In-depth discussion on the key points and impacts of EU crypto asset supervision

Reprinted from panewslab

04/26/2025·18DAuthor: Shen Jianguang, Chief Economist of JD Group; Zhu Taihui, Senior Research Director of JD Group

Introduction

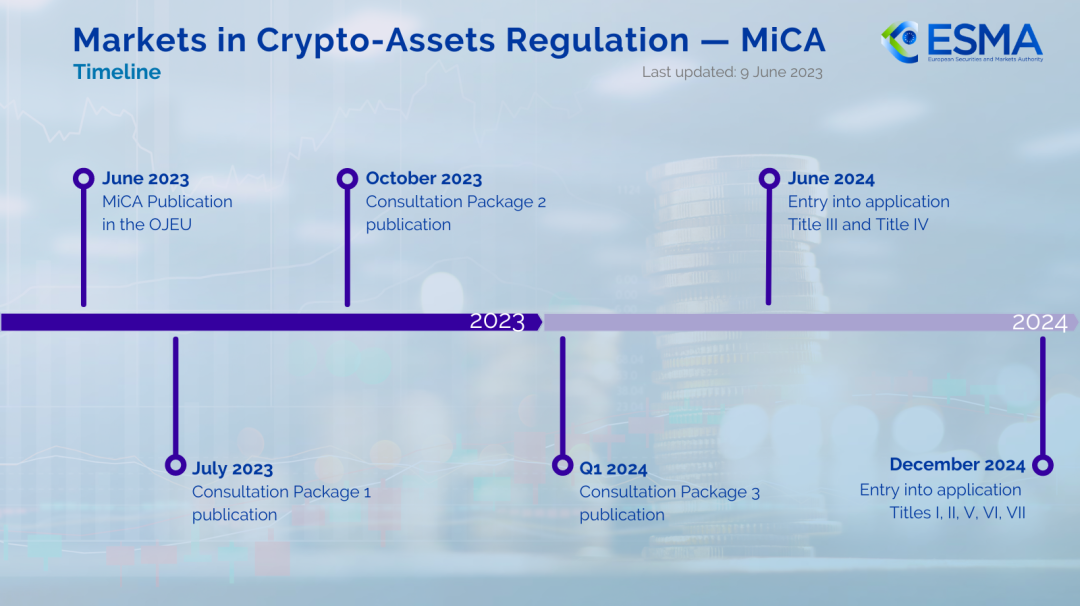

In June 2023, the EU officially issued the Crypto Assets Market Supervision Act (MiCA), which came into effect on December 30, 2024. It applies to 27 EU member states and three other European Economic Area countries (Norway, Iceland, Liechtenstein), solving the fragmentation and regulatory arbitrage problems of cryptoasset supervision by EU and European Economic Area countries. It is the world's largest cryptocurrency regulatory regulation.

According to the idea of classified supervision, MiCA has made detailed provisions on the definition and use of crypto assets, the access license of crypto asset issuers and service providers, the operation and management of crypto asset issuers and service providers, the reserve and redemption management of crypto asset issuers, and the anti-money laundering supervision of crypto asset trading activities. It is by far the most comprehensive crypto asset supervision regulations in the world.

MiCA not only sees the role of the development of crypto assets in improving the efficiency of financial services, improving financial inclusiveness and promoting economic growth, but also pays attention to the challenges brought by the development of crypto assets to the operation of the payment system, the stability of the financial system and the transmission of monetary policy (monetary sovereignty), and has embarked on a balanced path between supporting financial innovation and fair competition, maintaining financial stability and consumer rights. Starting from 2025, as MiCA gradually becomes effective in European countries, it will play a great role in promoting the compliance development of the global crypto asset market, and will also lead the formulation of crypto asset regulatory policies in other countries and the construction of a global governance collaborative system.

