The truth behind the data: the capital battle between consumer-grade applications vs infrastructure

Reprinted from panewslab

04/10/2025·2M

Original text: Robert Osborne , Outlier Ventures

Compiled by: Yuliya, PANews

Many people may have misunderstandings about Web3 financing. Within the industry, the tug-of-war between infrastructure projects and consumer-facing projects has become one of the longest discussions. According to a post on X by Claire Kart, chief marketing officer of Aztec Network, infrastructure projects appear to be overly favored in the Web3 industry.

Figure 1: Claire Kart, Chief Marketing Officer, Aztec Network

But things are often not what they seem. What if the venture capital preferences we thought were actually wrong? What if, in fact, consumer projects are the ones that benefit more?

Web3 Financing: Defining the Problem

In the venture capital field, it is generally believed that infrastructure projects have received high attention from investors and that “infrastructure” seems to dominate the venture capital market, resulting in shortage of funding for consumer projects.

Figure 2: Hira Siddiqui, founder of Plurality Network

In this kind of discussion, the basic concepts need to be defined first. Perhaps the arguments and frictions between the two sides are partly due to confusion of "consumer projects" and "infrastructure projects". The following are the definitions of these two types of projects.

- Consumer Projects : These projects are designed to interact directly with end users and provide tools, services or platforms that meet individual or retail needs. Consumer projects usually focus on improving user experience, providing financial services, promoting entertainment, enhancing community participation, etc. The end users are the main consumer groups for these projects. These solutions are often easier to use, prioritizing the immediate needs of individuals or businesses without requiring users to have too much technical background.

- Infrastructure projects : These projects are the basis of decentralized systems, focusing on building core technical levels that support secure, scalable, and interoperable networks. They include blockchain protocols, verification systems, cross-chain interoperability and other technologies to support the operation of other applications and services. Deep infrastructure is often invisible to end users, but is crucial to the performance and reliability of the entire system. These projects are mainly aimed at developers, node operators and those responsible for the maintenance and expansion of blockchain systems.

According to Messari's fundraising data, industry project classification does not need to be redefined and can be directly applied to existing frameworks.

Consumer applications include: consulting and consulting services, cryptocurrency, data, entertainment, financial services, governance, human resources and community tools, investment management, markets, meta-universe and games, news and information, security, synthetic assets, and wallets.

Infrastructure projects include: network and web services, node tools, cross-chain interoperability, networks, physical infrastructure networks, computing networks, mining and verification, developer tools, and consumer infrastructure.

It should be noted that the boundaries of the category of "consumer infrastructure" are relatively blurred. It is a framework that supports user-oriented applications, but is not necessarily directly visible. For the purposes of this article, “consumer infrastructure” will be considered an infrastructure project.

The meaning of a debate

Why is this debate so important? Why do founders and investors feel the need to draw a line on this issue? Recently, Boccaccio from Blockworks, Mike Dudas from 6th Man Ventures and Haseeb Qureshi from Dragonfly briefly explored the issue in a panel discussion at the 2025 New York DAS conference, but a brief exchange between the three was not enough to solve the issue.

Figure 3: New York Digital Assets Summit, “Is venture capital still important?” , Boccaccio (left), Haseeb Qureshi (middle), Mike Dudas (right).

Infrastructure supporters believe that they are the future "invisible architects" on the chain, and that digital railways must be laid before consumers can move forward at high speed. Without sufficient scalability to deal with the surge in traffic and lack of strict security protection to prevent attacks and vulnerabilities, widespread adoption can only be empty talk. As Haseeb Qureshi said in the panel discussion: "Have we built a blockchain? Is this the final form? If we want more than 10 million people to use public chains, we are not done yet."

Figure 4: Antonio Palma

Through investment in technology research and development, the goal is to simplify the construction process, reduce friction between the next dApp creators, and ultimately achieve extensive interaction between blockchain and users. This is not only a short-term bet, but a long-term plan: build infrastructure and pave the way for the smooth delivery of powerful consumer dApps.

On the other hand, supporters of consumer projects criticized existing systems for their serious preference for infrastructure projects, and even the most successful consumer applications were considering turning to infrastructure: Uniswap is building a modular AMM framework, Coinbase has launched its own L2, and even social applications like Farcaster have begun to position themselves as social protocols.

