Grayscale's latest research report: tariffs, stagflation and Bitcoin

Reprinted from panewslab

04/11/2025·20DOriginal title: "Market Byte: Tariffs, Stagflation, and Bitcoin"

Written by: Zach Pandl

Compiled: Asher (@Asher_0210)

Editor's note: This article analyzes the impact of recent changes in the US global tariff policy on the financial market, especially the unique performance of Bitcoin in this process; explores the long-term impact of tariffs on the economy, especially the choice of asset allocation during the stagflation period, and the performance of Bitcoin and gold in this environment; analyzes the impact of the current trade tensions on the US dollar and the potential adoption of Bitcoin, and finally makes a prospect for the economic outlook in the next few years, pointing out that scarce commodity assets such as Bitcoin and gold may usher in more attention and demand in a high inflation environment.

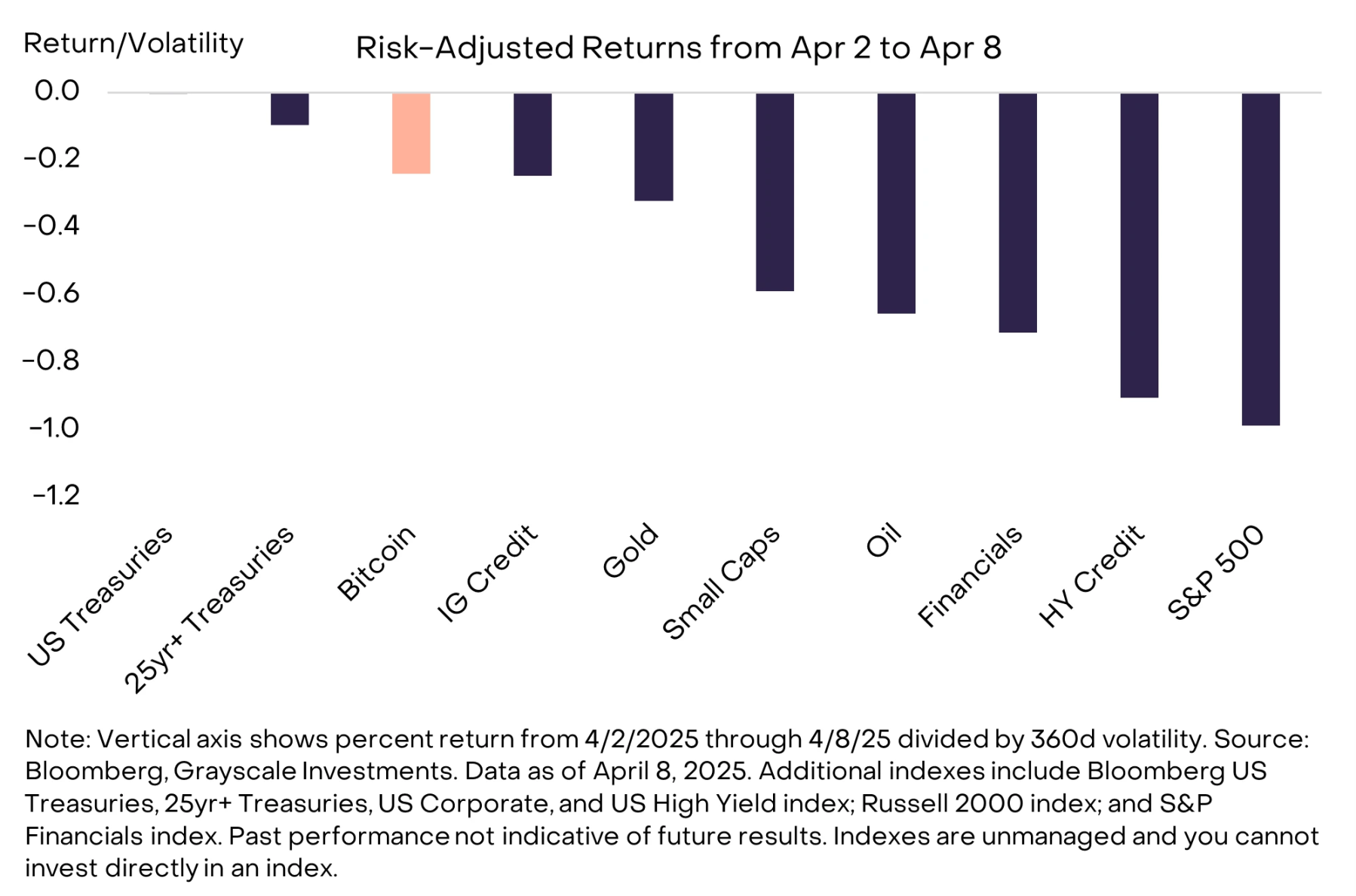

Since the United States announced a new global tariff policy on April 2, global asset prices have fallen sharply, and it was not until Trump announced this morning that the tariff suspension (except China) gradually recovered. However, the initial tariff announcement affected almost all assets, and during this time, Bitcoin fell relatively small by risk-adjusted benchmarks. So, if Bitcoin’s correlation with stock market returns is 1:1, the decline of the S&P 500 should mean that the price of Bitcoin is down 36%. However, the reality is that Bitcoin has fallen by only 10%, highlighting the significant diversification benefits that holding Bitcoin as part of its portfolio can bring about even when the market is in a deep retracement.

