SignalPlus Macro Analysis Special Edition: The Xmas Grinch

Reprinted from chaincatcher

12/31/2024·4M

2024 is drawing to a close, and the last few trading days of the year are more important than expected. While the Bank of England and the Bank of Japan kept interest rates unchanged and leaned dovish as expected, the Fed's "hawkish interest rate cut" and technical adjustment to the overnight reverse repurchase rate surprised the market, indicating that liquidity conditions at the end of the year will be Tighten.

In terms of interest rates, although Powell announced a 25 basis point interest rate cut as expected, his statement carried a clear hawkish stance, specifically mentioning the "extent and timing" of future interest rate cuts, which is reminiscent of the moratorium on interest rate cuts in 2006-07. The wording used, Clevent Fed Chairman Hammack also expressed opposition to interest rate cuts and hoped to keep interest rates unchanged, and the Summary of Economic Projections (SEP) dot plot also showed a hawkish stance, with only 5 members believing that 2025 There will be more than three interest rate cuts this year, and the median dot plot predicts only two interest rate cuts in 2025. While economic conditions remain solid, long-term interest rate expectations have also risen to 3.0%.

More importantly, core PCE median inflation also rose to 2.5% (+0.3%) in 2025, and the "inflation risk distribution" rose to 15 (only 3 in September), highlighting the stickiness of inflation in the past quarter. sex. In addition, during the question and answer session at the last FOMC meeting of the year, Powell made it clear that he was "very optimistic" about the economic situation and believed that after cutting interest rates by 100 basis points, the Fed has now entered a new stage where it should "act cautiously". It has a strong meaning of pie.

On the fiscal front, Trump's campaign is expected to increase the U.S. deficit by $7.7 trillion over the next 10 years (CRFB estimates range from $1.7 to $15.5 trillion), which would push the U.S. debt-to-GDP ratio to around 145% by 2035 . The extent of the ultimate inflationary pressure will depend on how much he is able to implement in his second term, and Trump's recent U-turn on the TikTok ban may indicate that the actual implementation of his policies may not be as strong as expected?

Regarding government spending, the current debt ceiling pause is set to expire on January 1, prompting Secretary Yellen to take a series of "extraordinary measures" to create more room for borrowing. The Treasury should have enough emergency funds available through August, according to Wall Street estimates, so the debate over the debt ceiling may not be in the news until after the spring at the earliest.

A series of hawkish news has brought significant negative risk effects. The SPX index fell 200 points, the U.S. bond yield curve showed a steep bearish trend, and the 10-year yield broke through the downward channel and is heading towards the high point of the year. In the past week alone, That's an increase of 15 basis points.