1. Classify and define crypto assets and clarify usage and transaction

requirements

1. In terms of asset definition, MiCA divides regulated crypto assets

into three categories

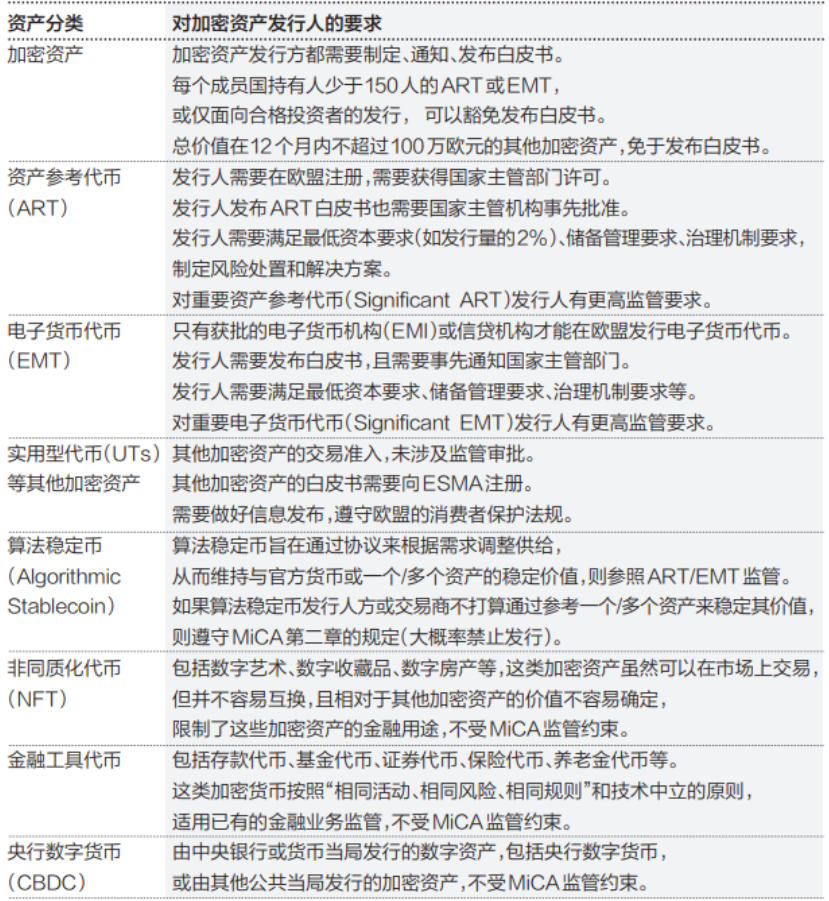

According to whether crypto assets try to stabilize their value by referring to other assets, MiCA divides regulated crypto assets into three categories: electronic monetary tokens (EMT), asset reference tokens (ART), "utility tokens" (Utility tokens, UTs), and other crypto assets, while fully decentralized crypto assets are not regulated by MiCA.

Among them, EMT maintains the value of assets by referring to an official currency (i.e., a stablecoin supported by fiat currency), and is a payment method. The issuer of EMT is prohibited from paying interest (including compensation, discounts, etc., similar to domestic requirements for non-bank payments).

ART is to maintain a stable value by referring to another value or right or a combination of both, including one or more value or rights, commodities, fiat currency or crypto assets. It is a means of trading and investment vehicle. Issuers and service providers should not pay holders interest related to the length of time the ART is held when providing services related to ART.

The difference between EMT and fiat currency-backed ART is the claim right. EMT holders can and have the right to redeem EMT at face value at any time. The redemption time and redemption value of ART holders are not so strongly guaranteed.

Other crypto assets such as UTs are provided with digital access to a certain product or service, provided on distributed ledger technology, and accepted only by the issuer of that token, with non-financial purposes related to the operation of digital platforms and digital services, and are a specific type of crypto assets. In addition, non-fungible tokens (NFTs) and central bank digital currencies (CBDCs) are not within the regulatory scope of MiCA, and securities tokens are not regulated by MiCA, but are regulated in accordance with securities regulations.

Table 1: MiCA's regulatory requirements for crypto assets and their issuers

2. In terms of use and transactions, daily trading volume of crypto

assets and foreign currency stablecoins are set.

MiCA requires that the daily trading volume of a single ART and EMT must not exceed 5 million euros, and the market value of ART and EMT exceeds 500 million euros, the issuer must report to the regulator and conduct additional compliance measures.