Figure 5: JokeRace co-founder David Phelps

As Mike Dudas said in the panel, the current market structure means that infrastructure projects are by default "darling" in the eyes of venture capitalists, although the actual liquidity involved in these projects is not high.

Therefore, supporters of consumer projects believe that the role of venture capital is an artificial market distortion: large-scale adoption can be achieved if more capital can be allocated to consumer applications. The cumbersome wallets and complex interfaces are the biggest obstacles to entry, making the most powerful blockchain almost invisible to the public. What can really promote the market is "killer application". Although efficient and safe infrastructure is crucial, no one is willing to buy a ticket if the seat is uncomfortable and the journey is poor.

Figure 6: Gardo Martinez, Senior Product Manager, Story Protocol

The financing structure in the Web3 field has always been dominated by a common assumption: infrastructure projects deserve more capital support. The logic behind this view is that Web3 is still in its early stages of development and the underlying facilities are not yet fully mature, so the market's attention to infrastructure projects will be higher than consumer-oriented applications.

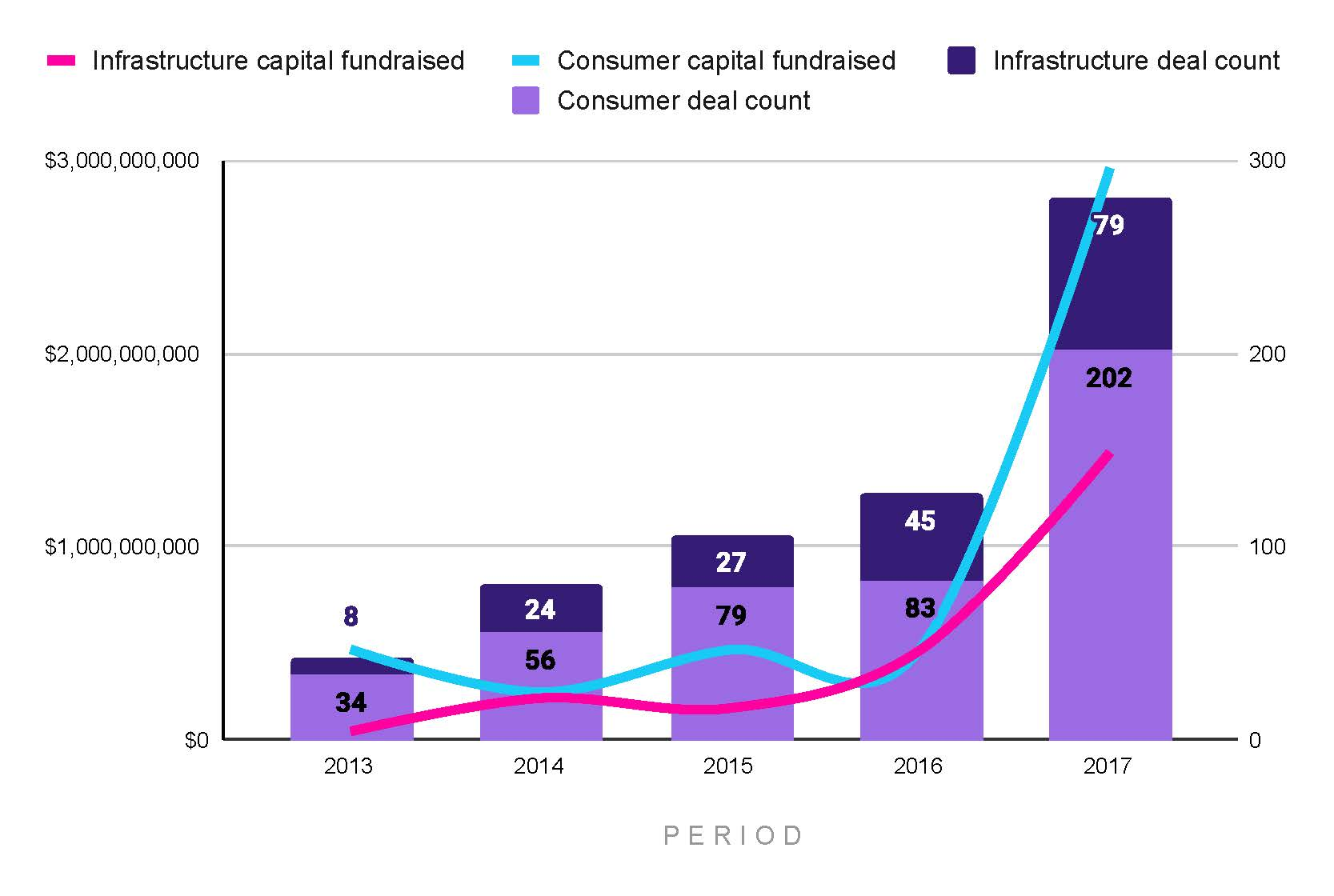

Figure 7: The amount of financing and transactions of consumer goods and infrastructure projects at each stage from 2013 to 2017

