lock their USD0++ for a specified period of time. At the end of this period, users can choose to claim their rewards in the form of USUAL tokens or USD0 in risk-free earnings.

USUAL

USUAL serves as the main reward mechanism, incentive structure and governance tool. The core concept of its design is that USUAL tokens are actually minted as proof of income and are directly tied to the income of the protocol treasury. USUAL allocates daily and distributes it to different categories of participants.

USUALx

USUALx is the pledge form of USUAL. Holding USUALx can activate governance rights and obtain 10% of the total newly issued USUAL, thereby promoting USUAL currency holders' long-term participation in the Usual ecosystem. Users can unstake USUALx at any time, but they need to pay 10% of the unstaking amount .

USUAL*

USUAL* is the founding token of the Usual protocol, allocated to investors, contributors, and advisors to fund the creation of the protocol, and is endowed with specific rights that are different from the USUAL token, but it has no liquidity.

USUAL currency holders have two main permanent rights:* 1. USUA token distribution rights: USUAL* currency holders are entitled to receive 10% of all USUAL tokens minted, and the remaining 90% is distributed to the community. 2. Fee distribution rights: USUAL* holders will also receive one- third of all fees generated by USUALx staking withdrawal.

USUAL* holders are granted majority voting rights in the early stages of the protocol to ensure compliance with the roadmap and facilitate effective decision-making during the launch phase. Over time, governance will transition to a decentralized model centered on USUALx. However, this transition will not affect the permanent economic rights of USUAL* holders.

From the above, it can be seen that USD0++, USUALx, and USUAL are closely related to the issuance and emission distribution of USUAL.*

Through the distribution of USUAL, it not only incentivizes users to exchange USDC for USD0 and pledge it into USD0++, but also incentivizes users to pledge the USUAL tokens into USUALx. It also gives USUAL* a 10% USUAL incentive to benefit Usual’s team, VC and community. Long term binding.

Exquisite USUAL token issuance and distribution mechanism

USUAL’s token issuance adopts a different strategy from other crypto projects, mainly in its token issuance and distribution mechanism.

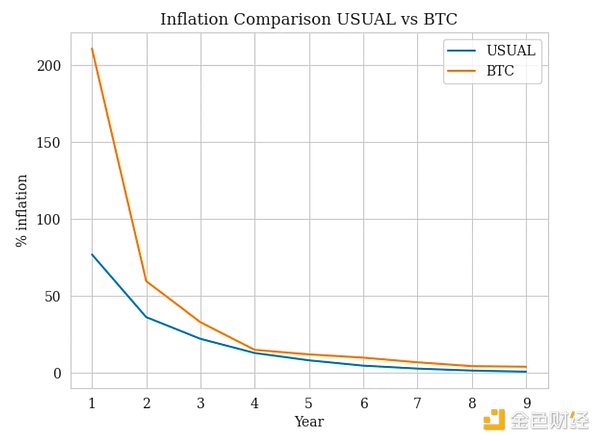

Let’s talk about token issuance first. The maximum supply is 4 billion USUAL within 4 years. USUAL adopts a dynamic supply adjustment emission mechanism, and the emission rate is adjusted based on TVL growth denominated in USD0++ and interest rate changes in supporting USD0 assets, and a cap is set to prevent excessive issuance. As the supply of USD0++ increases, the minting rate decreases, which helps create scarcity and reward early participants.

Usual's issuance model is designed to be deflationary, and the inflation rate of USUAL is lower than that of Bitcoin. The inflation rate is calibrated to stay below protocol revenue growth, ensuring that token issuance does not exceed the protocol’s economic expansion rate.

