Galaxy: Understand the future trends of Bitcoin mining and AI infrastructure in one article

Reprinted from jinse

12/24/2024·4MSource: Galaxy; Compiled by: Baishui, Golden Finance

summary

- Bitcoin miners with large-scale land, cooling water, dark fiber, reliable power, skilled labor, power approvals and critical long-term lead time infrastructure components are well-positioned to meet the needs of the rapidly growing AI/HPC data center market to increase the value of its assets.

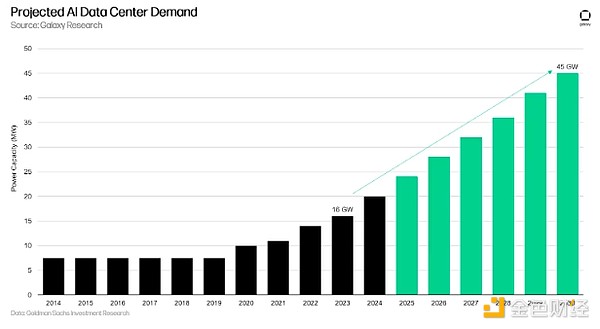

Goldman Sachs research predicts that U.S. data center demand will reach 45 gigawatts by 2030, with power demand growing at a compound annual growth rate of 15% between 2023 and 2030, driven by AI.

-

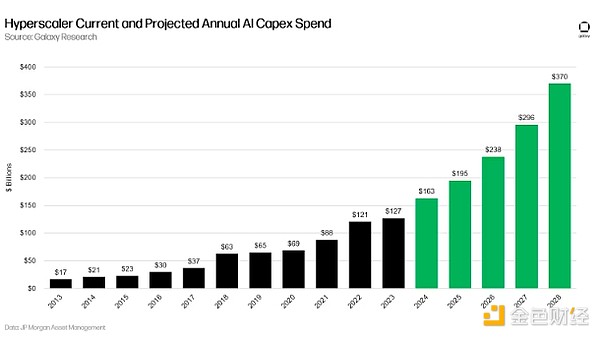

JPMorgan Chase predicts that ultra-large-scale AI capital expenditures will reach US$370 billion by 2038, a 127% increase from the projected AI capital expenditures in 2024.

-

The dramatic increase in connection requests from facilities ranging from 300 MW to 1,000 MW or more is putting pressure on the local grid's ability to deliver power at such a fast pace, resulting in 2-4 years longer interconnection and construction times.

-

Traditional data centers do not have the high power capacity to support high-density computing operations. Server racks, which once had a maximum power of 40 kW per rack, now need to support more than 132 kW per rack, which is required for cutting-edge systems such as the GB200 NVL72.

-

Cash flow predictability, active financing markets, and significant valuation upside for AI/HPC operations make this opportunity highly attractive and potentially accretive to miners with the right assets.

-

Miners can unlock significant value by transitioning to the AI/HPC market, by arbitraging their EV/EBITDA valuations of 6-12x versus the typical 20-25x multiples currently offered by leading data center operators.

Preface

The rise of artificial intelligence (AI) is creating unprecedented demand for high-capacity computing (HPC) facilities. This surge has led to significant investments in new data center capacity by hyperscalers. However, due to limited power capacity, the construction time of new facilities extends to 2-4 years, making it difficult for traditional data centers to meet these needs.

Bitcoin miners are uniquely positioned to take advantage of this market opportunity as they already have access to the critical components needed to operate large-scale power infrastructure and data centers. While not all mining facilities can be converted into AI data centers due to specific requirements for cooling, networking, and redundant systems, those with the right assets and expertise will benefit from the high cash flow margins and huge valuations of AI/HPC operations. benefit from value potential. The report examines the current landscape of traditional data centers and highlights specific barriers to meeting AI computing needs. The report then analyzes why certain types of Bitcoin miners are well-positioned to fill this gap and explores future trends at the intersection of Bitcoin mining and AI infrastructure.

What are the opportunities for AI data centers?

