Solana inflation revolution: SIMD-0228 proposal triggers community controversy, with 80% reductions in additional issuances hidden risk of "death spiral"

Reprinted from panewslab

02/27/2025·2MAuthor: Frank, PANews

Recently, the Solana Governance Forum launched a proposal called SIMD-0228, which will reduce the annual additional issuance of SOL by 80% by dynamically adjusting the inflation rate and guide funds from pledge to DeFi. However, this seemingly "smart issuance" blueprint has aroused fierce controversy in the community about the "inflation spiral" and the game of interest - when the pledge rate falls below the critical point, higher inflation may backfire market confidence. The income structure of the verifier and the distribution of interests of ecological participants have become the invisible explosives of this token economic experiment.

New proposals may reduce inflation by 80% and reduce SOL issuance by 22

million that year

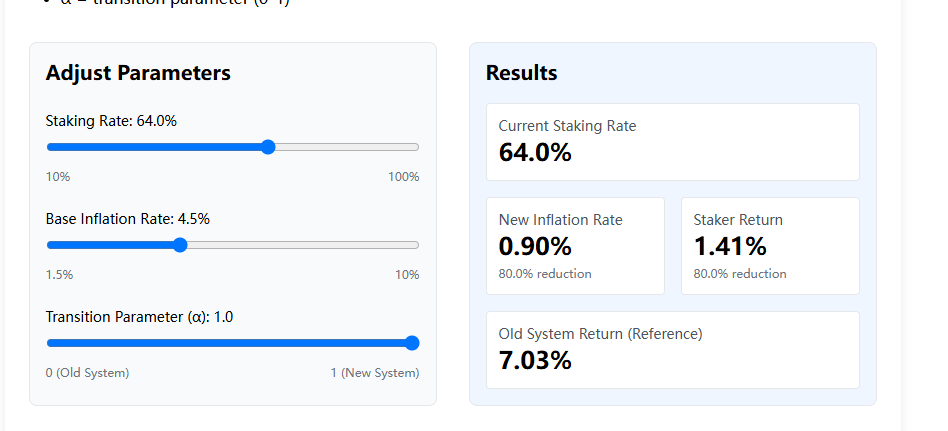

Solana's token SOL issuance mechanism has always adopted a fixed timetable mechanism, that is, the inflation rate drops from 8% to a decrease of 15% per year over time until it reaches the 1.5% target, and the current inflation rate is 4.694%. Under this inflation rate mechanism, the number of additional tokens issued this year is about 27.93 million tokens, and the pledge rate is about 64%.

In contrast, Ethereum's inflation rate is currently about 0%, and its pledge rate is about 30%. The inflation model of SOL tokens is obviously more unfavorable to token preservation, and the excessive inflation rate also allows a large number of tokens to choose to be pledged to obtain higher yields. Therefore, it is not conducive to the development of the DeFi ecosystem.

The proposal believes that in the Solana network, MEV revenue has become the main source of income for validators, and reducing the pledge yield will not have much impact on the return. “In simple terms, it’s a 'silly issuance’. Given Solana’s booming economic activity, it makes sense to develop the monetary policy of the network to achieve 'smart issuance’.”

In the proposal, a dividing line is proposed, which is assumed to be 50%, that is, when the pledge rate exceeds 50%, the inflation rate will drop, reducing the pledge income of the network. When the pledge rate is less than 50%, the inflation rate is increased and the rewards are expanded to incentivize more funds for pledge.

Subsequently, forum users questioned the lack of rigorous calculation basis for the 50% threshold and believed that the setting was too hasty. The proposer then provided a new algorithmic curve, setting the pledge rate of 33% as a dividing line, and when the pledge rate is higher than 33%, the annual inflation rate will be lower than the current inflation rate.