MiCA allows the use of EMT (stablecoins) for cryptocurrency transactions and decentralized finance (DeFi) activities, but differentiates EMT for payments for goods and services. Only euro stablecoins can be used for daily payment of goods and services to protect the EU's monetary sovereignty and prevent the development of foreign currency stablecoins from affecting the EU's monetary system.

In addition, MiCA has also strictly restricted the use of ART on a daily basis. When the usage of ART exceeds 1 million transactions or transaction volume of 200 million euros per day (quarterly average), the issuance of this ART must be stopped.

2. Clarify the license requirements of crypto asset issuers and service

providers, and implement classified supervision

1. Implement different access and licensing requirements for the

issuance of different types of crypto assets

MiCA believes that ART may be widely used by holders to transfer value or as a means of exchange, and puts forward stricter requirements on ART issuers to protect the interests and market integrity of holders (especially retail holders).

MiCA clarifies the access authorization requirements for ART issuers: ART issuers must be established as legal entities in the EU and must first obtain authorization from the designated regulatory authority of their home country, and such assets must be traded on a crypto asset trading platform. However, in the case where the ART issuer is already a credit institution, the outstanding ART is less than 5 million euros, and the ART is issued to qualified investors, the access authorization can be exempted.

For the issuer of EMT, MiCA requires that it must be authorized as a credit institution or electronic currency institution and comply with the requirements of the Electronic Currency Directive (EMD2) regarding electronic currency institution. In the absence of EMT amount not exceeding 5 million euros, EMT issuers can also obtain access authorization exemption, but they need to publish a white paper in accordance with regulations.

For crypto asset issuers other than ART and EMT, MiCA's requirements are mainly focused on disclosure rules, but the white papers of these crypto assets need to be registered with the European Securities and Markets Administration (ESMA).

2. Clarify the scope of crypto asset service and the crypto asset

service provider license requirements

MiCA has a broad definition of crypto asset services, mainly covering the following ten aspects of business activities: providing crypto assets custody and management on behalf of customers, operating crypto asset trading platform, exchange of crypto assets and fiat currencies, exchanging crypto assets with other crypto assets, executing crypto asset orders on behalf of customers, and issuing crypto investments, receiving and transmitting crypto asset orders on behalf of customers, providing advice on crypto assets, providing portfolio management of crypto assets, and providing transfer services on behalf of customers.

On this basis, MiCA will classify any individual and entity that provides crypto asset services through commercial means as crypto asset services providers (CASPs). Service providers that intend to provide crypto asset services need to register an office with one of the EU member states and apply for CASP authorization from the competent authorities of the member state where their registered office is located. It should be noted that crypto asset services provided in a completely decentralized and without any intermediary are not covered by MiCA supervision.

3. Clarify the operating requirements of crypto asset issuers and

service providers, and capital supervision is the focus.

1. Make capital supervision the top priority of the business

supervision of crypto asset issuers

MiCA has made clear requirements for the disclosure and honest operation of ART issuers, corporate governance mechanisms, internal control mechanisms, risk management procedures, reserve asset management and redemption, and requires all types of crypto asset issuers to publish white papers (except UT and small cryptocurrencies). For EMT issuers, they need to meet the operating regulatory requirements of electronic currency and payment tool institutions.

At the same time, in order to cope with the impact of the widespread ART issuance that may cause a stability to the financial system, MiCA has put forward specific capital requirements for ART issuers (essentially following the principle of proportional to the scale of ART issuance), and must always have at least the higher of the following amounts: one is 350,000 euros, two is 2% of the average amount of reserve assets/issued tokens as described in Article 32 of MiCA, and three is one-quarter of the fixed indirect expenses in the previous year (if the ART issuer is a credit institution, it complies with the capital regulatory requirements of the credit institution); the capital requirements for EMT issuers are not less than 2% of the scale of EMT issuance circulation, and it also needs to meet the capital regulatory requirements of credit institutions or electronic monetary institutions.

In addition, MiCA also refers to the supervision of "systemically important financial institutions" to evaluate whether ART and EMT are "important crypto assets" from the aspects of customer number, market value scale, transaction scale, and correlation with the traditional financial system, and impose additional risks and own funding requirements on the issuers of important crypto assets.