After risk-adjusted, Bitcoin price declines relatively small

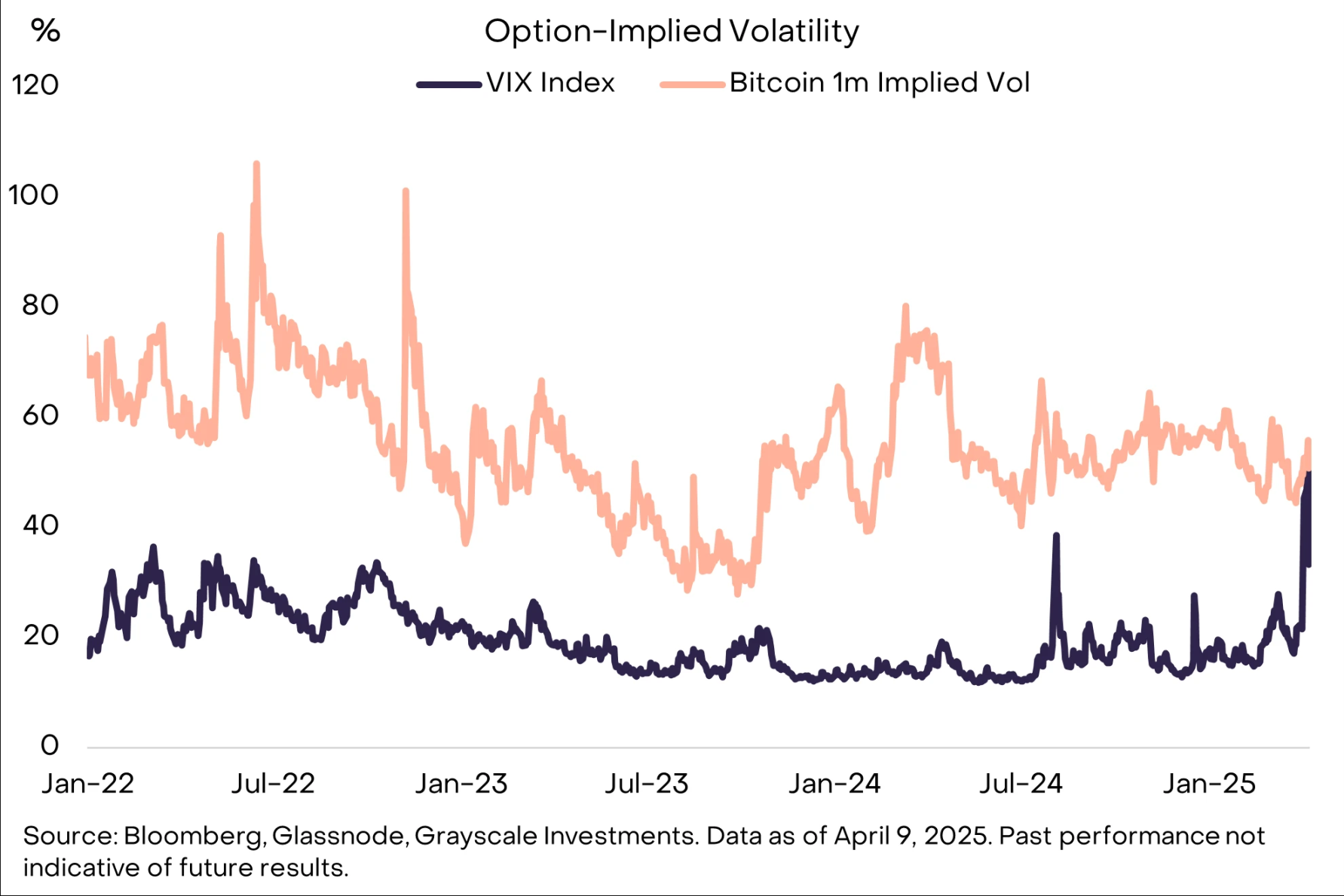

In the near term, the outlook for global markets may depend on trade negotiations between the White House and other countries. While negotiations may lead to lower tariffs, setbacks in negotiations may also trigger more retaliation, with the actual and implicit volatility of traditional markets still high, making it difficult to predict how trade conflicts will evolve in the coming weeks. Therefore, investors should adjust their positions carefully in a high-risk market environment. In addition, the increase in price volatility of Bitcoin is much lower than that of stocks, and multiple indicators show that speculative traders in the cryptocurrency market hold relatively low positions. If macro risks ease in the next few weeks, the market value of cryptocurrencies should be expected to rebound.

Implicit volatility of stocks is close to Bitcoin

Regarding Bitcoin, despite its price drop in the past week, the impact of higher tariffs on Bitcoin will depend on its impact on economic and international capital flows in the longer term. Tariffs (and changes in non-tariff trade barriers associated with them) may lead to "stagflation" and may lead to structural weakness in the U.S. dollar demand, so in this case, the increase in tariffs and changes in global trade patterns may be positive for Bitcoin's adoption in the medium and long term.

Asset allocation under stagflation

Stagflation refers to an economic state where economic growth is slow/slowing while inflation is high/accelerating. Tariffs raise prices of imported goods, thus (at least in the short term) leading to higher inflation. At the same time, tariffs may also slow down economic growth due to the reduction of residents' actual income and the adjustment costs faced by enterprises. In the long run, the impact could be partially offset by increased domestic manufacturing investment, with most economists expecting these new tariffs to continue to drag the economy for at least a year to come.