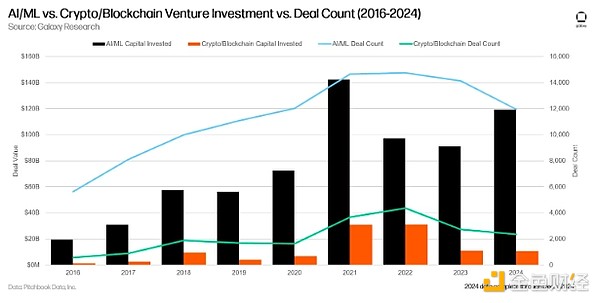

AI is booming in 2024, driven by widespread adoption of generative AI (GenAI) technology. According to Pitchbook, more than $680 billion has been invested in AI and machine learning startups across more than 100,000 deals since 2016, with $120 billion invested in 2024 alone.

The proliferation of artificial intelligence and high-performance computing (HPC) is creating huge demands on data center capacity. Data centers are critical to AI/HPC operations, providing the infrastructure and power required for GPU-intensive computing. New AI applications such as large language models (LLMs) are particularly power-hungry. According to the International Energy Agency, a single ChatGPT query requires 2.9 watt hours of electricity, while a Google search requires only 0.3 watt hours.

The emergence of emerging energy-intensive AI/HPC businesses in the United States has driven the growth in demand for data centers. Goldman Sachs Research estimates that U.S. data center demand will reach 21 GW by 2024 (a 31% year-on-year increase). For reference, data center demand growth in the United States from 2022 to 2033 is estimated to be a CAGR of 15.8%. Based on the substantial year-on-year growth in data center demand in 2024, Goldman Sachs Research predicts that U.S. data center demand will increase to 45 GW by 2030. By 2030, U.S. data centers will consume 45 gigawatts of electricity, accounting for 8% of the total U.S. electricity capacity.

The U.S. data center market opportunity will be supported by increased investment in AI infrastructure by hyperscalers, which are large data center companies such as Google Cloud and AWS that can quickly expand data center capacity to serve other enterprise customers. These hyperscale companies have committed to investing more than $100 billion in AI data centers over the next 10 years to cope with growing data center demand. JPMorgan Asset Management estimates that $163 billion will be invested in expanding hyperscale enterprise businesses by the end of 2024, a year-on-year increase of 28%. The report predicts that AI capital expenditures by hyperscale enterprises will reach $370 billion by 2038, a 127% increase from the 2024 AI capital expenditure estimate.

Current and expected growth in AI and HPC technologies are changing the data center landscape. As processing demands increase, hyperscale data centers and data centers are gradually evolving from traditional computing facilities to advanced AI infrastructure centers. These facilities are becoming the foundational infrastructure that will power breakthrough technologies such as autonomous vehicles, advanced medical research, and next-generation AI applications. The future of digital innovation will largely depend on the continued development and expansion of these critical computing facilities, marking a new era in technology infrastructure.

Current Data Center Market Overview

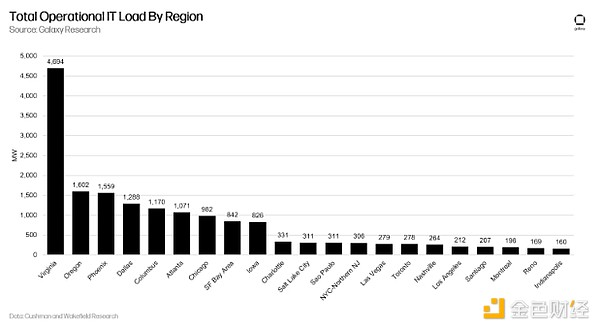

The current data center market consists of multiple public and private companies that collectively manage a large number of data centers. Well-known companies in this field include Digital Realty, Equinix, Vantage, EdgeConnex and QTS, among others. The largest data center region in the U.S. is currently in Northern Virginia, according to CBRE, but growth in all regions has been rapid, resulting in vacancy rates reaching historically low levels.

Data centers are the backbone of several different industries, supporting everything from streaming services like Netflix to cloud computing, artificial intelligence and numerous other applications. However, not all data centers are created equal. Each data center can be customized for specific capabilities and classified into different categories, including hyperscale, edge, cloud and enterprise data centers. Data centers are getting larger and larger, and their power density is getting higher and higher. The competition to provide infrastructure for rapidly expanding industries such as AI has led to an arms race among hyperscalers to expand data center capacity at an accelerated pace.