However, earlier data reveal another trend (see Figure 7). Starting from 2013, from 2013 to 2017, 72% of financing transactions came from consumer projects, while infrastructure projects accounted for only 33% of the total financing. Although the total financing amount of the two types of projects was once the same in 2014 and 2016, the number of consumer projects successfully raised was still more. It can be seen that although the financing rounds of infrastructure projects were fewer, the single round amount was larger (see Figure 12). By 2017, consumer projects once again dominated Web3 venture capital.

Overall, the capital investment during this period is just a drop in the bucket compared to the scale of subsequent years and cannot constitute the core support of the Web3 ecosystem. It is also precisely because of the limited data sample, the analysis at this stage is independent of the main discussion. From 2018 to 2024, a large amount of capital was pouring in, and early venture capital interest was just a drop in the ocean.

Even so, these preliminary data raise some key questions: Do infrastructure projects really get more financial support than consumer projects? Is people’s perception based on a wrong premise?

Do you have a preference for consumer projects?

Looking at the Web3 financing data from 2018 to 2024, there has been a trend of infrastructure projects gaining additional attention recently, but consumer applications are favored by more investors.

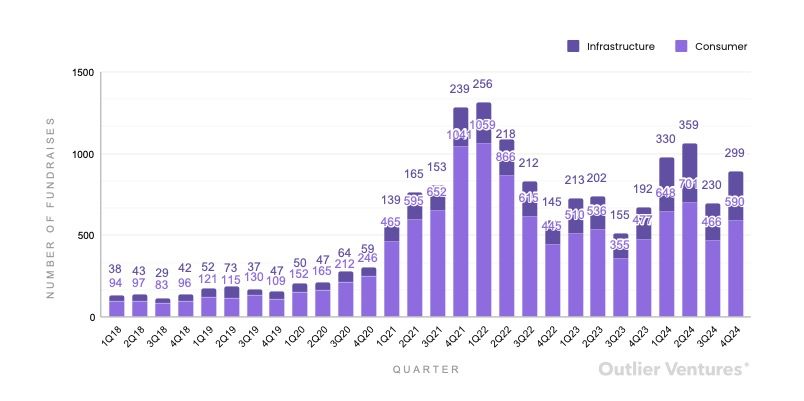

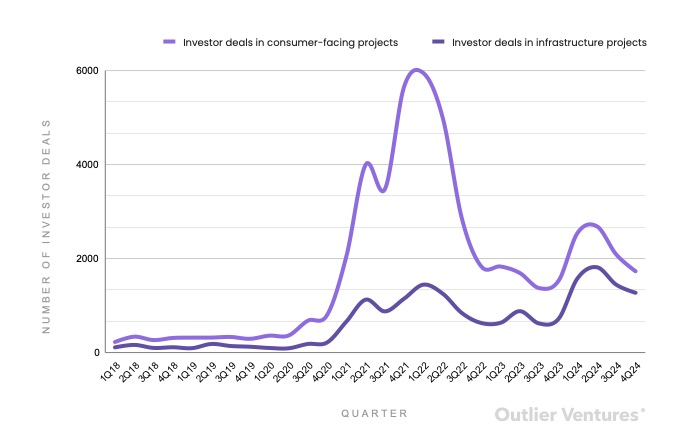

Figure 8: Total financing projects in infrastructure and consumer product categories divided by quarter from 2018 to 2024

From 2018 to 2024, consumer applications accounted for 74% of all financing transactions. Even in 2023 and 2024, consumer applications still account for 68% of all financing transactions (see Figure 8).