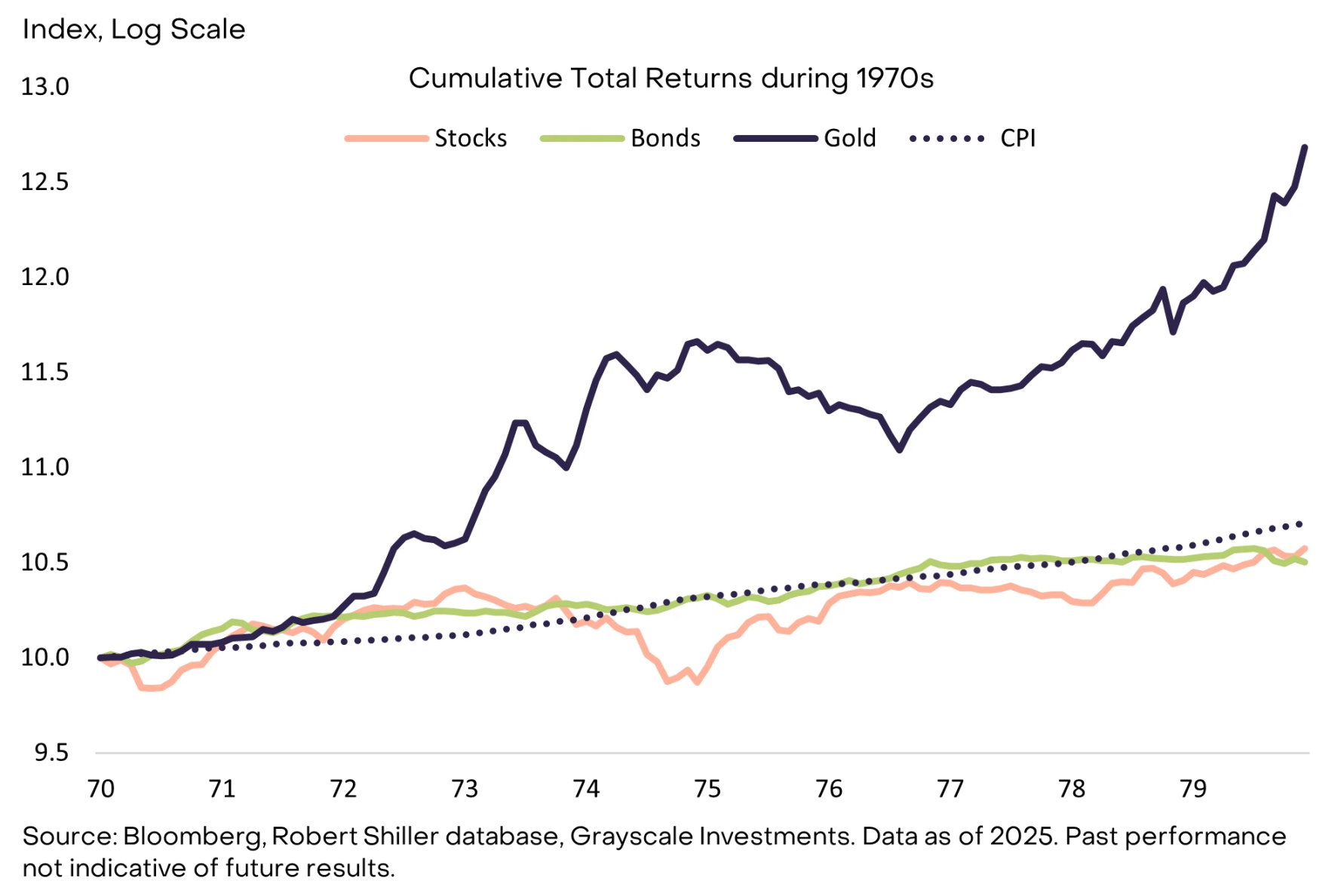

From a historical perspective, the 1970s’ asset returns most vividly demonstrated the impact of stagflation on financial markets (Bitcoin was too short to backtest its performance). In that decade, both U.S. stocks and long-term bonds had an annualized return of about 6%, lower than the average inflation rate at that time of 7.4%, compared with an annualized increase in gold prices at about 30%, far exceeding inflation.

The actual return of traditional assets in the 1970s was negative

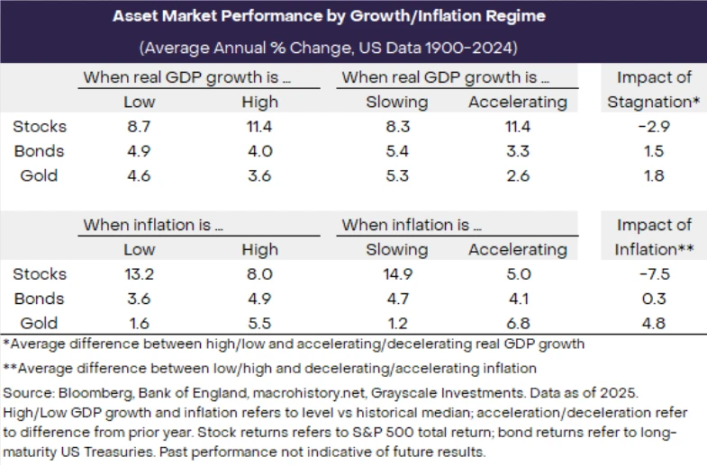

Typically, extremes during stagflation are rare, but their impact on asset returns is generally consistent over time. The following chart shows the average annual returns of U.S. stocks, government bonds and gold over different economic growth and inflation cycles from 1900 to 2024.

