From Bitcoin Ecosystem to RWA Track, Web3 Ecosystem Panoramic Analysis

Reprinted from panewslab

04/21/2025·1M

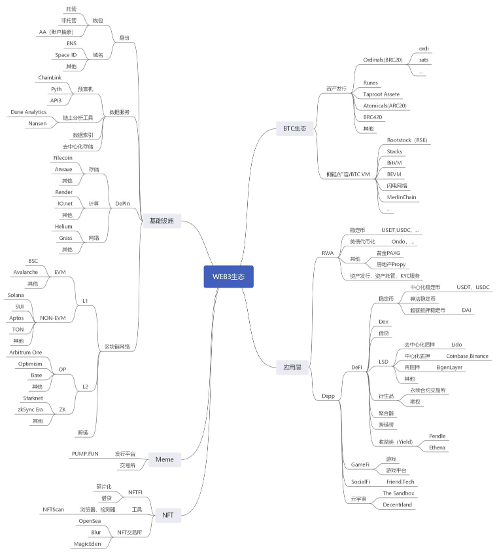

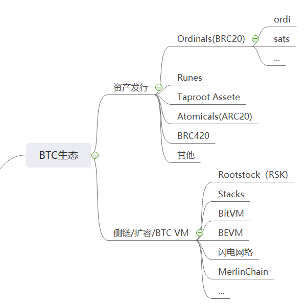

1. Introduction to BTC Ecology

The Bitcoin ecosystem focuses on asset issuance agreements and expansion plans to form a diversified competitive landscape. In the field of asset issuance, BRC20 takes the lead with its first-mover advantage, but faces dust attacks and high gas fees; Runes solves technical bottlenecks through UTXO model innovation and quickly rises to become the underlying infrastructure of DeFi; Taproot Assets and Lightning Network deeply integrate, opening up a new scenario for off-chain asset issuance; BRC420 promotes the innovation of meta-universe and chain games with modular recursive characteristics.

The expansion plan shows a trend of parallelism between "technical route differentiation" and "ecological collaboration": Lightning Network firmly sits as the leader in payments, and is expected to break through functional boundaries after integrating asset agreements; Merlin Chain achieves explosive growth of TVL with community-driven and dual-mining mechanisms; BEVM and BitVM lead technological original breakthroughs with completely decentralized cross-chain and trustless interaction respectively.

The competitive landscape revolves around two major technical camps: UTXO native schools (such as Runes and Lightning Networks) emphasize security and Bitcoin native compatibility, but faces the challenge of insufficient development tools; EVM compatible schools (such as BEVM and Stacks) borrow Ethereum ecological potential energy, but are subject to cross-chain centralization disputes. In the future, modular protocols, cross-chain interoperability and regulatory variables will dominate the ecological evolution - BRC420 may open the era of Bitcoin application chains, BitVM is expected to promote the integration of multi-chain DeFi, and SEC regulatory rulings and the entry of exchange Layer2 may reshape the industry structure. In terms of risks, technological maturity, liquidity fragmentation and geopolitical policies are still key constraints on ecological development.

(I) Asset Issuance Agreement

1. Ordinals ( BRC20 )

• Technical features : By numbering the smallest unit of Bitcoin "Shuo" and attaching any content (inscription), it realizes the issuance of native digital assets, and has the characteristics of pure on-chain storage and non-tampering.

• Representative items :

▪ ordi : The first BRC20 token, the experimental symbolic significance is greater than the functionality, and the market value accounts for 50% of the total market value of BRC20.

▪ sats : Tokens based on "Sheng" as the valuation unit, promote the Bitcoin micro-payment scenario.

• Limitations : Relying on off-chain indexers, UTXO dust problem causes network congestion.

2. Runes

• Innovation value : proposed by Casey, founder of Ordinals, combined with the OP_RETURN opcode and UTXO model, it solves the dust problem of BRC20 and supports asset splitting and unified on-chain management.

• Technical breakthroughs :

▪ Asset transfer is automatically completed through UTXO split to avoid the risk of "burning" of ARC20;

▪ Compatible with Ordinals protocol and implements the FT/NFT unified issuance framework.

• Market impact : Market impact: After the halving is cut in 2024, the main network will be launched, absorbing liquidity of protocols such as BRC20, but not completely replacing other standards. For example, Runes-based lending platform RunesLend allows users to use Runes assets as collateral to borrow and lend, automatically match the lending parties through smart contracts, set interest and repayment periods, effectively leveraging Runes' asset splitting and on-chain management functions, promoting the development of Bitcoin DeFi.

3. Taproot Assets

• Positioning : The asset issuance layer of Lightning Network supports the issuance of stablecoins and other assets within the Lightning Network channel, improving off-chain transaction efficiency.

• Progress : The main network has been opened and is gradually deepening and integrating with the Lightning Network to jointly build a closed loop of 'payment + asset circulation'.

4. Atomicals ( ARC20 )

• Technical features : The dyed coin model based on UTXO is realized through POW mining, and the technical community is highly recognized.

• Problem : Relying on isolated witness storage data, the token splitting function has defects, and some assets are permanently lost due to operational errors.

5. BRC420

• Innovation direction : modular recursive combination of inscriptions, supporting metacosmic asset formats and on-chain royalty protocols, expanding the functional boundaries of Ordinals.

• Case : The RCMS protocol implements multi-inscription nesting to promote applications on complex chains (such as game prop synthesis).

(II) Extension scheme and computing layer

1. Side chain & capacity expansion technology

• Rootstock ( RSK )

▪ The old EVM is compatible with side chains and shares Bitcoin computing power through merger mining, but the centralized bridge mechanism (sBTC) is controversial.

▪ Currently, TVL is about US$300 million, focusing on DeFi scenarios.

• Stacks

▪ Introducing sBTC to realize cross-chain of Bitcoin assets. After Nakamoto upgrades, it supports final settlement of Bitcoin, and the ecosystem covers DEX and lending agreements.

