Safe-haven assets or risky assets? Bitcoin under the shadow of the trade war

Reprinted from panewslab

03/18/2025·3MArticle author: Andrew Singer

Article Compilation: Block unicorn

A few years ago, many in the crypto community described Bitcoin as a “help-haven” asset. Nowadays, fewer and fewer people call it this way.

Safe-haven assets maintain or increase their value during economic pressure. It can be government bonds, currencies like the US dollar, commodities like gold, or even blue chip stocks.

The global tariff war triggered by the United States and disturbing economic reports have already caused stock market crashes, and so is Bitcoin — which should not happen for a "safe-haven" asset.

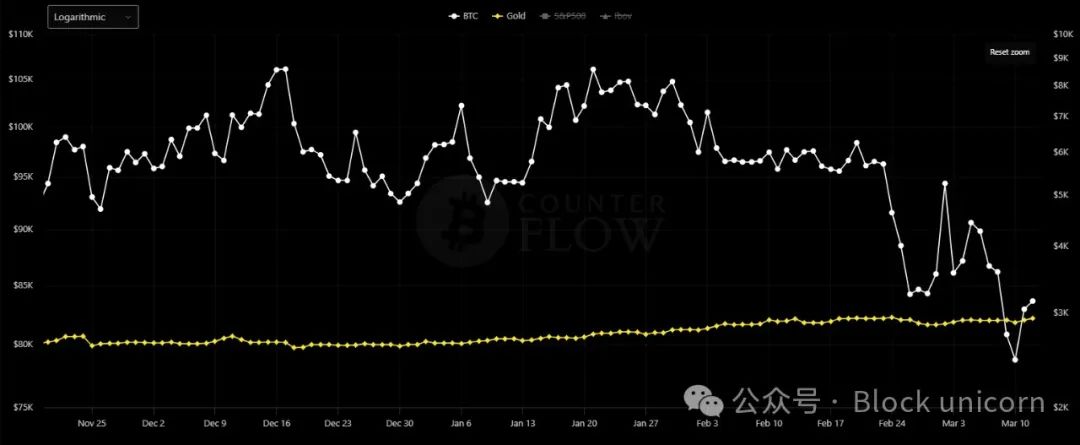

Bitcoin also performs poorly compared to gold. “Since January 1, gold prices have risen +10%, while Bitcoin has fallen -10%,” Kobeissi Letter noted on March 3. “Cryptocurrencies are no longer considered a hedge.” (Bitcoin fell even more last week.)

But some market observers say this is not entirely unexpected.

Bitcoin (white) and gold (yellow) price chart, from December 1 to March 13. Source: Bitcoin Counter Flow

Was Bitcoin a safe haven asset?

“I never viewed Bitcoin as a 'safe-haven asset',” Paul Schatz, founder and president of financial consulting firm Heritage Capital, told us. “Bitcoin’s volatility is too large to be included in the safe-haven category, although I do think investors can and should allocate this asset class in general.”

“For me, Bitcoin is still a speculative tool, not a safe haven asset,” Jochen Stanz l, chief market analyst at CMC Markets (Germany), told us. "Hell-haven investments like gold have intrinsic value and will never be zero. Bitcoin could fall 80% in a big adjustment. I don't think gold will do that."

Cryptocurrencies, including Bitcoin, “never seemed to me that they were ‘help-haven tools’,” Buvaneshwaran Venugopal, assistant professor in the Department of Finance at the University of Central Florida, told us.

But things aren't always as clear as they initially seem, especially when it comes to cryptocurrencies.

One might think there are different types of safe-haven assets: one applies to geopolitical events such as wars, pandemics and recessions, and the other applies to strict financial events such as bank failures or weakening of the dollar.

Perceptions about Bitcoin may be changing. In 2024, exchange-traded funds (ETFs) issued by major asset management firms such as BlackRock and Fidelity have included them, expanding their ownership base but may also change their “narrative.”

Now, it is more widely seen as a speculative or “risk-favorite” asset, similar to tech stocks.