2. Implement differentiated regulatory requirements for crypto asset

service providers in different scopes

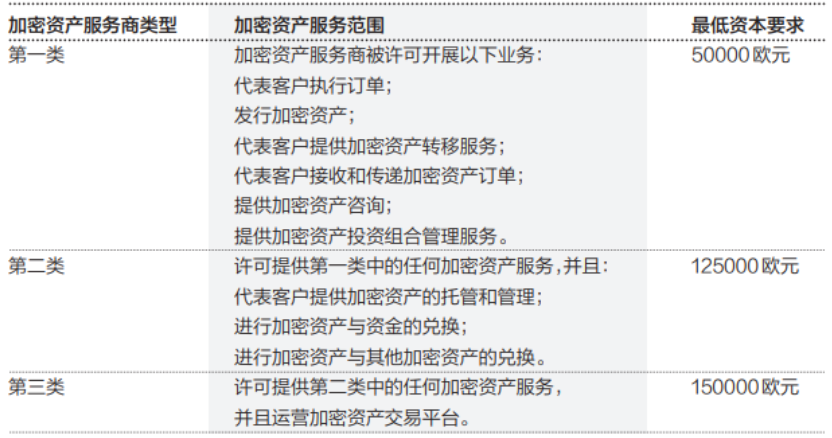

MiCA sets differentiated minimum capital requirements for different types of crypto asset service providers, which are implemented at no less than the following standards or one-quarter of the fixed administrative expenses of the previous year: the minimum permanent capital (own capital) that the trading platform needs to maintain is 150,000 euros; the minimum permanent capital for crypto asset custodians and brokers is 125,000 euros; the minimum permanent capital that CASPs providing other services need to hold is 50,000 euros, and the regulatory requirements are reviewed annually.

At the same time, MiCA also puts forward targeted regulatory requirements for the implementation of different CASPs. For example, MiCA requires crypto asset custodians to formulate clear custody policies, regularly transmit asset situations to customers, and assume responsibility for customer asset losses caused by cyber attacks/malfunctions, etc., trading platforms need to implement market manipulation monitoring, open trading prices and transaction depth, trading brokers need to formulate non-discriminatory policies, etc., and consultants and portfolio managers need to evaluate whether to conduct crypto asset investment based on their risk tolerance and knowledge.

Table 2: MiCA's Differentiated Capital Requirements for Crypto Asset Service Providers

4. Strengthen the management and supervision of issuer reserve assets,

and the key points are: quarantine and custody and timely redemption.

1. Clear requirements have been made on the custody and investment

direction of reserve assets

In order to protect ART's reserve assets from creditor claims by issuers and custodians, MiCA requires ART's reserve assets to always be completely isolated from the issuer's own assets. The issuer must hand over the reserve assets to a qualified credit institution, investment company or crypto asset service provider for individual custody, and the reserve assets shall not be used by the issuer for mortgage or as a guarantee. In the event of a loss, the custodian must return the crypto assets of the same type or value as the lost asset to the ART issuer unless the custodian can prove that he can be exempted from repaying the liability.

When the issuer faces bankruptcy and other inability to fulfill his obligations to the holder, the reserve assets should be used first to protect redemption repayment to the ART holder. However, when reserve assets cannot guarantee all holders’ redemption rights at face value, MiCA has not yet given specific requirements.

For EMT reserve assets management, MiCA requires the issuer to comply with the safeguard requirements of the EU Electronic Currency Directive (EMD2) and Payment Service Directive (PSD2): Reserve assets shall not be mixed with funds from any natural/legal person other than the payment service user at any time; reserve funds shall be invested in assets denominated in the same currency as the currency referenced by the electronic currency token to avoid cross-currency risks; and if funds are held by the payment institution and are not used for payment at the end of the next working day, they shall be deposited into the creditor's separate account or invested in secure, liquid, low-risk assets determined by the competent authorities of the country's member states; EMT issuers must isolate the reserve assets from the claims of other creditors, and ensure that the EMT holders are given priority repayment in the event of bankruptcy of the issuer.