▪ The market value increased by more than 300% in 2024, becoming a representative of the smart contract layer.

• BitVM

▪ Rollup-like solution based on fraud proofs, off-chain computing is implemented through logic gate verification, and the technology is still in the early verification stage.

▪ Potential scenarios: Cross-chain bridge and state channel optimization.

▪ Future development trends: If BitVM's fraud proof technology is successfully verified, it will promote trustless cross-chain interaction between Bitcoin and other blockchains (such as Ethereum and Solana). This will usher in a new era of multi-chain DeFi ecosystem integration. For example, Bitcoin native assets can directly participate in liquidity mining on Ethereum, or conduct high-speed transactions on Solana, thereby improving asset utilization and market liquidity.

• BEVM

▪ Fully decentralized Layer2, using Taproot multi-signature and MAST script to implement BTC cross-chain, and is compatible with the EVM ecosystem.

▪ Technical highlights: significantly reduce the risk of third-party custody, and on-chain applications initially cover DEX, stablecoins and other fields.

• Lightning Network

▪ The orthodox Layer2 plan will support asset issuance after integrating Taproot Assets in 2024, with the number of nodes exceeding 50,000 and the daily trading volume reaches tens of millions of US dollars.

▪ Bottleneck: Complex asset management functions are insufficient and rely on channel liquidity.

• Merlin Chain

▪ Community-driven Layer2, relying on native assets such as BRC420 and Bitmap to accumulate users, TVL ranked first with over US$2 billion.

▪ Innovation model: The dual mining mechanism attracts miners, and joint exchange activities push up popularity.

(III) Competitive pattern and trend

1. Market structure: " multi-dimensional game "

between protocol standards and expansion solutions

( 1 ) Asset issuance agreement: technology iteration accelerates, BRC20 and Runes compete for the dominance

• BRC20 : Still dominates with its first-mover advantage, but faces technical bottlenecks:

▪ The market share is about 55%, and the head tokens represented by ordi and sats contribute more than 70% of the liquidity;

▪ The problems of dust attacks and high gas fees have not been fundamentally solved, and some developers have turned to the Runes ecosystem.

• Runes : Technological innovation drives rapid rise:

▪ The proportion of the agreement market value increased to 30% within 3 months after the main network was launched, and the number of ecological projects increased by 300%;

▪ The asset splitting function based on the UTXO model has become the preferred underlying protocol for Bitcoin DeFi (such as lending and DEX).

• Other protocol differentiation development :

▪ Taproot Assets is deeply bound to the Lightning Network and has supported stablecoin issuance testing;

▪ BRC420 has become the core of chain games and meta-universe infrastructure due to its modular characteristics, and TVL has exceeded US$800 million.

( 2 ) Expansion plan: Ecological collaboration and technological originality become the key to winning

• Lightning Network : Payment scenarios are absolutely king, but they face functional limitations:

▪ The number of nodes exceeded 60,000, and the daily trading volume reached US$120 million;

▪ After integrating Taproot Assets in 2025, a new cycle of "payment + asset circulation" may be launched.

• Merlin Chain : A sample of community-driven Layer2 burst:

▪ TVL has exceeded US$2.5 billion, attracting miners through dual mining mechanisms, and cross-chain pledge of BRC420 assets accounts for 40%;

▪ Jointly launched the "Inscription Mining + Trading Rebate" activity with the exchange, with an additional address of more than 2 million in a single week.

• BEVM and BitVM : Technical originality leads the migration of developers:

▪ BEVM's fully decentralized cross-chain solution attracts more than 500 DApp deployments;

▪ During BitVM verification network testing, if successful, cross-chain without trust will be implemented.

2. Technical route: " Paragraph conflict " of

UTXO native school vs EVM compatible school

( 1 ) UTXO native school ( Runes , Lightning Network)

• Advantages :

▪ Deeply bound to the underlying Bitcoin, with security reaching the highest level in the industry;

▪ Asset issuance does not require dependence on external protocols, and is in line with the philosophy of minimalism of Bitcoin.

• challenge :

▪ There is a lack of development tools and limited smart contract functions;

▪ Ecological fragmentation is severe and cross-protocol interaction costs are high.

( 2 ) EVM compatible patties ( BEVM , Stacks )

• Advantages :

▪ Reuse of the mature Ethereum ecosystem, and the adaptation of the leading DeFi protocols such as Uniswap and Aave have been completed;

▪ Developers have low learning costs and support the rapid deployment of complex DApps.

• challenge :

▪ Controversy over centralization of cross-chain bridges;

▪ Relying on Bitcoin main network settlement, transaction confirmation delay affects user experience.

3. **Future trends: ecological integration and regulatory variable

reshaping pattern**

( 1 ) Modular protocol opens the era of " Bitcoin Application Chain "

• BRC420 recursive inscriptions support multi-chain nesting, and 3 chain games have implemented cross-chain synthesis function of props;

• Taproot Assets may be combined with the Lightning Network to create the first Bitcoin off-chain stablecoin.

( 2 ) Cross-chain technology breakthroughs promote " Bitcoin DeFi 2.0 "

• After BitVM verification is successful, Bitcoin L1 can directly call Solana and Ethereum smart contracts;

• Bitcoin staking derivatives (LST) TVL exceeded US$5 billion, with the annualized yield of the leading protocol reaching 18%.

( 3 ) Regulation and market variables have the greatest uncertainty

• The US SEC may make a ruling on the securities attributes of BRC20 tokens on H1 2025;

• After Bitcoin halving, miners' income declined, and the leading mining pools accelerated the layout of Layer2 node custody business;

• Binance, OKX and others plan to launch their own Bitcoin Layer2, which may break the existing ecological balance.

4. Risk warning

• Technical risks: Frontier solutions are still in their early stages, and there is a possibility of asset losses due to code vulnerabilities;

• Liquidity risk: Differentiation of protocol standards leads to dispersion of funds, and long-tail projects have difficulty in survival;

• Geo-risk: If cryptocurrency supervision is strengthened after the US election, the process of Bitcoin ecological compliance may be hindered.