Stagflation reduces stock returns and improves gold returns

Historical data reveals three key points:

- Stock market returns usually increase when GDP is higher or accelerated and inflation is lower or slowed. Therefore, during stagflation, stock market returns will fall as expected and investors may need to reduce their equity allocation;

- Gold tends to perform better when economic growth is sluggish and inflation rises, especially during stagflation, which becomes the main tool to hedge against inflation. This suggests that in this environment, gold is often a more attractive investment option;

- Bond performance is closely related to changes in inflation. Bond yields are usually better when inflation is low, and bonds usually perform poorly when inflation rises. Therefore, bond investors may face the risk of a decline in returns during periods of rising inflation.

- In summary, different assets perform differently in the economic cycle, and investors should adjust their asset allocation according to the macroeconomic environment. Periods of stagflation are particularly important because they often have a negative impact on stocks, while gold may experience growth.

Bitcoin and USD

Tariffs and trade tensions may drive Bitcoin adoption in the medium term, one of the reasons is pressure on dollar demand. Specifically, if the overall trade flow with the United States declines, and most of the trade flows are denominated in US dollars, then the trading demand for the US dollar will decrease. Furthermore, if the imposition of tariffs also leads to conflicts with other major countries, they may weaken the demand for the US dollar as a means of stockpiling value.