In addition, MiCA has made strict requirements on the investment direction and structure of reserve assets of crypto asset issuers: general ART and EMT issuers need to deposit 30% of reserve assets as deposits in credit institutions (banking institutions), and important ART and EMT issuers need to deposit 60% of reserve assets as deposits in credit institutions.

2. Focus on protecting the holder's asset redemption rights

For ART, MiCA requires issuers to establish liquidity mechanisms and develop an orderly redemption plan to ensure asset liquidity and customer redemption requirements. If the market price of ART differs greatly from the value of reserve assets, ART holders have the right to redeem ART directly to the issuer even if the issuer does not grant the right through the contract. However, MiCA did not provide specific requirements for the time limit for the funds that holders redeem ART, and it is necessary to follow up on the specific implementation requirements of EU member states.

For EMT, MiCA requires that issuers must be able to redeem the currency value of their holdings at face value at any time, and redeem the currency value of their holdings in cash or credit transfer. The redemption conditions must be stated in the crypto assets white paper, and redemption shall not be charged. If the issuer of EMT has not met the redemption request of the EMT holder within 30 days, the holder may seek help from the custodian of the EMT assets and/or distributors acting on behalf of the EMT issuer.

5. Implement strict anti-money laundering supervision of cryptocurrency

and improve the implementation standards of travel rules

Crypto assets are based on blockchain issuance and transactions, and are characterized by decentralization, globalization, anonymity, convertibility (exchanged into fiat currency), and irrevocable transactions. Chain bridge technology strengthens the interconnection of different blockchains, resulting in the prevention of money laundering and terrorist financing risks of crypto assets becoming more complex. MiCA and the EU's relevant regulatory regulations have made targeted requirements for this.

1. MiCA requires crypto asset transactions to accept comprehensive

anti-money laundering regulatory requirements

MiCA attaches great importance to the possible illegal and criminal behaviors (such as insider trading, market manipulation, etc.) in the stablecoin and crypto market, requiring all crypto asset service providers to implement comprehensive anti-money laundering and anti-terrorist financing measures, including strict KYC procedures and transaction monitoring, implement strict customer due diligence (CDD) procedures and monitor suspicious transactions, and report to relevant authorities to prevent money laundering and terrorist financing activities.

Although ART and EMT are tokens operating on open systems without having to establish a direct relationship with issuers, MiCA still emphasizes that issuers should use chain analysis to understand token usage, allowing issuers to view active wallets holding their tokens in real time, including holder behavior (i.e. exchange and personal wallets, holding periods), overall transaction volume across multiple blockchains, and transaction size involving sanctioned entities or jurisdictions, etc., in order to prevent the use of tokens for illegal activities.

2. MiCA raises anti-money laundering “travel rules” requirements for

crypto assets

The Fund Transfer Regulations, which were passed at the same time as MiCA, provide more targeted requirements for crypto asset anti-money laundering and anti-terrorist financing operations, requiring crypto asset service providers to accompany information about the remitter and payee (i.e., the "travel rules" of anti-money laundering and anti-terrorist financing) when transferring crypto assets. In the absence of personally identifiable information, no amount of cryptocurrency is allowed to be transferred between accounts on their crypto asset service providers (CASPs). Compared with the 1,000 euro/dollar threshold set by the FATF for the implementation of the "Travel Rules", the above requirements of the Fund Transfer Regulations are undoubtedly more stringent.

In addition, in December 2024, the European Banking Authority (EBA) officially announced the expansion of the EU's Travel Rules Guide to crypto asset service providers and their intermediaries, requiring that it include collecting information reporting users' transfer of funds or crypto assets, determining whether transactions are related to the purchase of services, and monitoring suspicious crypto asset transactions; crypto service providers and intermediaries need to declare their multiple intermediary and cross-border transfer policies.

6. Impact on the development and regulation of global crypto assets

The implementation of MiCA marks the stage of the global crypto asset market development from "free development" to "compliance competition", which will have an important impact on the structure of the global crypto asset market development, the direction of global crypto asset supervision, and the construction of a global crypto asset collaborative governance system.