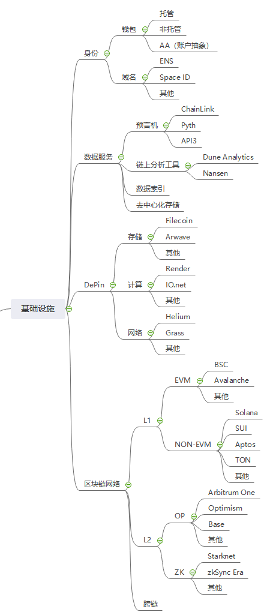

2. Panoramic analysis of infrastructure

Currently, blockchain infrastructure presents three main lines: "security upgrade, performance iteration, and ecological differentiation". In the field of identity management, custodial wallets are driven by compliance and shift to institutional-level multi-signature solutions. Unmanaged wallets reconstruct user experience through MPC technology and account abstraction (AA). ENS and Space ID are competing for the entrance to the identity ecosystem with multi-chain domain names + credit systems. Data services develop in depth to vertical scenarios: ChainLink and Python form a "general data-high-frequency finance" dual oligopoly pattern in the oracle track, Filecoin and Arweave build a storage hierarchical ecosystem, and FVM smart contracts activate storage financialization scenarios.

Blockchain network performance competition enters a new stage: Layer1 presents a triangular game of "Solana performance breaks, TON traffic crushing, and EVM chain compatibility counterattack", Layer2 faces the confrontation between the maturity of ZK Rollup technology and the first-mover advantage of OP-based ecosystems, and the cross-chain bridge cracks the contradiction between security and efficiency through zero-knowledge proof and intention matching mechanism. The competitive landscape highlights three major trends: the wallet has been upgraded from asset tools to DApp aggregation portal, the data service has established barriers around real-time and vertical integration capabilities, and the infrastructure layer competes for the developer ecosystem through modular design. We must be vigilant about the heavy pressure of supervision on cross-chain protocols, the hidden dangers of centralization of ZK technology and the risk of ecological resource dissipation caused by the homogeneity of EVM chains.

(I) Identity Management

1. Wallet

• Hosted wallet

▪Current status : The built-in wallets on the exchange (such as Binance and Coinbase) account for 70% of the new user portals, but the CEX hacking incident in 2024 caused losses of more than US$1.2 billion.

▪Trend : The rise of compliant custody programs (such as Fireblocks institutional-level custody), supporting multi-signal and insurance compensation mechanisms.

• Unmanaged wallet

▪Top projects : MetaMask (monthly active users 45 million), Phantom (dominated by Solana ecosystem, with daily trading volume accounting for 65%).

▪Technical breakthrough : MPC wallet (ZenGo) realizes private key sharding, and the penetration rate of social recovery function reaches 40%.

• Account Abstraction ( AA )

▪Core values : Gas payment, batch transactions, and indirect interaction reconstruction of user experience.

▪Ecological progress :

– Ethereum mainnet ERC-4337 standard is being gradually promoted, and middleware service providers such as Stackup and Biconomy are actively exploring cross-chain AA solutions.

– Middleware service providers such as Stackup and Biconomy lead cross-chain AA solutions.

2. Domain name service

• ENS ( Ethereum Name Service )

▪ Market position : The registration volume exceeds 8 million, and is compatible with 12 chains such as Solana and BNB Chain;

▪Innovation : Launch the ".eth" subdomain auction function, with a maximum transaction price of 50 ETH for a single domain name.

• Space ID

▪Differentiation : one-stop multi-chain domain names (.bnb, .arb), integrating DID authentication and on-chain credit score;

▪Data : The transaction volume in Q4 2024 increased by 320% month-on-month, and the BSC ecosystem accounted for more than 60%.

• SNS ( Solana Name Service )

▪ Positioning : High-performance chain exclusive domain name, transaction confirmation speed reaches milliseconds;

▪Bottleneck : Solana network downtime event causes domain name resolution delay, and the user churn rate is 15%.

(II) Data Service

1. Oracle

• ChainLink

▪ Market share : 65%, supporting more than 1,500 smart contracts;

▪Technical barriers : The DECO protocol ensures data resistance to tampering, and the node pledge volume exceeds US$4 billion.

• Python

▪ Features : Institutional-level high-frequency data (real-time quotations for US stocks and cryptocurrencies), delay less than 300ms;

▪Partner : Jump Trading’s exclusive data source, and the DeFi protocol adoption rate increased by 30% month-on-month.

• API3

▪Innovation model : first-party oracle (data source direct operation node), reducing intermediate layer costs;

▪User cases : Deep integration of derivative protocols such as UMA and Synthetix, and the data call fee is reduced by 50%.

2. On-chain analysis tools

• Dune Analytics

▪Core advantages : User-defined kanban and SQL queries, indexing more than 30 public chains;

▪Data volume : The daily active developers exceeds 150,000, and the number of generated reports exceeded 2 million.

• Nansen

▪ Positioning : Institutional-level monitoring, the Giant Whale Address Tag System covers 98% of the top 1,000 addresses of ETH positions;

▪New features : MEV transaction tracking and NFT liquidity heat map, with over 100,000 paid users.

3. Data index

• The Graph

▪Ecological status : 90% of EVM chain DApps rely on their services;

▪Technical upgrade : Firehose protocol achieves a 10-fold increase in data throughput and reduces index latency to within 1 second.

4. Decentralized storage

• Filecoin

▪Current status : The storage capacity reaches 30 EiB, and the utilization rate has increased to 8% (mainly due to Solana historical data storage cooperation);

▪Breakthrough : FVM smart contracts support storage rental auctions, with annual revenue increasing by 200%.