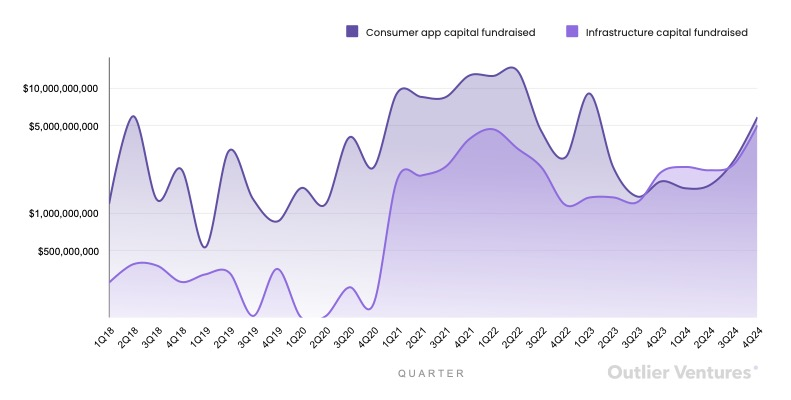

However, in terms of the total financing amount, the fate of infrastructure

projects has changed. From 2018 to 2020, infrastructure projects lag behind

consumer applications, with only 11% of capital flowing to infrastructure

projects. This trend began to change in 2021, although consumer projects still

account for the majority of financing. Infrastructure projects accounted for

19% of financing capital in 2021 and 2022, while this proportion reached 25%

and 43% in 2023 and 2024, respectively (see Figure 9). In fact, from the

fourth quarter of 2023 to the second quarter of 2024, infrastructure projects

surpassed consumer projects in total financing.

Figure 9: Total financing of consumer goods and infrastructure projects in each quarter from 2018 to 2014

Another dimension worth paying attention to is investor participation. Although there is a view that most investors prefer infrastructure investment, judging from the 2018-2024 data, the number of investors participating in consumer projects has always been higher. Especially between 2021 and 2022, 79% of investor transactions appear in consumer projects (see Figure 10).

Figure 10: Total number of investor transactions in consumer and infrastructure project categories quarterly from 2018 to 2024

Although the influx of capital for consumer projects lags in the early stages of the epidemic, this is consistent with the usual 6 to 9-month financing cycle. The epidemic lockdown has prompted a craze for consumer applications in Web3 by pushing people to turn their attention and disposable income online.

However, the craze did not last. The market crash in the second quarter of 2022 is widely believed to be triggered by Terra/Luna's collapse in May. When UST deaned the anchor, the market value instantly evaporated by more than US$40 billion, triggering a chain reaction. Large funds such as Three Arrows Capital and Celsius have successively burst, and the vulnerability of the DeFi system has been exposed. Coupled with macro pressures such as rising inflation, rising interest rates, and tightening liquidity, the entire crypto market is in crisis. FTX's bankruptcy in November 2022 further exacerbated the collapse of market confidence.

From the perspective of venture capital, the rebound in the crypto market at the end of 2023 and 2024 did not simultaneously transmit to the VC market. The reason is that the market is still in the "hangover" stage after the consumption boom during the epidemic. The investment returns between the fourth quarter of 2020 and the fourth quarter of 2023 did not meet expectations, revealing the premature investment of consumer investment and the immaturity of encrypted VCs. Although the number of investor transactions in consumer projects remains ahead, the gap between infrastructure projects and consumer projects has narrowed significantly. In 2024, infrastructure projects account for 40% of the number of investors' transactions.