Barriers Traditional Data Centers Face in Meeting Artificial Intelligence

Needs

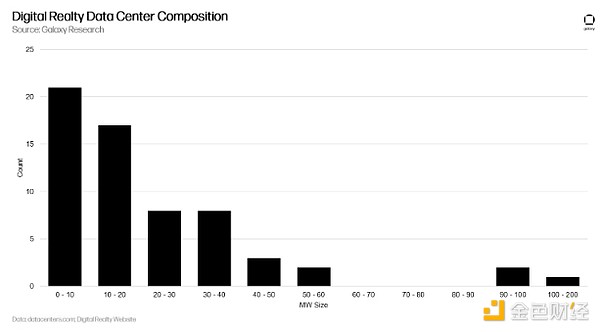

Traditional data center providers serving non-AI industries typically use a smaller, geographically dispersed portfolio of data centers, many of which were originally built for low-density applications. Over the past decade, traditional data centers have operated on relatively low energy consumption. Although Digital Realty (market cap $62 billion) and Equinix (market cap $94 billion) are two of the world's largest data center companies, they primarily operate smaller data centers. For example, Digital Realty's data centers typically range from 0.5 megawatts to 40 megawatts per facility. Likewise, Equinix's xScale plan consists of a global data center network with a total operating capacity of just 292 MW across 20 facilities (Equinix Q3 2024 Investor Presentation, November 8, 2024). In contrast, some mining operations can obtain comparable energy capacity at a single site.

Historically, operators have had little incentive to scale quickly because of the limited computing density of streaming services, telecoms, data storage and many cloud applications. However, as artificial intelligence advances and these algorithms become increasingly complex, data centers must now use the latest generation of GPUs and run state-of-the-art facilities at scale to optimize training execution.

The increase in scale is due to advances in GPU computing power and the advantages of parallel computing, allowing data centers to build larger clusters with greater computing power. Parallel computing allows workloads to be seamlessly distributed across other GPUs, allowing efficient scaling by adding more units. Crucially, large clusters at a single site reduce latency between GPUs, thereby improving the performance of parallel computing. This advantage makes a single 200MW cluster significantly more efficient for AI training than four geographically distributed 50MW clusters, as low-latency communication between GPUs is critical to maximizing computing efficiency. As a result, hyperscale enterprises prioritize a single location with access to high power capacity to meet the needs of advanced AI workloads.

Currently, this capacity is in short supply, with many legacy facilities struggling to meet the massive energy demands required by modern AI/HPC workloads. Older facilities cannot be easily retrofitted due to factors such as differences in network, cooling, and rack density requirements between low and high compute use cases.

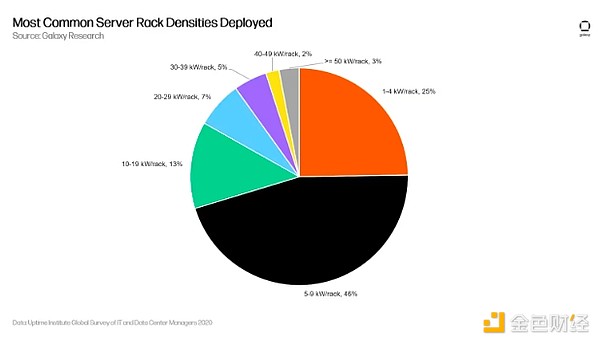

Today, hyperscale enterprises require data centers with higher energy capacity to support the training of their energy-intensive models, such as large language models. According to a December 2020 Uptime Institute article, the average rack density for that year was 8.4 kW/rack, excluding high-performance outliers of 30+ kW/rack. Server racks in these data centers, which once had a maximum power of 40 kW per rack, now need to support more than 132 kW per rack. This is the power required by cutting-edge systems such as NVIDIA's GB200 NVL72, which has grown in just a few years. Three times more. Industry experts predict that increases in computing density and the development of Moore's Law may push server rack power requirements to unprecedented levels.

As a result, traditional data center operators have shifted their focus to greenfield development to accommodate a new generation of AI/HPC dedicated data centers, the energy approval and construction of which will take several years. According to a recent U.S. Department of Energy report, a sharp increase in connection requests from facilities ranging from 300 megawatts to 1,000 megawatts or more is putting pressure on local grids’ ability to deliver power at such fast rates, leading to interconnection and construction The time extension is 2-4 years.

Hyperscale data center operators now aim to build the largest possible GPU clusters to train AI/HPC models, with several companies targeting gigawatt- level data centers to accommodate hundreds of thousands of next-generation GPUs. While hyperscale data center operators are building their own data centers, they still rely heavily on third-party vendors with proven power capabilities to power GPUs in a faster timeframe. However, only a few existing data centers can handle such huge power demands and high rack energy density. Much of this shortage stems from a lack of expectations for the dramatic growth in data center demand.