• Arweave

▪Technical features : permanent storage protocol, single-payment model;

▪Usage rate : The first choice for cold data storage for NFT projects, with a cumulative storage volume exceeding 500TB.

(III) Depin (Decentralized Physical Facilities Network)

1. Storage

• Filecoin

▪Technical features : IPFS-based distributed storage protocol, the storage capacity exceeds 30 EiB, and the utilization rate is increased to 12%;

▪ Innovation : FVM smart contracts support storage rental auctions, with annual revenue growth of 300%;

▪ Challenge : The search market is inefficient, and cold data accounts for more than 90%.

• Arweave

▪Technical features : permanent storage protocol, single-payment model;

▪Used scenarios : NFT project cold data storage is preferred, with a cumulative storage volume exceeding 800TB;

▪Bottleneck : Storage costs are higher than Filecoin, and the adoption rate of small and medium-sized projects is low.

2. Calculation

• Render

▪Technical architecture : distributed GPU computing power network, supporting 3D rendering and AI model training;

▪ Market performance : Hollywood studio adoption rate exceeds 20%, and computing power rental revenue increased by 150% year-on-year.

• IO.net

▪Core value : aggregate idle CPU/GPU resources and provide low-cost AI reasoning services;

▪Usage case : The inference cost of Stable Diffusion model is reduced by 70%, and the average daily call volume exceeds 100 million times.

3. Network

• Helium

▪Transformation direction : from LoRaWAN to 5G network coverage, with more than 500,000 base stations deployed;

▪ Challenge : Operator cooperation is progressing slowly and the user's paid subscription model is low.

• Grass

▪Technical model : build a decentralized IP proxy network through user shared bandwidth;

▪Data : The number of nodes exceeded 2 million, and the average daily data throughput reached 100TB.

( IV ) Blockchain Network

1. Layer1

• EVM compatible chain

▪ BSC :

– TVL is stable at $8 billion, with Gas fees as low as $0.05;

– Problem : Highly centralized (21 verification nodes), DeFi protocol is seriously homogenized.

▪ Avalanche :

– The subnet architecture supports the game chain ecosystem (such as DeFi Kingdoms), with TPS exceeding 8,000;

– Challenge : The pledge rate of native token AVAX is less than 30%, and the ecological incentive effect is limited.

• Non- EVM chain

▪ Solana :

– Performance benchmark : The average daily transaction volume exceeds 800 million transactions, and the cost is 0.05% of Ethereum;

– Breakthrough : Firedancer client is launched, with the goal of achieving a million-level TPS.

▪ SUI :

–Technical features : The object storage model supports high concurrent interaction between GameFi assets;

– Ecological shortcomings : DeFi protocol TVL is less than US$1 billion, and developer tools are scarce

▪ TON :

– Traffic portal : Relying on Telegram’s 900 million users, the monthly active wallet address exceeded 50 million;

– Killer application : Telegram Bot trading robots account for 80% of the on-chain interaction volume.

2. Layer2

• OP Rollup series

▪ Arbitrum One :

– TVL is US$15 billion, accounting for 55% of the Rollup market;

–Bottleneck : The delay in fraud certificates is still 7 days, and the safety hazards in the dispute period have not been resolved.

▪ Blast :

–Native income model : ETH pledge + US Treasury yield, TVL has exceeded US$5 billion in 6 months after its launch;

– Controversy : The team signs multiple contract permissions, and the decentralization process is lagging behind.

• ZK Rollup series

▪ zkSync Era :

–Technical advantages : LLVM compiler supports Rust development, and ZK-Prover efficiency is increased by 3 times;

– Ecological incentives : A US$350 million fund supports GameFi and SocialFi projects.

▪ Scroll :

– Compatibility : fully adapted to EVM bytecode, developer migration costs will go to zero;

– Data : The main network has been online for 9 months, and the number of DApps has exceeded 800.

3. Cross-chain bridge

• status quo :

▪ Header solutions : LayerZero (full-chain interoperability), Wormhole (message delivery protocol);

▪ Security dilemma : The cross-chain bridge attack losses exceed US$1 billion in 2024 (Ronin bridge accounts for 40%).

• Innovation direction :

▪Zero Knowledge Proof : zkBridge implements trustless verification, and the verification speed is increased to within 5 seconds;

▪ Intent Centralization : Socket Protocol matches the optimal cross-link path through user intent.

( V ) Competitive pattern and trend

1. Identity Management: The Battle From Tools to Ecological Entrance

• Wallet battlefield : The proportion of AA wallet users has jumped from 15% in 2023 to 45%, and the share of custodial wallets continues to decline;

• Domain Name Service : ENS faces the impact of Space ID multi-chain strategy, and the market share of .eth has dropped to 50%.

2. Data service: verticalization and real-time upgrade

• Original : Python seizes the financial derivatives market, and ChainLink turns to AI data oracles (such as LLM training data verification);

• Storage protocol : Filecoin virtual machine (FVM) promotes smart storage contracts and forms a "hot data-cold data" layered ecosystem with Arweave.

3. DePIN : Resource integration and vertical scene breakthroughs

· ****Storage : Filecoin and Arweave form a "hot data-cold data" layered ecosystem;

· Computing : AI computing power demand drives Render and IO.net's annual revenue growth by more than 200%;

· Network : Helium 5G and Grass proxy network explore the enterprise-level B-end market.

3. Blockchain network: performance, compatibility and user experience game

• Layer1 : Solana and TON squeeze the EVM chain space with their performance and traffic inlets, and BSC maintains the basic system with low gas fees;

• Layer2 : ZK Rollup technology maturity has improved, and the OP Stack camp is facing challenges such as Starknet and Scroll.

4. Risk warning

• Regulatory risks : The US SEC plans to include cross-chain bridges into the "securities trading platform" supervision, and compliance costs surge;

• Technical risks : Prover centralization issues in ZK Rollup may trigger a trust crisis;

• Ecological risk : Homogeneous competition in EVM compatible chains leads to the dispersion of developers' resources and the survival of long-tail chains is difficult.