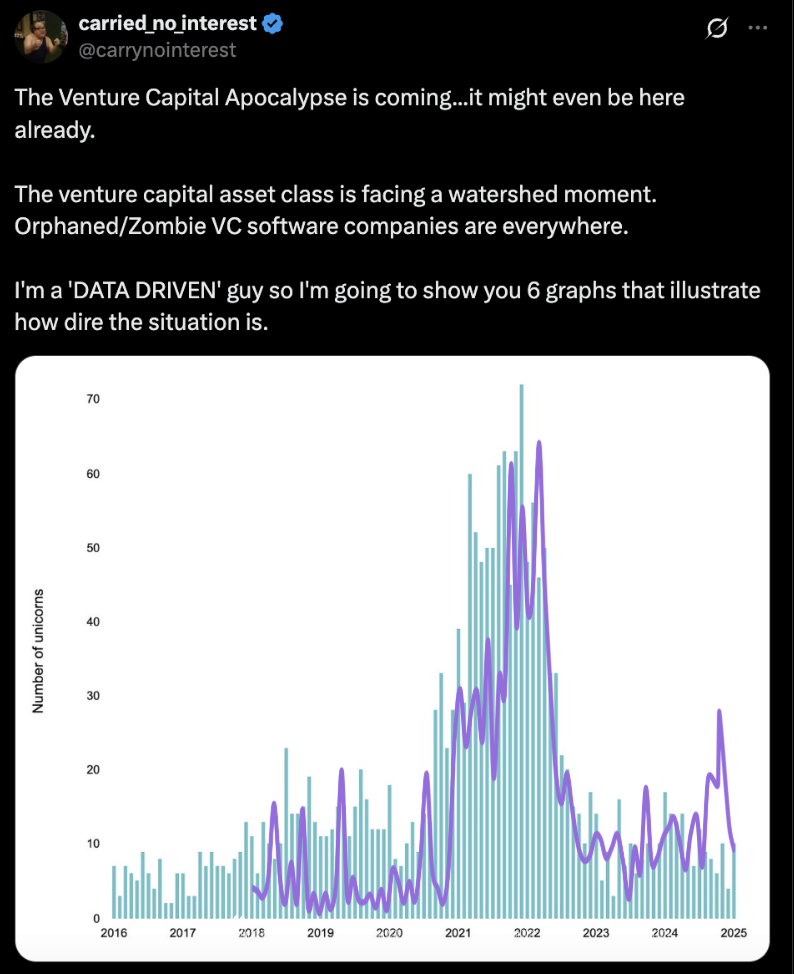

This is not a phenomenon unique to Web3. Between 2020 and 2021, a large amount of capital poured into the traditional VC market. Private equity investor "@carrynointerest" pointed out that capital mismatch at this stage will lead to a long-term wave of VC failures. The lack of mergers and acquisitions exit, rising interest rates, and declining software valuations have made a large number of VC-backed companies "orphans" or "zombie" companies.

If the total amount of Web3 financing is compared with the number of

traditional VC unicorns, the trends of the two are highly similar (see Figure

11). As shown in Figures 8, 9, 10 and 12, consumer projects occupy capital and

transaction share for a long time. The failure of VC in the Web3 field is

essentially a failure of consumer projects. Based on this understanding,

investors should turn their focus to infrastructure.

Figure 11: The number of startup unicorns between 2016 and 2025, and the total amount of funds raised by Web3 consumer and infrastructure projects

But in reality, the adjustment range of capital allocation to consumer projects is still limited. This is closely related to the financing mechanism of Web3. Unlike traditional equity, the token-based financing mechanism can achieve partial exit before the project is implemented, allowing investors to achieve certain returns even in the face of failed projects.

In addition, due to the longer development cycle and higher requirements for protocol security and token economic model, Web3 infrastructure projects often adopt longer locking and unlocking mechanisms. Its tokens usually assume core roles in the network operation (such as staking or governance), so short-term centralized unlocking must be avoided. In contrast, consumer projects pursue market speed, user growth and early liquidity, and often design shorter lock-up cycles to quickly capture market heat and speculative demand.

This structural difference brings about the cycle of capital: the early liquidity brought by a consumer project will feed back to the next project, thereby continuously promoting investment in the track and buffering the impact of failure. Because of this, the Web3 VC market has to some extent circumvented the drastic corrections experienced by traditional VCs.