Why Bitcoin miners can fill a critical gap

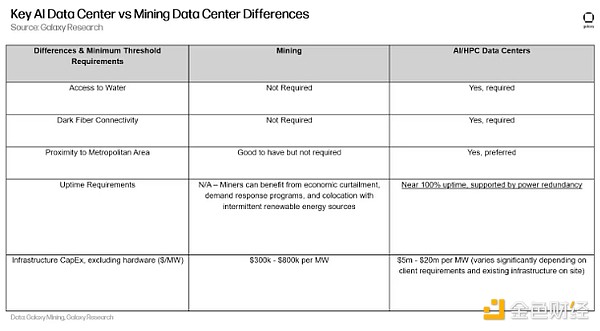

Bitcoin miners have large-scale, power-ready facilities and are therefore capable of meeting the energy needs of very large-scale miners. For years, miners have been looking for sites with abundant and affordable energy and securing large amounts of power capacity in a single location, as well as long-term infrastructure projects such as substation components and medium and high-voltage equipment. Some mining sites already have power-ready capabilities, which solves one of the biggest constraints faced by hyperscale miners: access to reliable power at scale.

By having access to these electricity-ready Bitcoin mining sites, hyperscale miners can bypass the lengthy process of ensuring energy availability and focus on retrofitting and customizing infrastructure to meet their specific needs. Many miners control sites with hundreds of megawatts, and few traditional data center operators can achieve this scale in a single location. Several large mining companies have established access to industrial-scale power infrastructure, securing energy pipelines with a capacity of over 2 gigawatts (GW), allowing miners to benefit from increased demand for power capacity. Although there are significant differences between traditional Bitcoin mining farms and AI data centers, miners have valuable experience in large-scale building and data center management and often have mature electrical, mechanical, facilities and security teams. This expertise can further simplify the transition for hyperscale enterprises looking to scale quickly.

Only some miners can benefit from artificial intelligence

Not all miners can take advantage of AI/HPC opportunities. To build a data center suitable for AI/HPC, several key factors must be met, including access to large-scale land, cooling water, dark fiber, reliable power and skilled labor. Unfortunately, even if these conditions are met, companies that have not yet obtained the necessary approvals (i.e., power capacity, land, and zoning) or do not yet have critical long-term infrastructure components will encounter obstacles and delays in the development process.

Another key reason why not all Bitcoin miners are able to take advantage of the AI/HPC opportunity is that miners’ existing infrastructure is not directly transferable or adaptable to AI data centers due to differences in design and operational requirements. While there are some similarities in critical electrical infrastructure, including high-voltage substation components and power distribution systems, AI data centers have specific requirements that require detailed expertise and skilled labor.

The complexity of AI data centers elevates nearly every aspect of operations, including mechanical, cooling, and networking systems, making converting Bitcoin mining facilities into AI/HPC data centers a daunting task. Below, we outline some of the major upgrades miners will need to transform their existing facilities into AI data centers:

1. Network infrastructure:

AI/HPC workloads require high-speed, low-latency connections between data center GPUs. Therefore, the internal network structure of AI/HPC workloads is much more complex than mining because GPUs are constantly communicating with each other. The key to successful AI operations is developing an optimal network backbone to ensure rapid execution of workloads. Additionally, connections to dark fiber must be established from the site and latency requirements must be met, whereas mining sites do not require these requirements.

2. Cooling system:

Miners use a variety of cooling designs, including air-cooled, water-cooled, and immersion cooling systems. Cooling focuses primarily on the actual machines themselves and less on the supporting infrastructure. AI data centers, on the other hand, will require more advanced cooling solutions, such as direct-to-chip liquid cooling to cool the latest generation of power-dense NVIDIA servers, combined with additional air cooling systems to support network and mechanical infrastructure.

3. Redundancy:

Compared with Bitcoin mining data centers, artificial intelligence data centers have stricter redundancy requirements. Mining operations are inherently flexible and therefore do not require powerful backup power generation facilities. AI data centers, on the other hand, typically use at least N+1 redundancy throughout operations, while more mission-critical components such as core network and storage components require a higher degree of redundancy to ensure uninterrupted operations , or at least properly cache and check data in the event of device failure. This means that for every critical piece of infrastructure (such as cooling equipment), there must be a backup (N+1 redundancy). For example, when performing maintenance on a cooling unit, an additional unit must be available to maintain continuous operation. This level of redundancy is rarely found in mining facilities without such uptime requirements.