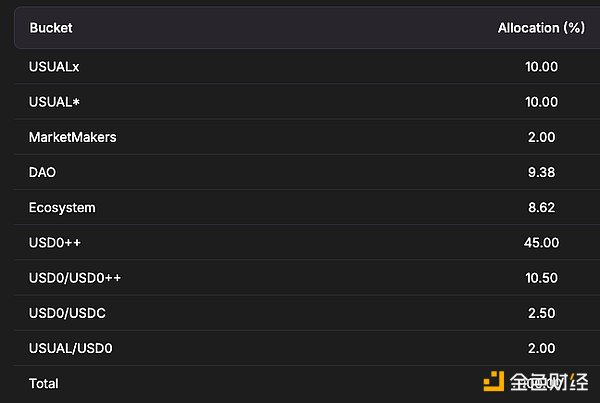

Let’s talk about distribution. The picture below shows the USUAL allocation:

As mentioned in the previous section, USUAL* is a special token model designed by the team and VC. Through two permanent economic rights, insiders such as the team, VC, and consultants can obtain 10% of the USUAL issuance, and within 4 years it will be shared with the entire community. Obtained simultaneously and locked in the first year. The remaining 90% is fully allocated to the Usual community.

The result of this design is that USUAL avoids becoming the widely criticized low-circulation high FDV VC token, ensuring the consistency of interests of the team, VC and community.

At the same time, USUAL token issuance is linked to protocol revenue, and its supply increases with the growth of protocol revenue. Therefore, unlike other DeFi project VCs and early adopters who quickly sell tokens, Usual’s token model incentivizes long-term holders.

Where does Usual’s super high income come from?

One of the reasons for USUAL's recent rapid development is its ultra-high earnings.

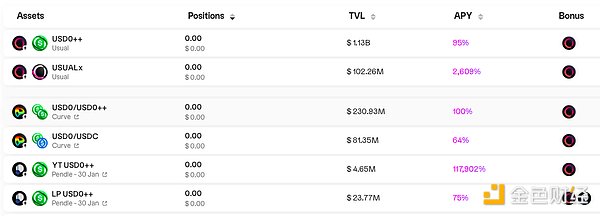

On December 20, 2024, the APY of USD0++ reached 94%, and the APY of the pledged token USUALx of the governance token USUAL reached 2200%, and their corresponding APRs were 66% and 315% respectively. On December 19, 2024, the APY of USUALx was as high as 22,000%, and the corresponding annualized return APR was 544%.

Where does this high income come from?

Currently, Usual’s first collateral comes from Hashnote’s USYC. USYC is the on-chain representative of Hashnote International Short Duration Yield Fund (SDYF). SDYF mainly invests in reverse repurchases and short-term U.S. Treasury bonds. According to Hashnote’s official website, in the past five months, USYC’s total revenue has been only 6.87% .

Obviously, the income from the underlying assets is not enough to support the ultra-high income of USD0++, USUALx and related LP on Curve and related LST on Pendle. Their high income mainly comes from the incentives of USUAL tokens.

Conclusion: Usual flywheel

Stablecoins are the killer application for encryption. As U.S. regulations become clearer after Trump takes office, the prospects for the stablecoin market are broader. The stablecoin market in 2025 is likely to reach trillions of dollars.

According to Usual's plan, Usual will also diversify USD0 assets in the future, and future collateral will come from other U.S. debt RWA projects such as BlackRock and Ondo. With the relaxation of U.S. regulations, U.S. bonds on the chain will surely develop on a large scale in 2025. According to data from the U.S. Treasury Department, the size of short-term U.S. debt exceeds $2 trillion. Usual’s RWA collateral market may be comparable to Tether in 2025.

From the above analysis, we can see that Usual targets real problems (Tether on the currency issuance chain, short-term US debt), and forms the Usual flywheel through exquisite token economics design (USD0, USD0++, USUAL, USUALx and USUAL*):

Usual stablecoin market expectations - > USUAL price rises -> high yield -> mint USD0 in large quantities and pledge USUAL -> protocol revenue increases, USUAL locked up and minting decreases -> USUAL scarcity -> USUAL price rises ——>High yield——>Minting USD0 in large quantities and pledging USUAL——>Usual stablecoin market share increases.

The Usual flywheel is already spinning. Since USUAL was listed on Binance, the market value of its stablecoin USD0 has increased by nearly US$1 billion in less than one month and currently reaches US$1.38 billion .

panewslab

panewslab