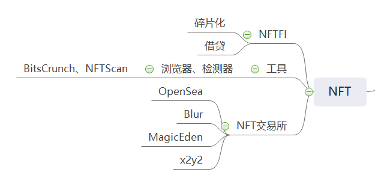

3. NFT ecological panoramic analysis

The NFT ecosystem has formed a diversified system of financial innovation, tool empowerment, transaction competition and regulatory game parallel, and continues to evolve in technology-driven and market iteration.

In the field of NFT Finance ( NFTFi ) , fragmentation technology lowers the asset threshold through standards such as ERC-721E. Unicly takes over US$500 million in the pool segmentation market, while Floor Protocol focuses on the fragmentation of blue-chip NFTs and expands the pledge income scenarios. However, the structural contradictions of liquidity concentration in the leading projects and the securitization review of SEC pose a dual challenge. In the lending track, BendDAO has firmly ranked as the leader in ETH mortgage with a low bad debt rate. NFTfi achieved quarterly growth of 200% through the P2P model, but the insufficient liquidity of long-tail assets and the deviation of oracle valuation still limits the upper limit of development.

The tool service layer focuses on data transparency. BitsCrunch relies on AI detection technology to process more than 100 million API calls per day, effectively suppressing wash trading; NFTScan promotes the exposure rate of forgery projects by 50% through multi-chain data aggregation and copyright tracing, becoming the infrastructure pillar of platforms such as OpenSea and Blur.

The trading market structure is highly dynamic: OpenSea maintains an average monthly transaction volume of US$800 million with professional aggregators and mandatory royalties, but its market share is eroded by Blur; Blur rises rapidly with zero handling fees and token incentives, but it has caused controversy because of the proportion of volume trading exceeding 40%; MagicEden establishes its cross-chain advantage with 60% of transactions on the Solana chain and millisecond speed, while x2y2's DAO governance and leasing functions explore differentiated paths, but faces liquidity dilemma.

Future trends focus on technological integration and compliance breakthroughs: the annual adoption rate of dynamic NFTs surged by 300%, LayerZero cross-chain protocol reduced Gas costs by 60%, and promoted multi-chain interoperability of assets; DeFi integration gave birth to NFT staking derivatives (TVL exceeded US$2 billion) and option hedging tools. However, regulation has become a key variable - the EU MiCA framework requires NFT platform KYC to comply with, and the US SEC's securities recognition of fragmented NFTs may squeeze the space for small and medium-sized creators, while risks such as liquidity exhaustion and contract loopholes continue to threaten ecological health.

The evolutionary logic of this ecosystem is clearly presented: technological innovation expands application boundaries, market game reshapes the competitive landscape, and the compliance process will determine the value allocation and living space in the next stage.

(I) NFT Finance ( NFTFi )

1. Fragmentation

• Technical features : Split a single NFT into multiple ERC-20 tokens (such as the ERC-721E standard) through smart contracts, lowering investment thresholds and improving liquidity.

• Representative Agreement :

▪ Unicly : supports multi-NFT pooling fragmentation, TVL exceeds US$500 million, accounting for 40% of the market share;

▪ Floor Protocol : mainly focuses on the fragmentation of blue-chip NFTs (such as BAYC), and at the same time expands other NFT businesses, with annual pledge income reaching 12%.

• Market impact :

▪ Fragmented NFT trading volume accounts for 15% of the total NFT trading volume, but liquidity is concentrated in the top items;

▪ Regulatory Risk: The US SEC's scrutiny on whether fragmented NFTs are securities is becoming more stringent.

2. Lending and lending

• Operational model : NFT is used as collateral for on-chain lending, supporting fixed interest rates and Dutch auction rates.

• Head platform :

▪ BendDAO : ETH loan accounts for more than 60%, supports blue-chip NFTs such as BAYC and CryptoPunks, and the bad debt rate is controlled within 3%;

▪ NFTfi : Decentralized P2P model, the loan issuance in Q4 2024 increased by 200% month-on-month.

• challenge :

▪ Long-tail NFT collateral has poor liquidity and long liquidation period (average 72 hours);

▪ Valuation relies on oracles, and extreme market volatility leads to a collateral value deviation of more than 30%.

(II) Tools and Services

1. Browser / detector

• BitsCrunch :

▪Core functions : AI-driven NFT wash trading detection, rarity score and price prediction;

▪Data coverage : Supports 12 chains such as Ethereum and Solana, with an average daily API call volume of more than 100 million times.

• NFTScan :

▪ Positioning : Multi-chain NFT data aggregator, providing batch transaction analysis and copyright traceability services;

▪Partners : OpenSea, Blur and other leading platforms integrate their data APIs.

• Industry Value : Increased tool usage rate increases transparency in the NFT market, and the exposure rate of fake projects has decreased by 50%.

(III) Trading Market

1. OpenSea

• Market position : Still the largest comprehensive market, but its share dropped from 80% in 2023 to 45%;

• Innovation strategies :

▪ Launched the "OpenSea Pro" professional version, with the aggregator function supporting price comparison and cross-platform orders;

▪ Integrate ERC-721C on-chain royalty standards and force creator royalties.

• Data : Monthly transaction volume is stable at US$800 million, but users are lost to emerging platforms such as Blur.

2. Blur

• Subversion mode :

▪ Zero platform handling fees, incentivize market makers through token airdrop (accounting for 70% of transaction volume);

▪ The first "Bid Pool" batch quotation system is designed to support one-click floor price NFT.

• Market impact :

▪ Trading volume surpassed OpenSea in Q1 2024, accounting for 35% of the market share;

▪ Controversy: Excessive reliance on token incentives leads to over 40% of transactions in volume trading.

3. MagicEden

• Positioning : The Solana ecosystem dominated the market and expanded to Ethereum and Bitcoin Ordinals;

• Core Advantages :

▪ The transaction speed is milliseconds, and the Gas fee is 1/100 of Ethereum;

▪ Launched the "Diamond Hand" reward program, and long-term holders receive airdrops on platform tokens.