“Bitcoin and cryptocurrencies as a whole have been highly correlated with risk assets, and they often fluctuate inversely with safe-haven assets such as gold,” Adam Kobeissi, editor-in-chief of Kobeissi Letter, told us.

He continued that there is a lot of uncertainty about the future of Bitcoin with “more institutional participation and leverage” and that “the narrative has shifted from Bitcoin being seen as ‘digital gold’ to a more speculative asset.”

One might think that the acceptance of traditional financial giants such as BlackRock and Fidelity would make Bitcoin’s future safer, which would enhance its safe-haven narrative—but according to Venugopal, this is not the case:

“The influx of big companies into Bitcoin doesn’t mean it’s becoming safer. In fact, that means Bitcoin is becoming increasingly like any other asset that institutional investors tend to invest in.”

Venugopal continues, it will be more affected by conventional trading and drawdown strategies used by institutional investors. “If anything, Bitcoin is now more relevant to risky assets in the market.”

The dual nature of Bitcoin

Few deny that Bitcoin and other cryptocurrencies are still affected by large price volatility, with recent increase in cryptocurrency adoption by retail investors, especially driven by the Meme coin boom, “This is one of the largest cryptocurrency entry events in history,” Kobeissi noted. But maybe this is the wrong focus.

“Hard-haven assets are always long-term assets, which means short-term volatility is not a factor that characterizes them,” Noelle Acheson, author of the Crypto is Macro Now newsletter, tells us.

The biggest question is whether Bitcoin can maintain its value to fiat currency for a long time, and it has been able to do that. “The numbers prove their effectiveness – Bitcoin outperforms gold and U.S. stocks in almost any four-year timeframe,” Acheson said, adding:

" Bitcoin has always had two key narratives: it is a short-term risk asset, sensitive to liquidity expectations and overall sentiment. It is also a long-term store of value. It can have both, as we have seen."

Another possibility is that Bitcoin may be a safe-haven asset for some events, but not for others.

Gold can serve as a hedge against geopolitical issues such as trade wars, while both Bitcoin and gold can serve as a hedge against inflation. “So both are useful hedging tools in the portfolio,” Kendrick added.

Others, including Cathie Wood of Ark Investment, also agreed that Bitcoin acted as a safe haven asset during the March 2023 SVB and Signature bank runs. According to CoinGecko, when SVB went bankrupt on March 10, 2023, the price of Bitcoin was about $20,200. A week later, it was close to $27,400, up about 35%.

Bitcoin price fell on March 10 and rebounded a week later. Source: CoinGecko

Schatz does not consider Bitcoin to be a hedge against inflation. The 2022 event, when FTX and other crypto companies went bankrupt and the crypto winter began, “significantly damaged that argument.”

Maybe it is a tool to hedge against the dollar and Treasury bonds? “It’s possible, but these scenarios are quite dark and unimaginable,” Schatz added.

Don't overreact

Kobeissi agrees that short-term volatility in asset classes is “usually minimally relevant over a long-term time frame.” Despite the current decline, many of Bitcoin’s fundamentals remain positive: the U.S. government that supports crypto, the announcement of U.S. Bitcoin reserves, and a surge in cryptocurrency adoption.

The biggest problem faced by market participants is: “What is the next major catalyst to drive the rise?” Kobeissi tells us. “That’s why the market pulls back and consolidation: looking for the next major catalyst.”

“It has been acting like a risky asset since macro investors began to see Bitcoin as a highly volatile, liquid-sensitive risk asset,” Acheson added. Additionally, “almost always short-term traders set the last price and if they are exiting risky assets, we will see weakness in Bitcoin.”

The market is generally struggling. "The reappearance of inflation ghosts and economic slowdowns have seriously affected expectations," which has also affected the price of Bitcoin. Acheson further notes:

“Given this prospect, and the dual nature of Bitcoin as a risky asset and a long-term safe haven asset, I was surprised that it did not fall further.”

Since 2017, Bitcoin has not been a short-term hedging or safe-haven asset, Venugopal said. As for the long-term argument that Bitcoin has become digital gold due to its 21 million supply cap, this only holds true if “if most investors collectively expect Bitcoin to increase value over time” and “this may or may not be true.”

jinse

jinse