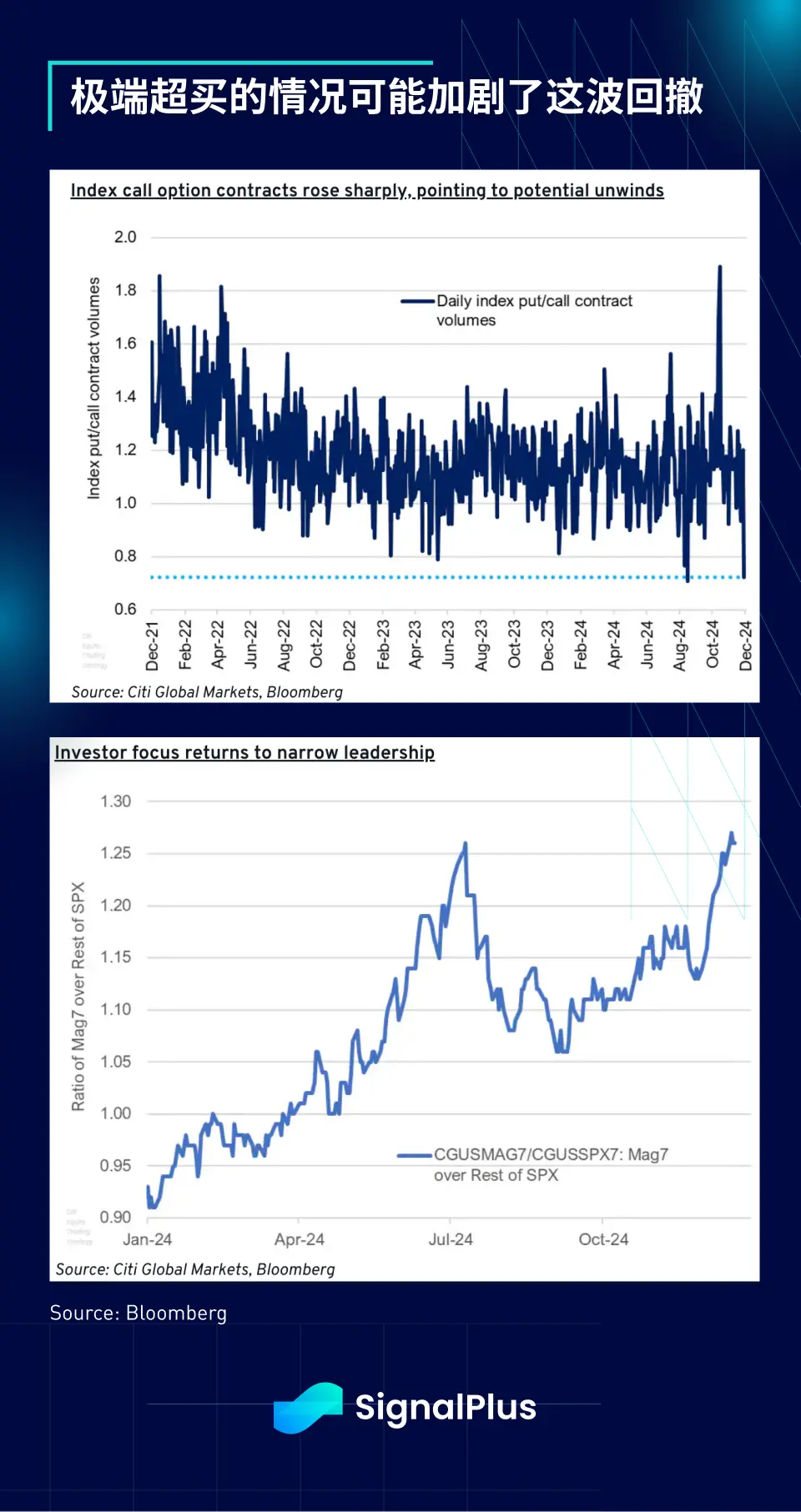

The SPX Index experienced a minor collapse following the FOMC meeting, with the VIX significantly surging, with index options becoming significantly overbought in call options before the sell-off occurred, and the stock market's leading range narrowed to more than July levels, Both may have played important roles in the VIX surge. Under extreme oversold conditions, the stock market has rebounded rapidly to nearly 6,000 points in the past few days, but it remains to be seen whether the market is out of danger.

The so-called "Christmas move" may offer some indication of how risk markets are wrapping up and heading into the New Year. Past data shows that negative performance in the last week is often followed by a sell-off in January. Will the market at the end of the year come again? We'll find out in a few days...

In the field of cryptocurrency, 2024 will undoubtedly go down in history. The market value of cryptocurrency increased by more than 90% during the year, from US$1.65 trillion to US$3.2 trillion. Incredibly, cryptocurrencies are the only asset class to surpass U.S. stocks on a market cap growth basis in 2024, helped by the launch of spot ETFs in January and regulatory optimism following Trump’s election.

The cryptocurrency’s gains this year were initially led by BTC, which saw its dominance rise from a low of 40% to over 60%. Overall, this year's market activity consists of three important phases: in the first quarter, the approval of spot ETFs led to significant gains; in the second and third quarters, market activity was flat and lacked continuation momentum, resulting in sideways trends; and finally, , Trump's re-election has returned altcoins to a dominant force in the market, driving recent gains, with XRP and Dogecoin rising by more than 200% for the year, while other major altcoins have also risen by 150% Or so, which dwarfs ETH’s 40% gain so far this year.

The impact of the mainstream market on cryptocurrencies is best reflected in the high correlation between BTC and the SPX index. By the end of 2024, the SPX index will still be the asset class with the highest correlation with BTC. In addition, Citi’s research shows that ETF inflows can explain nearly half of the fluctuations in BTC’s weekly returns, and this trend is likely to continue into the new year.

In addition, using the market value of stablecoins as an indicator, since Trump was elected, mainstream funds have re-entered the cryptocurrency market on a large scale. The current market value of stablecoins is close to US$190 billion, far exceeding the high point of the FTX period in 2022. At the same time, discussions of BTC reserves among governments have become increasingly popular, with unconfirmed media reports stating that Hong Kong lawmakers recently proposed that the government should consider including BTC in its foreign exchange reserve portfolio.

Another sign that BTC is becoming a mainstream asset class is the continued decline in realized volatility, which will ultimately provide more diversification benefits and excess returns for traditional 60/40 portfolios. Volatility should continue to decline as the asset class matures, with cryptocurrencies following the same path as other asset classes.

Finally, we conclude with an unsolved BTC and M 2 chart. As global liquidity continues to decline, should we remain cautious about BTC's rise? Could continued inflows of new TradFi funds and crypto-friendly regulations in the US lead to a breakthrough change in this correlation? Or will macro factors prevail, allowing skeptics to prove that BTC is simply part of a liquidity performance?

Thank you all for accompanying us through a wonderful 2024, and we look forward to continuing to share more insights on cryptocurrency and macro markets with you in the new year! Happy holidays!

panewslab

panewslab