4. Redesign of overall dimensions:

AI data centers use rack-mounted servers, which are very different from the shoebox ASICs used in Bitcoin mining. Accommodating AI hardware requires a complete redesign of a facility's internal physical infrastructure to support rack-mounted systems and their specific cooling, networking, and electrical needs.

5. Other differences:

Collectively, these factors indicate that retrofitting mining facilities to meet the requirements of AI/HPC data centers is a design and engineering challenge. Enhanced infrastructure requirements also cause AI/HPC data center capital expenditure costs to rise significantly relative to Bitcoin mining construction costs.

Miners able to capitalize on AI data center demand have upside potential

While miners may have the right infrastructure and location, transitioning to AI/HPC operations requires more than just physical assets—it requires expertise, a different technology stack, and new business models. Those who have experienced management teams and can successfully build AI/HPC operations have a huge opportunity to bring significant incremental value to their companies. Here are some key advantages that can add value to companies that choose to allocate their power and data center resources from Bitcoin mining to AI/HPC:

-

High cash flow margins and predictability: AI/HPC data center operations, especially colocation/custom models, have long-term contracts with fixed and recurring cash flows typically agreed upon before data center construction begins. These are predictable and high-margin cash flows, often with reputable counterparties, and data center operators can pass on the majority of costs to tenants, including energy and operating expenses (depending on the lease structure).

-

Cash flow diversification: Revenues are not only more predictable than Bitcoin mining, but are also cryptocurrency market agnostic, which can balance out the revenue profiles of companies with higher exposure to volatile cryptocurrency markets. In a Bitcoin bear market, this could enhance financial stability, allowing miners to continue raising cash through equity or debt without incurring undue dilution or interest burdens.

-

Deep capital markets can help scale operations: Although the infrastructure is much more expensive than Bitcoin mining, underwriting investments is more straightforward due to the predictability of cash flow, opening up new sources of debt and equity capital for data center projects. Private equity firms, infrastructure investments, pension funds, life insurance companies and many other companies are eager to get involved in the data center space to reap the benefits. A data center operator that has a lease with a reputable counterparty can assume the lease and raise significant project financing to build the data center.

-

According to Newmark's 2023 Data Center Market Annual Overview Report, term debt financing volumes hit an all-time high in 2023 and are not slowing down, with $18 billion in development financing being underwritten in the first quarter of 2024 alone. Interest rates are also very reasonable, with Newmark's rates ranging from approximately 2.25% - 4.50% of SOFR, depending on the lender.

-

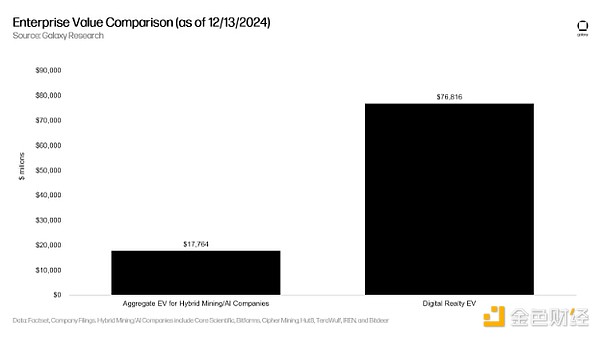

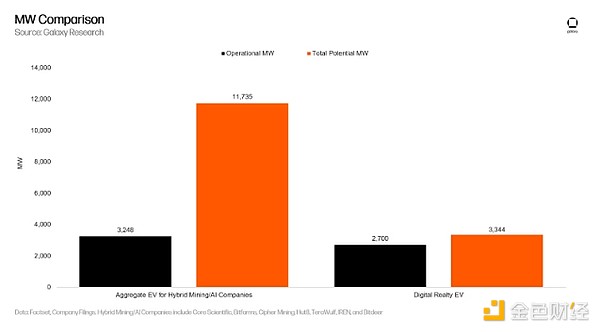

Huge valuation appreciation potential: Once the assets are established and stabilized, there is also a huge valuation difference between mining and AI/HPC, making AI/HPC a very attractive opportunity. Bitcoin miners have historically traded in the 6-12x EV/EBITDA multiple range, while some of the world's largest data center operators are valued at 20-25x EV/EBITDA. This makes sense given the industry’s high profit margins, growth trajectory, predictable cash flow, and reduced market volatility compared to cryptocurrencies. To further understand the scale of the current difference, the total EV of hybrid mining/AI companies is 23% of Digital Realty's EV, despite the total potential MW capacity being 3.5 times greater.