• Data : The NFT transaction volume on Solana chain accounts for more than 60%, with 3 million monthly active users.

(IV) Competitive pattern and trend

1. Market structure

• Trading Platform :

▪ Blur and OpenSea compete for comprehensive market dominance, with the combined share of the two exceeding 70%;

▪ MagicEden is firmly in the leader of Solana's ecosystem and actively expands its multi-chain strategy.

• NFTFi :

▪ The centralization of lending agreements, BendDAO and NFTfi account for 80% of the market share;

▪ Fragmentation protocols penetrate into vertical fields (such as game assets, music copyright).

2. Technical route

• Dynamic NFT :

▪ The metadata is updated in real time based on on-chain data (such as changes in game prop attributes), and the adoption rate increases by 300% annually;

▪ Chainlink VRF and IPFS dynamic storage have become the technical standard.

• Cross-chain NFT :

▪ LayerZero full-chain communication protocol supports NFT seamless cross-chain, reducing Gas costs by 60%;

▪ Bitcoin Ordinals and Ethereum NFT bidirectional mapping protocol are being tested.

3. Future trends

• Deepening of DeFi fusion :

▪ NFT-staking derivatives (such as NFT-LST) TVL exceeded US$2 billion;

▪ NFT option protocols (such as Hook Protocol) are launched to hedge the risk of price volatility.

• Regulatory compliance :

▪ EU MiCA regulations include NFTs in the regulatory framework, requiring trading platforms to implement KYC;

▪ The US IRS intends to impose capital gains tax on NFT transactions, triggering users' demand for anonymization.

4. Risk warning

• Liquidity risk : Long-tail NFT liquidity is exhausted, and 90% of the project trading volume is reduced to zero;

• Technical risks : Dynamic NFT smart contract vulnerabilities lead to frequent metadata tampering events;

• Policy risks : Different countries identify NFT securitization attributes and trigger a surge in compliance costs.

• Regulatory Risk : In addition to the US SEC's review of fragmented NFTs, the EU also plans to include NFTs in the MiCA regulatory framework, requiring issuers to conduct KYC and transparent disclosures. This may cause some NFT projects to exit the market due to excessive compliance costs. For example, some small artists' NFT works may not meet complex compliance requirements, affecting the diversity of the NFT market.

4. Panoramic analysis of Meme track

The Meme track presents the ecological characteristics of " high explosion and high fluctuation coexist " . Its core has shifted from disorderly hype to a dual-track parallel Meme track with technology-driven and compliance exploration with issuance platform - trading market - community consensus as the core chain, forming a market structure that has both explosive power and fragility. The leading issuance platform PUMP.FUN has an absolute advantage in Solana chain with its low cost and "one-click coin issuance" mechanism. Although its innovative mechanisms such as "social map detection" effectively filter the robot's brush volume, the extremely short life cycle and high Rug Pull rate still expose the cruelty of the speculative bubble. Emerging competitors try to break through the situation through DAO governance and cross-chain collaboration, but Gas cost and liquidity depth are still key bottlenecks.

The trading market shows liquidity stratification between CEX and DEX : centralized exchanges dominate high-liquidity tokens through strategic innovation, while Solana-based DEX undertakes long-tail assets with low slippage and aggregation trading functions. With its anti-censorship characteristics and cross-chain support, decentralized exchanges have gradually become a new hub for the game between Meme coins and institutional funds.

At the technological evolution level, AI -driven has become a key variable: AI tools have greatly improved issuance efficiency, and risk control systems have strengthened real-time monitoring of risks; cross-chain protocols have tried to break the single-chain restrictions, but regulatory compliance pressures restrict their progress. Future trends focus on compliance survival and community economic revolution : anonymous projects turn to privacy chains, DAO model promotes democratization of token parameters, and SocialFi integrates fan economy and reshapes the governance framework.

(I) Meme distribution platform

1. PUMP.FUN

• Technical Features:

▪ One-click coin issuance protocol based on the Solana chain, token creation, liquidity pool injection and contract locking are completed within 5 minutes;

▪ Innovation mechanism:

– Social graph detection : Verify real users by binding Twitter/X accounts and filter the robot’s brush volume;

– Token destruction : If the preset liquidity threshold is not reached within 24 hours, the token will be automatically destroyed and funds will be returned.

• Market performance:

▪ The cumulative issuance of more than 800,000 tokens in 2024, with the peak daily trading volume exceeding US$350 million;

▪ Success stories:

– BOOM : Dogecoin imitation market, with a peak market value of US$150 million, and the number of addresses held by the community exceeds 100,000;

– SOLANA - Trump : Political Meme coin, trading volume soared by 500% during the US election cycle.

• Controversy and Risk :

▪ More than 95% of the tokens have less than 48 hours of life, and Rug Pull events account for 30%;

▪ The platform extracts 2% transaction fee + 10% liquidity pool fee, and its annual revenue is estimated to exceed US$600 million.

2. Emerging competitors

• PooCoin (Ethereum Chain) :

▪ Supports multi-chain deployment and integrates token market value prediction AI tools, but the Gas cost is 5 times higher than the Solana chain;

▪ The market share is less than 8%, and the liquidity depth is far inferior to PUMP.FUN.

• Memeland (cross-chain protocol) :

▪ The first "community governance and coin issuance" model, and the token parameters are determined by DAO voting;

▪ TVL exceeded US$50 million in the testing phase and has not been fully opened yet.

(II) Meme Exchange

1. Centralized exchange ( CEX )

• Head platform strategy:

▪Binance:

– Establish a "Meme Innovation Zone" and the listing of coins must be voted through community (such as PEOPLE, FLOKI);

– Launch Meme index futures, allowing 3x leverage to hedge volatility risks.