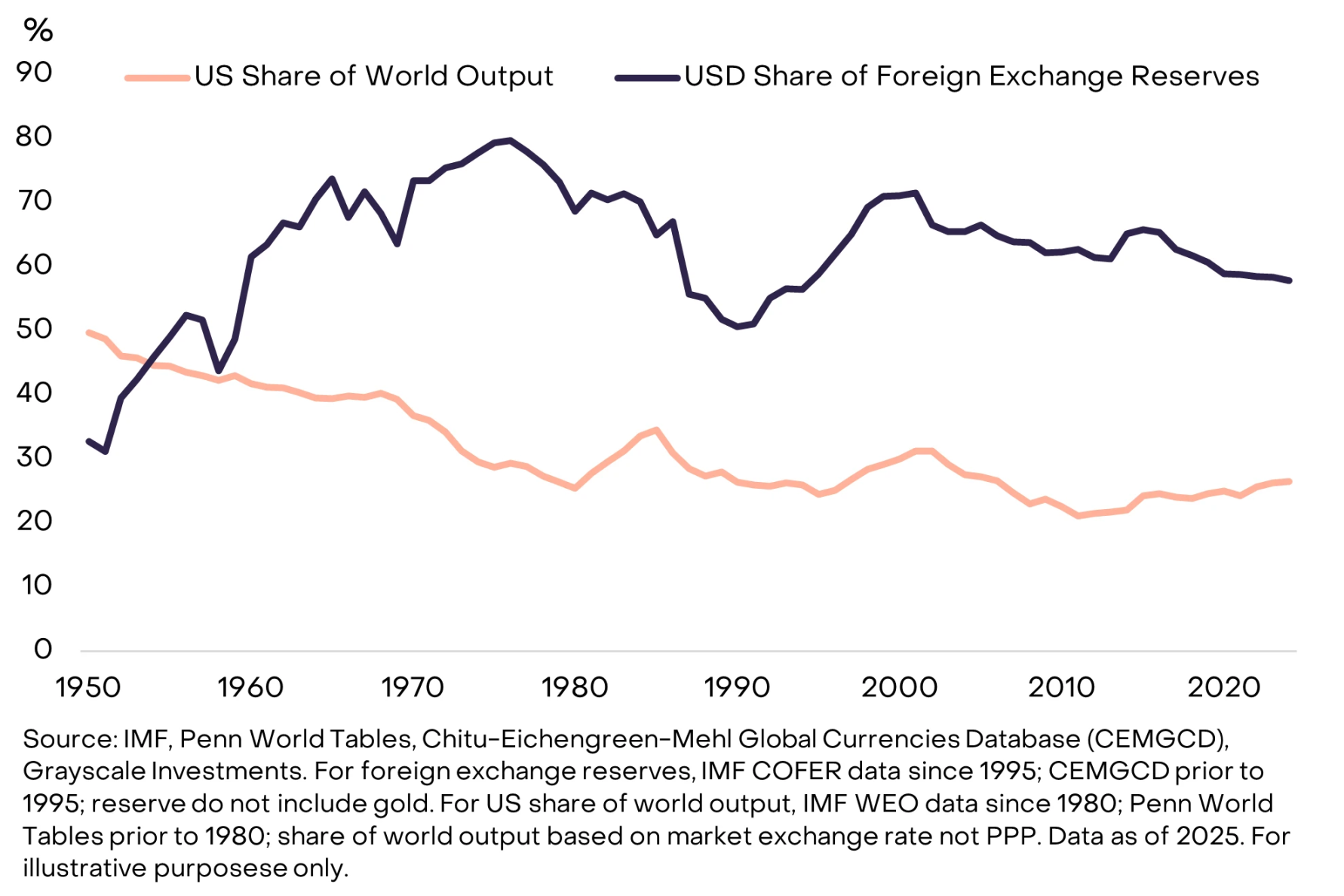

The US dollar accounts for far more than the US dollar's share of global foreign exchange reserves. There are many reasons for this, but the network effect plays an important role: countries trade with the United States, borrow in the US dollar market, and export commodities in US dollars. Countries could accelerate diversification of foreign exchange reserves if trade tensions lead to weaker links with the U.S. economy/dollar-based financial markets.

The US dollar accounts for far more than the US dollar\'s share in the global economy

Many central banks have stepped up their purchases of gold after Russia faces Western sanctions. It is understood that except Iran, no central bank in other countries currently holds Bitcoin on its balance sheet. However, the Czech National Bank has begun to explore this option, the United States has also established strategic Bitcoin reserves, and some sovereign wealth funds have publicly announced their investment in Bitcoin. In our view, the interference of the international trade and financial system centered in the US dollar may lead to further diversification of central banks' reserves, including investment in Bitcoin.

The most similar moment in American history to President Trump's "Liberation Day" statement may be the "Nixon Shock" on August 15, 1971. That night, President Nixon announced a full 10% tariff and ended the US dollar for gold, a system that has supported the global trade and financial system since the end of World War II. The action sparked diplomatic activity between the United States and other countries, and eventually reached a Smithsonian Institution agreement in December 1971, where other countries agreed to appreciate their currencies against the dollar. The dollar eventually depreciated by 27% between the second quarter of 1971 and the third quarter of 1978. There have been several rounds of trade tensions over the past 50 years that the dollar has weakened (partially negotiated).

Recent trade tensions are expected to lead to continued weakness in the U.S. dollar. According to relevant indicators, the US dollar has been overvalued, the Federal Reserve system has room to lower interest rates, and the White House hopes to reduce the U.S. trade deficit. Although tariffs will change effective import and export prices, the depreciation of the US dollar may gradually achieve a rebalancing of trade flows through market mechanisms, thereby achieving the expected results.