1. MiCA will promote the standardization and stratification of the

global crypto asset market development

On the basis of distinguishing crypto asset types, MiCA implements differentiated license access and operation supervision for issuers and service providers of crypto asset, and puts forward differentiated capital and liquidity requirements for different types of issuers and service providers, providing standardized action guidelines for the business activities of crypto asset market entities.

At the same time, considering that MiCA's regulatory requirements are relatively strict, such as high-standard supervision in the isolation and custody of reserve assets, minimum capital requirements, and anti-money laundering supervision, to increase the compliance cost of crypto asset market operations, it is conducive to leading compliant issuers and service providers (such as Circle's USDC) to consolidate market share through license barriers, while accelerating the exit of non-compliant crypto asset issuers and service providers.

In addition, MiCA exempts the supervision of fully decentralized crypto assets, but if decentralized exchanges (DEXs) involve fiat currency exchange or custody services, it still needs to be included in CASP supervision, which forces decentralized crypto asset trading platforms to restrict access to EU users and promote the marginalization of decentralized platforms. For the entire crypto asset market, these will ultimately increase the concentration of the entire market.

2. MiCA will become the "reference system" for the formulation of

crypto asset supervision policies in various countries

Judging from the policy recommendations of international regulatory organizations, in July 2023, the Financial Stability Council (FSB) issued the "High-level Recommendations on the Supervision of "Global Stablecoins"" and the "High-level Recommendations on Monitoring, Supervision and Supervision of Crypto Asset Business and Markets", among which the recommendations on the governance framework, risk management, information disclosure, reserve asset management and stablecoin redemption of stablecoins and cryptocurrency issuers and service providers, as well as the "same activities, same risks, same rules" and technically neutral regulatory principles are also requirements of MiCA, or the shadow of MiCA rules can be seen from it.

Judging from the regulatory practices of regulatory authorities in various countries, the regulatory agencies of EU countries will formulate specific implementation policies based on MiCA's requirements. The specific requirements of MiCA's classification definition of crypto assets, access supervision and operation requirements for issuers and service providers, upgrade the application of anti-money laundering supervision "performing rules", and restrictions on legal currency-supported stablecoins in other countries in physical transaction payments have also become important references for the formulation of cryptocurrency regulatory regulations in non-EU countries such as Singapore and Japan.

In this regard, MiCA has not only started the compliance process of the global crypto asset market development, but also started the standardization process of global cryptocurrency market supervision. Of course, in this process, it is not ruled out that some countries lower regulatory requirements (regulatory competitions) in order to promote the establishment of development advantages of their own cryptocurrency markets.

3. The construction of a collaborative system for global governance of

crypto assets is expected to be accelerated.

Crypto assets are globalized and essentially cross-border. Compared with traditional banking and financial markets, the crypto asset market has a higher degree of globalization, and it is more urgent to build a global regulatory governance system. Since the second half of 2023, the global stablecoin and cryptocurrency market has entered a rapid development track. According to Triple A's monitoring data, the number of global cryptocurrency assets exceeded 560 million in 2024, and the total market value of cryptocurrency assets has been above US$3 trillion most of the time after 2025. The integration of cryptocurrency assets with traditional financial system and real economy transactions has been rapidly advancing, and the construction of a global cryptocurrency governance system has become more prominent.

At present, global cryptocurrency supervision is still in a fragmented state of their own governance. International regulatory organizations have not yet issued stablecoins and crypto asset supervision standards similar to the "Basel Agreement", and there is no specific roadmap and timetable for the construction of stablecoins and crypto asset supervision systems in various countries. With the full implementation of MiCA in the EU, the United States is also accelerating the regulatory framework for stablecoins and crypto assets. It is expected that international regulatory organizations such as FSB will accelerate the research and formulation of unified regulatory standards for global crypto assets and the construction of collaborative governance mechanisms for global cryptocurrencies. The MiCA bill also clearly states that the EU will continue to support the promotion of global collaborative governance of crypto assets and services through international organizations or institutions (such as the Financial Stability Commission, the Basel Banking Regulatory Commission and the Financial Action Task Force).