Therefore, cash flow predictability, active financing markets, and significant valuation upside make AI/HPC opportunities extremely attractive and have value-added potential for miners with the right assets. These miners are expected to make significant inroads into the traditional data center market and become one of the largest operators in the industry.

The future of Bitcoin mining

AI/HPC has been in the spotlight over the past few months, but we still expect the hashrate and growth of Bitcoin mining networks to continue to rise. The growth of mining coincides with the growth of AI/HPC. Rising Bitcoin prices increase miners' profitability, and if prices continue to move higher and outpace increases in network difficulty, mining may become even more profitable. But with the rise of Bitcoin and AI/HPC, what will the future mining landscape be like? Below we outline some of the major trends that may emerge in the convergence of AI/HPC and Bitcoin mining in the foreseeable future:

Miners maximize the value of electrons:

Most Bitcoin miners always prioritize maximizing the value of their energy usage. Currently, AI data centers are the most profitable path for those with adaptable sites. Considering the value growth of AI/HPC sites, mining sites that can be converted into AI/HPC data centers are likely to follow this path to maximize shareholder value. However, this does not necessarily mean a disadvantage for Bitcoin miners. We still expect network hashrate to grow, but at a slower rate than if none of the major US miners converted their sites to AI/HPC data centers. These transformations benefit miners who remain on the network by eliminating competition for hashrate.

Bitcoin mining is the driving force behind monetizing idle electricity:

As Artificial Intelligence/High Performance Computing (AI/HPC) gains increasing prominence, we expect miners to further focus on deploying their capacity in more remote locations as hyperscalers have the infrastructure available for AI/HPC in more developed markets of large sites and thus outbid miners. Bitcoin mining is permissionless, location-independent, and flexible, making it one of the best ways to utilize idle power generation capacity.

We expect that a larger portion of Bitcoin mining will be pushed to the edge to monetize idle power capacity – particularly in remote areas of the United States and in international emerging markets such as Ethiopia and Paraguay, which are rich in cheap excess energy.

Bitcoin Mining as a Strategic Bridge between Infrastructure Investment

and AI/HPC Optionality

Additionally, as different regions of the United States strive to build transmission infrastructure and fiber optic connections, Bitcoin mining could serve as a bridge to underwrite larger capacity energy infrastructure projects such as substation and power plant construction, even when there is no immediate or clear opportunity to capitalize The same is true in the case of AI/HPC capacity. By using Bitcoin mining for opportunistic real estate and power generation-related investments, investors can earn returns while waiting for other long-term energy use cases to materialize, positioning it as an attractive strategy for infrastructure growth and investment.

For miners who cannot convert to AI/HPC data centers, Bitcoin mining farms can still operate as long-term profitable businesses. Several miners have purchased large capacity facilities without existing AI/HPC tenants and have also invested in sites in various stages of development. As we have outlined before, some of these sites may not have the best features required for AI/HPC but are still useful for Bitcoin mining. Other miners do not have the teams or in-house expertise to contract with major offtakers and undertake challenging engineering and large-scale construction projects. The hope of miners seeking to maximize value is to lock in an AI client, but in the event that the AI/HPC opportunity does not materialize, these miners still have the option of building a profitable BTC mining operation.

Emerging synergies between AI/HPC data centers and mining

ASIC manufacturers such as Bitmain have begun developing ASICs with form factors similar to GPUs for data center racks. Further harmonization of ASIC form factors with next-generation GPU form factors will allow data centers to monetize their underutilized server racks by installing server-sized miners in free rack space, which would be possible if similar racks were used Helps simplify the process of transforming data centers for AI/HPC. Going forward, miners may be more willing to purchase these machines because they maintain flexibility in data center design and can help miners move to AI/HPC more easily if higher value opportunities arise.

As AI/HPC data center capacity grows, so does their impact on the grid. While these data centers must be online almost all the time, this does not necessarily mean that total energy consumption is constant. In fact, the load profile for AI/HPC training can be very unstable, as more power is consumed during intensive compute execution and less power is consumed during checkpoints. The frequency of checkpoints varies, and depending on the deployed infrastructure and the size of the model, the process can take anywhere from a few minutes to tens of minutes. As the size of the model increases, more data needs to be stored, increasing the time required to save all the data.