▪ Bybit :

– The “zero handling fee Meme season” attracted retail investors, with a peak daily trading volume of US$1.8 billion;

– The number of robots brushes has caused sharp price fluctuations, and some tokens have increased or decreased by more than 1,000% intraday.

• Data Insights :

▪ The transaction volume of Meme coins in the top five CEXs accounts for more than 70%, with Binance, Bybit and OKX dominating;

▪ Coin fee stratification: Blue chip Meme projects (such as DOGE, SHIB) are free of charge, and the maximum payment of SGD is US$2 million.

2. Decentralized exchange ( DEX )

• Solana :

▪ Raydium : PUMP.FUN token core trading market, supports instant liquidity pool creation, with slippage below 0.5%;

▪ Jupiter : The aggregator integrates cross-DEX prices, and the Meme currency transaction volume accounts for 80% of the total transaction volume of the platform.

• Ethereum system :

▪ Uniswap V4 : Launches the "Meme Liquidity Mining Plug-in", and LP can obtain protocol token airdrops;

▪ ShibaSwap : Focus on Meme Coin Swap and supports staking SHIB to earn income, but TVL is less than US$100 million.

• Innovative tools :

▪ PumpBot : Telegram robot integrates DEX transactions, and users automatically complete on-chain purchases through the instruction "/buy token name";

▪ Meme sniper tool : real-time monitoring of PUMP.FUN new coins, supporting millisecond-level rush transactions.

(III) Competitive pattern and trend

1. Market structure

• Distribution side :

▪ PUMP.FUN monopolizes the Solana chain market (85% share), and Ethereum chain competitors are difficult to break through due to high gas fees;

▪ Cross-chain protocols such as Memeland try to break the single-chain monopoly, but the ecological synergy effect has not yet appeared.

• Transaction side:

▪CEX and DEX differentiation:

– CEX dominates high liquidity tokens (such as DOGE and SHIB), with trading volume accounting for 65%;

– DEX takes over long-tail assets, and Solana Chain DEX accounts for 60% of the market share.

2. Technology evolution

• AI -driven distribution :

▪ The platform integrates AI to generate token names, icons and marketing copy, and the issuance efficiency is increased by 10 times;

▪ The AI risk control system monitors the Rug Pull mode in real time, with an early warning accuracy of over 80%.

• Cross-chain issuance protocol :

▪ PUMP.FUN plans to support Ethereum and Aptos multi-chain deployment, and Gas costs may become a key bottleneck;

▪ LayerZero full-chain communication protocol tests Meme coins seamlessly cross-chain transfer.

3. Future trends

• Compliance attempts :

▪ The EU requires Meme coin issuers to submit KYC, and anonymous projects turn to privacy chains (such as Monero);

▪ The US SEC sued PUMP.FUN for securities issuance, and the platform may introduce mandatory information disclosure.

• Community Economic Revolution :

▪ The MemeDAO model is emerging, and token parameters are decided by community proposal voting (such as destruction mechanisms, tax and fee allocation);

▪ Social tokens (SocialFi) merge with Meme coins, and the fan economy drives market value growth.

4. Risk warning

• Technical risks :

▪ Smart contract vulnerabilities lead to funds stolen (the loss of Solana chain Meme project in 2024 exceeded US$200 million);

▪ The rush to trade robots lead to an over 30% deviation in transaction prices for ordinary users.

• Market risk :

▪ High volatility triggered a leverage liquidation, and a Bybit user lost $5 million in a single day;

▪ Liquidity depletion leads to the zeroing of tokens, and the average survival cycle of long-tail projects is less than 72 hours.

• Regulatory risks :

▪ India, South Korea and other countries have banned CEX from launching Meme coins, and geopolitical fragmentation has intensified;

▪ The US IRS has included Meme currency income in the tax audit focus, and tax evasion penalties have surged.

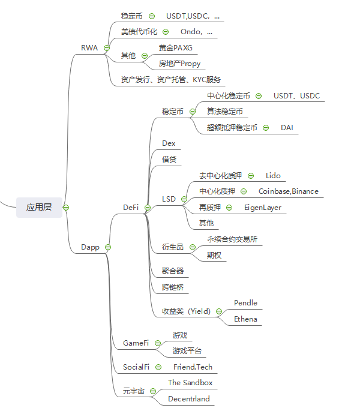

V. Panoramic analysis of the application layer

The application layer takes RWA asset tokenization and DApp scenario innovation as its core pillars, presenting a pattern of technological breakthroughs and compliance exploration in parallel.

In the RWA track, stablecoins (USDT/USDC) are firmly at the core of payments with a market value of US$160 billion, but the US Payment Stablecoin Act has intensified compliance pressure. Ondo TVL, the leader in U.S. bond tokenization, has exceeded US$5 billion, attracting 70% of institutional funds at low thresholds; the cumulative transaction volume of the real estate tokenization platform Propy has reached US$800 million, but cross-jurisdictional rights confirmation is still a bottleneck. In terms of supporting services, compliant issuance platforms such as Security and Polymesh dominate the market, institutional-level custody solutions such as Fireblocks improve asset security, and zero-knowledge proof technology is gradually integrated into the on-chain identity verification process.

DApp ecological differentiation is obvious:

DeFi track : Uniswap V4 dominated the average daily trading volume of US$5 billion. Aave V4 pushed the bad debt rate to below 0.5% through isolation pools and cross-chain clearing. LSDFI (such as Pendle) promoted the ETH staking derivatives market size to over US$50 billion.

GameFi field : Axie Infinity transformed into the free-to-play earning model and daily active users rebounded to 500,000, but the users of the Metaverse Platform stayed for less than 30 minutes, and the problem of land liquidity depletion was not solved (such as the average price of Decentraland fell 85% from its peak).

SocialFi Exploration : Friend.Tech's social tokenization model has been cold, and the token price has fallen by 90% from its peak. Decentralized social protocols (such as Lens and Farcaster) try to integrate NFT functions to regain users.