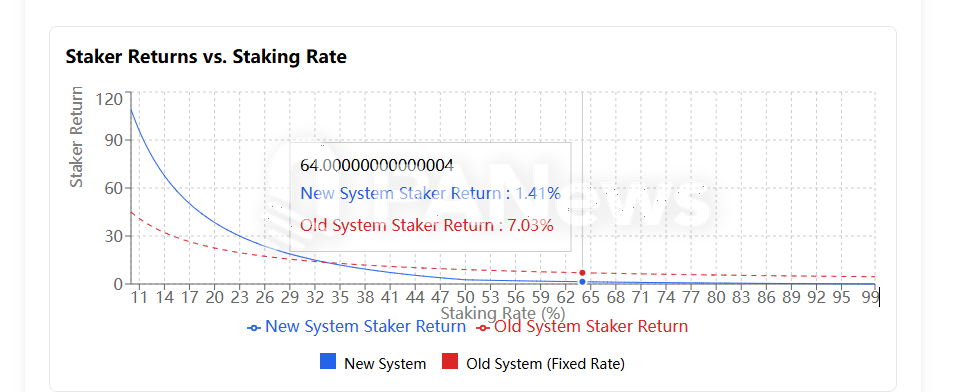

According to PANews calculations, taking the current 64% staking rate as an example, according to the new token issuance curve, the annualized inflation rate will drop from 4.694% to 0.939%, a decrease of about 80%.

If the proposal is finally passed and the current pledge rate is maintained, the number of additional issuances of SOL that year will drop from 27.93 million to 5.59 million.

Pledge rate and inflation rate for proposal modification

However, this statement in the proposal does not seem to be reached in the forum, and a large number of comments believe that if the plan is passed, the reality may not happen as ideally. For example, when the pledge rate drops, the rise in inflation will further reduce the market's expectations for tokens, which may lead to further selling of tokens by those unstaked tokens causing greater uncertainty.

PANews calculated that when the pledge rate is only 25%, inflation of 44.13 million tokens will be generated, which is much higher than the current inflation rate.

If you really fall into this vortex of inflation, then the result may be counterproductive. As the proposal says, the current source of income for validators is MEV income. This phenomenon is mainly because Solana's online transactions are currently active, and the demand for trading speed and anti-sandwich attacks by many MEME players has made MEV revenue account for a high proportion. If the overall network transaction volume declines in the future, the proportion of MEV revenue may be difficult to maintain the main source of income for verifiers. At that time, if the double blow of inflation and price decline was added, it might further dampen the enthusiasm for pledge, and instead move towards a reverse spiral of rising inflation and declining pledge.

The verification giants are collectively silent, and behind it may be the

game of interests of big currency holders

The proposal was initiated by Vishal Kankani, an early investor in Solana who led a $20 million Series A financing in 2019. And hold a large number of SOL tokens, and early investments choose to obtain SOL tokens rather than equity. From this background, Vishal Kankani represents a large Solana coin holder, which is more sensitive to inflation affecting the token market price.

Interestingly, as of February 26, Helius, binance staking, Galaxy and others in the Solana network have not made any statements on this proposal. The founder of Helius often speaks about the development of the Solana ecosystem, but this proposal that has a huge impact on the ecosystem has only forwarded a related content and commented that it is stupid to sell SOL tokens now.

In fact, once this proposal is passed, it may not be good news for Helius, a verifier who returns 100% of MEV revenue to the stakeholder. Because at present, since it does not obtain benefits through MEV, Helius may rely more on the benefits of pledge itself.

Overall, this proposal represents the interests of SOL's large coin holders, and they hope to reduce inflation to achieve value stability. In addition, from an ecological perspective, Solana Network's current pledge yield is about 7.03%. Under the new plan, the yield of the same pledge rate will drop to 1.41%, and the yield will drop by nearly 80%. This is not a good thing for large validator nodes that want to obtain risk-free returns through staking.

Of course, the proposal believes that it is the decline in the staking yield that will stimulate these validators to invest their tokens in more DeFi ecosystems, which can further enhance the ecological prosperity of Solana DeFi.

Solana's token economy reform is essentially a rebalancing of power between large coin holders, verifiers and ecological builders. After the proposal is passed, the 7.03% pledge yield may plummet to 1.41%, forcing validators to shift from relying on inflation rewards to deepening MEV and transaction fees

- this is both an opportunity and a bet.

If DeFi can absorb billions of dollars of idle liquidity, Solana may usher in explosive innovation like Uniswap and Aave; but if the market sells out due to a decline in yields, the 44.13 million yuan of staking rate at the 25% pledge rate may drag the network into the death spiral of "inflation-selling pressure-more inflation".

At present, the silence of top validators such as Helius implies the delicate tension of the interest chain - when the business model of 100% returning MEV is halved, the ecological "decentralized" narrative may face realistic questions. Multicoin Capital's position as an early giant whale reveals the deep logic of this game: in the eyes of institutional investors, SOL's value storage attributes have taken priority over network security needs. In the coming months, with the March 7 vote approaching, Solana's fate will no longer be code dictatorial, but will depend on whether the community can find that dangerous balance between idealism and capital rationality.