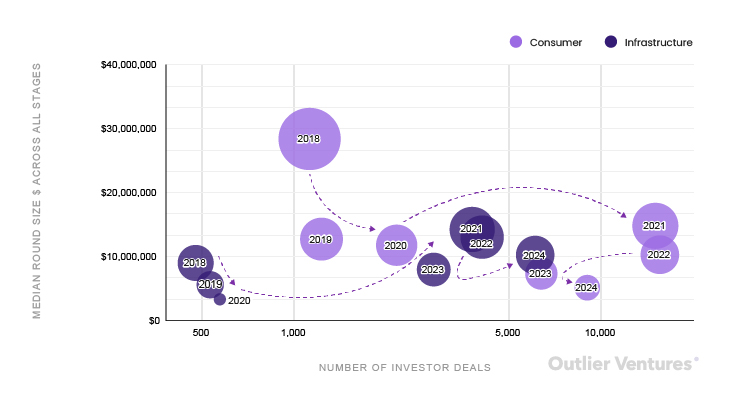

As a supplementary indicator, the total financing amount can be combined with the number of financing transactions, the median round scale of consumer and infrastructure projects can be calculated, and the financing paths of both are depicted in combination with the number of investor transactions (see Figure 12).

Figure 12: Median financing rounds of consumer goods and infrastructure projects at each stage from 2018 to 2024 and their corresponding annual investor transactions

- From 2018 to 2020, consumer projects will dominate the market. The median financing scale of the two types of projects was close for the first time in 2021 (USD 14.8 million in consumer categories and USD 14.2 million in infrastructure), but the number of investors in consumer projects is still four times that of infrastructure.

- Starting from 2022, the median infrastructure round surpassed the consumer category for the first time ($13 million vs $11 million) and continued until 2024.

- In 2024, the median financing scale of infrastructure projects is twice that of consumer projects.

Despite the increasing scale of infrastructure financing, the number of investor transactions in consumer projects remains the leading position. In 2024, the number of investors in this type of project will be 50% more than the infrastructure. This shows that consumer projects are rich and still attractive (see Figures 9 and 10).

Risk preference index

In order to more systematically measure venture capital preferences, the "Risk Preference Index" (see Figure 13) was introduced in the study. This index integrates the proportion of capital, transaction volume and investor proportion, with a score range of 0 to 1, with 0.5 being a neutral value. The weights of the three indicators are: capital account for 50%, transaction quantity accounted for 30%, and investors accounted for 20%. Among them, the proportion of capital is the strongest signal, representing high due diligence and strong expectations; the number of transactions reflects the market breadth, but the scale of a single transaction varies greatly; the number of investors reveals the market popularity, although the signal-to-noise ratio is relatively low.

So far, the index has not seen infrastructure projects score higher than consumer projects. The closest time was in the first quarter of 2024, when the infrastructure scored 0.48. In essence, this index can be regarded as a weather vane for VC confidence.

Figure 13: Risk preference score

Rethinking on the capital allocation of Web3 financing

There is no "correct" answer to the financing ratio of consumer to infrastructure projects, because it depends on market maturity, phased demand and environmental changes. In emerging technology ecosystems such as Web3, it is a natural phenomenon that infrastructure projects attract a large amount of capital in the early stages. The infrastructure layer takes longer to build and there is often a “winner-take-all” dynamic, which makes large-scale concentrated investment a reasonable choice. Infrastructure unlocks scale, performance and security, all of which are prerequisites for large-scale adoption of consumers. In this context, it seems reasonable to venture capital lean towards infrastructure.

However, the data reveals another story. Venture capital has always favored consumer projects, and the market acts as if infrastructure issues have been resolved, at least for now.

This mismatch raises important questions. Is the industry turning its attention to consumer applications too early without adequately testing the infrastructure? Have we paid too much attention to short-term liquidity in capital allocation and ignored long-term stability? Or, have we underestimated the existing maturity of infrastructure and instead ignored the user experience level that will drive mass adoption?

These are not binary choices, and in Web3, capital allocation should reflect the true maturity of the ecosystem, not the state we want it to achieve. The future path is not about being biased to one side, but about recalibrating confidence and reality.