How can Ethena lead the DeFi track in 2024?

Reprinted from jinse

12/27/2024·5MAuthor: Jack Inabinet, Bankless; Compiler: Baishui, Golden Finance

Ethena dominates DeFi in 2024, and while its synthetic dollar received a lot of criticism and attention upon launch, the team's efforts have become DeFi's most high-profile success this year as traders flock to the protocol One of the stories.

There are signals that the basis trading tokenization game is just getting started as other DeFi players look to capture Ethena’s growth prospects.

The market froth has significantly increased Ethena's revenue in recent months and transformed ENA into a top-performing cryptocurrency company.

Today, we explore Ethena’s success story in 2024.

explosive growth

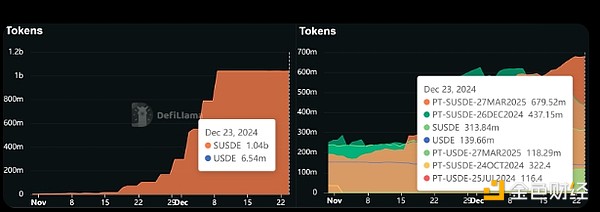

Ethena accepted its first public fundraising on February 19, and within a month of its mainnet launch, USDe’s circulating supply had surpassed all but five stablecoin competitors.

Thanks to its sizable airdrop incentives and its well-timed entry into the hottest funding rate environment of the year, USDe supply expanded unrestricted to $2.39 billion by mid-April, before fading as excitement over the ENA airdrop waned and the cryptocurrency market cooled At a standstill.

Although Ethena's subsequent decision on May 16 to reduce insurance funding occupancy temporarily revived USDe and led to a 50% expansion of one-month supply, continued compression of funding rates throughout the third quarter took its toll. By September, the increase in USDe supply had completely reversed, with ENA prices down 86% from their post-issuance highs.

While the funding rate arbitrage strategy employed by Ethena has long been possible for any trader familiar with futures, the problem is that the funds collateralizing these trades must be locked on the exchange (whether in CeFi or DeFi), which makes them unable to be staking. locking.

Through Ethena's approach, this underlying trading position itself becomes "tokenized" and represented in USDe, allowing traders to earn additional income in DeFi or lend against their holdings.

While third-party applications were initially hesitant to quickly incorporate USDe collateral, Ethena’s synthetic USD now dominates the crypto credit market due to simple yield economics.

Income providers that are unable to compete with Ethena 's market-leading returns may face the risk of reduced deposits or excessive borrowing demands. This dangerous dynamic could algorithmically set borrowing rates well above market value, forcing many DeFi lending markets to frantically buy billions of dollars in U.S. dollar derivatives collateral when funding rates surged again in November.

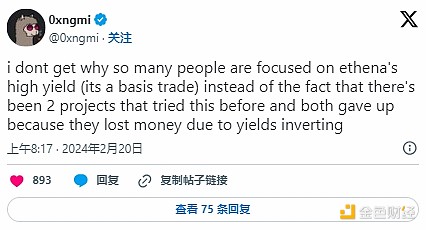

In just a few weeks, Aave's USDe's deposit limit soared to $1 billion (at the beginning of November, its lending market held a measly $20 million in Ethena collateral). Meanwhile, MakerDAO and other lenders on Morpho are taking in $1.2 billion in exposure to the extremely illiquid Pendle sUSDe primary token (PT) at an extremely high 91.5% maximum leverage.

An unparalleled asset?

Ethena’s asset is now intertwined with blue-chip DeFi, and ENA has taken a lot of interest, rallying an impressive over 500% from its September lows, ultimately settling not far from its post-launch highs.

While a negative funding rate environment is a known risk that could result in losses for USDe, many cryptocurrency observers are optimistic that Ethena 's recently deployed U.S. Treasury bond product (USDtb) could become a suitable underlying trading alternative, establishing a yield floor for Ethena savers .

That being said, funding rates are inherently unstable, and there is considerable uncertainty as to how Ethena will appropriately respond to a long-term negative funding rate scenario. If losses must be realized to convert existing synthetic USD exposure to Treasury collateral, USDe investors may begin to preemptively sell tokens to avoid additional losses, leading to further redemptions, which may result in USDe being forced to liquidate Or trigger a crisis of trust in the entire market. Position closing occurs in quiet markets where hedging demand is high (i.e. during a market downturn).

At its core, Ethena is an unregulated tokenized hedge fund. Despite the huge success of its basis trade in the fourth quarter of 2024, investors should still consider the protocol's various unknowns that could create problems if funding rates change.

panewslab

panewslab