Future trends focus on AI integration and regulatory breakthroughs:

Technology-driven: AI agents promote DeFi automated clearing and strategy optimization, and ZK-Rollup technology significantly improves Layer2's privacy and transaction efficiency; if Bitcoin OP_CAT upgrade is passed, the potential of native smart contracts may be released, which may push the BTCFi market size to exceed 10 billion US dollars.

Compliance Challenge: The US SEC's review of the securitization attributes of RWA platforms is becoming stricter. The EU MiCA framework requires stablecoin issuers to reserve 100%, and the compliance costs of small and medium-sized projects have surged.

( I ) RWA (real world asset tokenization)

1. Stable Coin

• USDT/USDC

▪ 市场地位 :合计市值超1600亿美元,占稳定币市场90%;

▪ 监管动态 :美国《支付稳定币法案》要求100%现金储备,Circle已获纽约州牌照。

2. 美债代币化

• Ondo

▪ 产品结构 :短期美债代币(OUSG)年化收益4.8%,最低投资门槛1美元;

▪ 规模 :TVL突破50亿美元,机构投资者占比超70%。

3. 其他资产

• 黄金( PAXG )

▪ 机制 :1:1锚定伦敦金库实物黄金,市值达30亿美元;

▪ 流动性 :CEX日均交易量不足1亿美元,套利效率低。

• 房地产( Propy )

▪ 用例 :通过NFT实现产权分割与链上交易,累计成交额超8亿美元;

▪ 局限 :法律确权依赖线下流程,仅限特定司法管辖区。

4. 配套服务

• 资产发行 :Securitize、Polymesh等合规平台主导;

• 资产托管 :Anchorage、Fireblocks提供机构级托管方案;

• KYC :Circle Verite、iden3支持链上身份验证,隐私计算技术(如零知识证明)逐步集成。

( 二 ) DApp 生态

1. DeFi

• 稳定币

▪ 中心化稳定币 :USDT/USDC主导支付与交易场景;

▪ 算法稳定币 :Frax v3引入部分抵押机制,市值回升至15亿美元;

▪ 超额抵押稳定币 :MakerDao的DAI通过超额抵押加密资产并由社区治理机制动态调整参数,以维持与美元的1:1价值锚定

• DEX

▪ 头部协议 :Uniswap V4日均交易量50亿美元,Solana链DEX(Orca)占比提升至25%;

▪ 创新 :意图交易(UniswapX)减少MEV,交易成本降低30%。

• 借贷

▪ Aave V4 :引入隔离池与跨链清算,坏账率降至0.5%以下;

▪ Compound :转向机构借贷市场,企业贷款占比超40%。

• LSD (流动性质押衍生品)

▪ 去中心化质押 :Lido,通过多节点运营商实现非托管质押,支持用户质押ETH获取stETH代币,质押市占率约65%,TVL超350亿美元;

▪ 中心化质押 :Coinbase、 Binance 等中心化交易所提供的质押服务,集中式服务通常提供更简单直接的用户体验,但相对于去中心化服务,用户对资产的控制权较低。

▪ 再质押 :代表协议Eigenlayer,允许用户将已质押的ETH再次质押,赚取多重收益;

• 衍生品

▪ 永续合约 :dYdX链上衍生品交易量占比超60%,V4版本支持自定义交易对;

▪ 期权 :Hegic v2推出无滑点期权交易,机构做市商占比提升至50%。

• 聚合器

▪ 1inch :整合200+ DEX,Gas优化算法节省用户成本15%;

• 跨链桥 :LayerZero全链交易占比超70%,但安全争议未解。

• 收益类

▪ Pendle :允许用户通过拆分资产的本金(PT)与收益权(YT)进行灵活交易,支持收益策略优化与远期收益对冲;;

▪ Ethena :合成美元协议,通过抵押ETH及做空期货合约生成收益型稳定币USDe,提供链上无风险利率与高杠杆衍生品策略。

2. GameFi

• 链游

▪ 头部项目:

– Axie Infinity :转型免费玩赚模式,日活用户回升至50万;

– Parallel :TCG卡牌游戏,NFT卡牌二级市场交易量超3亿美元。

• 游戏平台

▪ Immutable :以太坊ZK-Rollup游戏链,入驻项目超300个;

▪ Gala Games :节点销售模式遇冷,转型订阅制会员服务。

3. SocialFi

• Friend.Tech

▪ 模式 :社交代币化(Key)与内容订阅结合,创作者分成占比95%;

▪ 瓶颈 :用户流失率超80%,代币价格较峰值下跌90%。

4. 元宇宙

• The Sandbox

▪ 生态进展 :土地空投吸引Gucci、HSBC等品牌入驻,日活用户不足10万;

▪ 挑战 :3A级内容匮乏,用户停留时长均值低于30分钟。

• Decentraland

▪ 转型策略 :聚焦虚拟会议与展览场景,2024年承办超500场企业活动;

▪ 数据 :土地均价较2022年峰值下跌85%,流动性枯竭。

( 三 )竞争格局与趋势

1 . RWA :合规化与规模化并行

• 美债代币化 :Ondo、Maple Finance竞争机构资金入口;

• 房地产 :Propy与Chainlink合作实现链下-链上产权确权验证。

2 . DApp 生态:用户体验与合规重构

• DeFi :LSDFI与ReStaking推动ETH质押衍生品市场超500亿美元;

• GameFi :3A游戏《Illuvium》上线或成行业转折点;

• SocialFi :去中心化社交协议(Lens、Farcaster)集成Meme与NFT功能。

3 . 风险提示

• 监管风险 :美SEC起诉RWA平台涉嫌发行未注册证券;

• 市场风险 :元宇宙土地泡沫破裂,流动性危机蔓延至关联DeFi协议。

• 信用风险 :资产发行方的信用状况和资产本身的质量。资产需经过严格的线下确权和评估,以确保资产的真实性和合法性。