Likewise, for AI/HPC inference workloads, load profiles are expected to be closely aligned with customer needs because every model query is processed directly within the data center. Initially, these profiles may exhibit significant volatility as model demand fluctuates. Over time, however, as a particular model becomes more widely adopted, loads may become more predictable, with demand peaking during the day and declining at night. This daily load cycle presents an ideal opportunity for Bitcoin mining, as mining operations can dynamically scale up or down to supplement the fluctuating energy demands of the AI inference process.

Therefore, in the future Bitcoin mining can be used as a load balancing mechanism, with mining increasing when the load is low and decreasing when the AI load resumes. Tenants may not yet need to use full GPU capacity, allowing miners to accelerate.

For data center operators, the benefits are clear, as they are able to extract more value from the capacity that can be brought online, while for tenants, this provides a degree of load stability to the data center and the grid as a whole. As data center clusters increase in size, power consumption and impact on the grid will come under increasing scrutiny, and ensuring load stability will be critical.

Moving MW to AI/HPC should slow hashrate growth rate

Miners moving into AI/HPC operations are actively diverting capacity that could otherwise be used for Bitcoin mining, which should slow the growth rate of the network hash rate. This is especially important given Bitcoin’s potential bull run, as an increase in Bitcoin’s price will not bring an equal and offsetting increase in the network’s hash rate, pushing the hash rate higher. That being said, we still expect network hashrate to rise as more efficient mining machines come online, either to replace older generation machines or to make net new investments at sites that are not conducive to AI/HPC operations.

Summarize

Data center demand in the United States is likely to surge at an unprecedented rate, with a year-over-year growth of 31% expected in 2024 alone. The forecasts also suggest that U.S. data center capacity will more than double over the next five years, jumping from the current 21 GW of data center capacity to a projected 45 GW. This explosive growth, coupled with the hundreds of billions of dollars of investment committed by hyperscale providers over the next 5-10 years, creates an attractive opportunity for companies that can provide two critical resources: abundant cheap energy and the ability to Robust infrastructure to support AI and HPC operations.

The current AI and HPC boom has exposed a key weakness of traditional data centers: their inability to retrofit existing facilities to meet the powerful power demands of modern AI workloads. This gap in the market creates a significant opportunity for Bitcoin mining operations, which already have what AI/HPC companies desperately need: large sites with accelerated power-up plans. Hyperscale providers have limited options and cannot scale their operations in time to meet the explosive demand of AI/HPC businesses. Bitcoin miners are becoming a legitimate and viable option for hyperscale enterprises to expand their operations and stay competitive in a growing market. However, this generational opportunity for Bitcoin miners remains selective. Only a small percentage of Bitcoin mining operations have the necessary infrastructure and capabilities to successfully support the demanding requirements of modern AI/HPC workloads. Those miners who own these scarce assets and seek to maximize their value will turn to AI/HPC data centers.

While some critics argue that Bitcoin miners’ diversification into AI/HPC services could weaken network security by reducing the amount of computing power dedicated to mining blocks, the shift could actually benefit the broader mining ecosystem. Miners unable to meet the demands of AI/HPC sites can gain higher profitability from increased hash prices. As more miners go offline and Bitcoin prices rise, rising hash prices will significantly increase the profit margins of all Bitcoin miners. With Bitcoin prices up as much as 143% year-to- date and a new pro-Bitcoin president in the White House, Bitcoin mining in the United States is poised to enter its strongest era yet.

The intersection of cryptocurrency and artificial intelligence is arguably one of the hottest cryptocurrency areas in 2024. As of December 2024, the total market capitalization of cryptocurrency projects using liquid tokens to build artificial intelligence projects is approximately $33 billion. Additionally, Galaxy Research estimates that more than $382 million in venture capital has been allocated to early-stage crypto AI startups in 2024. While most crypto AI projects lack product-market fit, the intersection of Bitcoin mining with the growth of AI/HPC businesses is clear. Bitcoin mining’s entry into AI stands out from other overlapping areas of the two sectors because of its potential to supply at scale the most important component of an AI/HPC business – energy. Therefore, Bitcoin miners holding AI/HPC convertible assets may be one of the only pure and scalable crypto-x AI investments in the industry today.

panewslab

panewslab