Son of the Times - Bitcoin

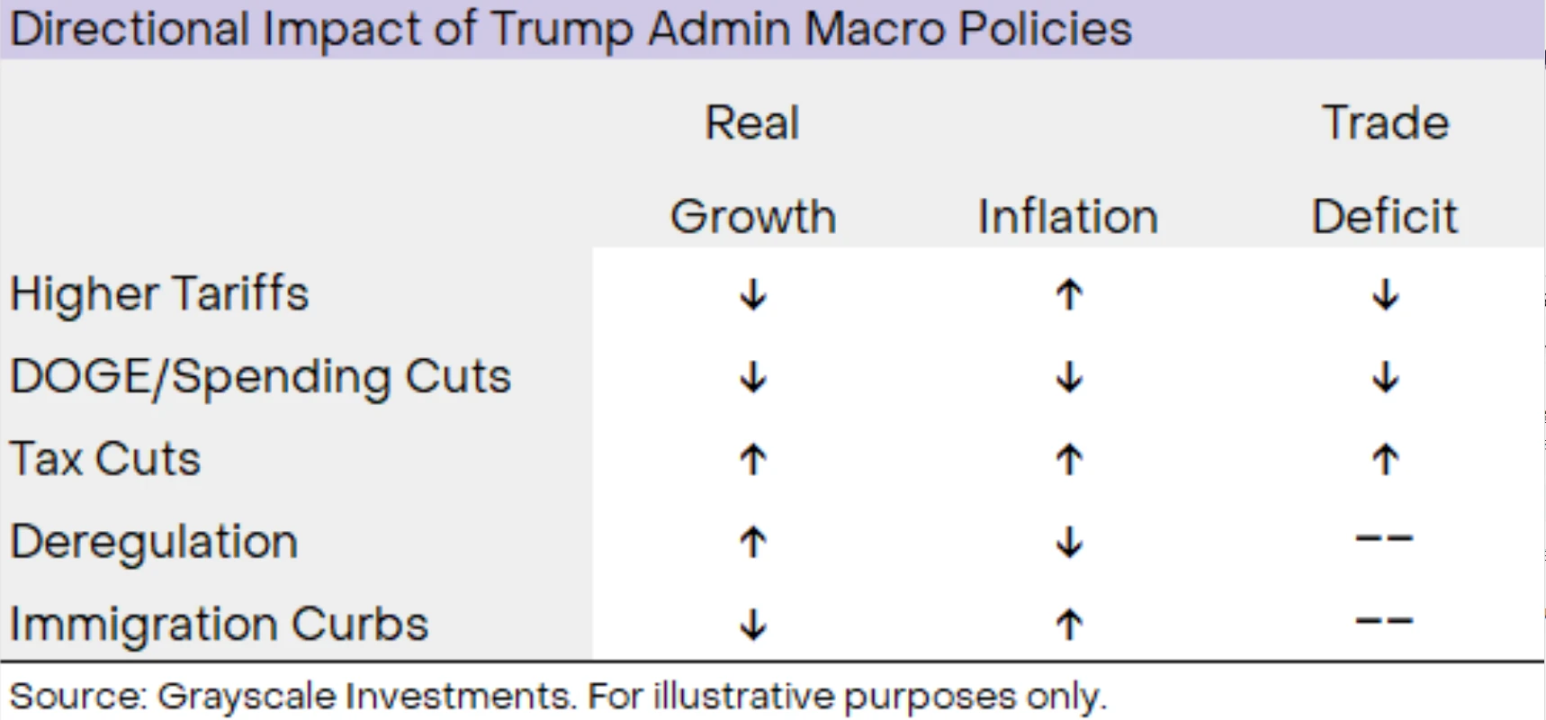

The sudden change in U.S. trade policy is causing adjustments to financial markets, which will have a short-term negative impact on the economy, however, market conditions in the past week are unlikely to become the norm for the next four years. The Trump administration is implementing a series of policy measures that will have different impacts on GDP growth, inflation and trade deficits. For example, while tariffs may reduce economic growth and increase inflation (i.e., cause stagflation), some types of deregulation may increase growth and reduce inflation (i.e., reduce stagflation), the end result will depend on the extent to which the White House implements its policy agenda in these areas.

U.S. macroeconomic policies will have a series of impacts on growth and inflation

Despite uncertainty in the outlook, the best guess is that the U.S. government policy will lead to continued weakness in the U.S. dollar and overall higher-than-target inflation over the next 1 to 3 years. The tariffs themselves may slow growth, but the impact may be partially offset by tax cuts, deregulation and a devaluation of the dollar. If the White House also actively promotes other growth-promoting policies, GDP growth may remain relatively good despite initially being hit by tariffs. Regardless of whether the actual growth is strong or not, history shows that sustained inflationary pressures over a period may be favorable for scarce commodities such as Bitcoin and gold.

Furthermore, like gold in the 1970s, Bitcoin now has a rapidly improving market structure—supported by changes in the U.S. government policy. The White House has implemented a broad range of policy changes this year that should support investment in the digital asset industry, including the removal of a series of lawsuits, ensuring the applicability of assets to traditional commercial banks, and allowing regulated institutions, such as custodians, to provide cryptocurrency services. This in turn triggered a wave of mergers and acquisitions and other strategic investments. The new tariffs are a short-term downside to valuation of digital assets such as Bitcoin, but the Trump administration's cryptocurrency-specific policies have been supporting the industry. Overall, the rising demand for scarce commodity assets in the macro economy and the improvement of investors' operating environment may be a powerful combination of widely adopted Bitcoin in the next few years.

jinse

jinse