Coinbase: The future of currency has arrived and has just begun

Reprinted from jinse

06/11/2025·6DSource: [Coinbase 2025Q2 encryption status report](https://www.coinbase.com/zh-cn/blog/the-state-of-crypto-the-future-of- money-is-here) ; compiled by: AIMan@Golden Finance

Key points:

-

Six out of 10 Fortune 500 executives said their company is working on blockchain-related projects.

-

The number of stablecoin holders has reached 161 million, exceeding the total population of the top ten cities in the world.

-

Nearly one-fifth of Fortune 500 executives said the on-chain plan is a key component of the company's future strategy, a 47% increase year-on-year.

One-third of SMEs use cryptocurrencies, which is twice as much as in 2024.

-

The scale of real-world asset tokenization has exceeded US$21 billion as of April 2025, an increase of 245 times year-on-year.

-

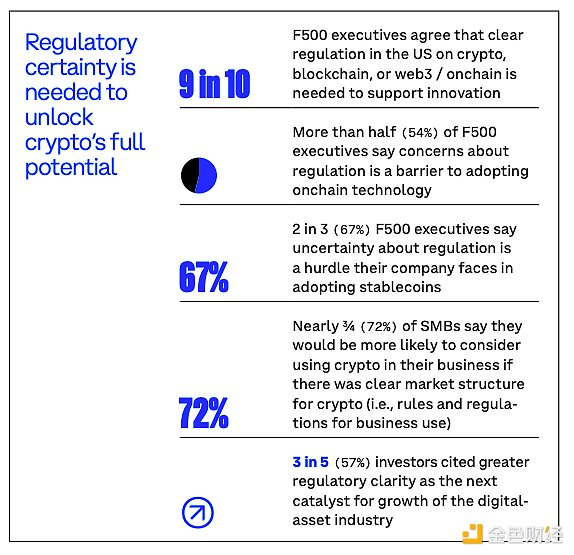

Nine out of 10 Fortune 500 executives believe that the United States needs to develop clear regulatory rules for cryptocurrencies, blockchain or Web3/on-chain fields to support innovation.

-

The global stablecoin supply increased by 54% year-on-year.

introduction

16 years after Bitcoin was launched, the development of modern blockchain technology has made it safe to say that the future of currency has arrived. Cryptocurrency holdings are more common than many think: stablecoin transfers are at an unprecedented level; more than one-third of small and medium-sized businesses use cryptocurrencies in their businesses; and six in ten Fortune 500 executives say their companies are working on blockchain-related projects.

But this is just the beginning. Nearly one in five Fortune 500 executives said the on-chain plan is a key component of the company's future strategy (a year- on-year increase of 47%), and more than four in five institutional investors plan to increase their investment exposure to cryptocurrencies this year.

The development of cryptocurrencies is particularly evident among small and medium-sized enterprises, which are the backbone of the US economy. In 2025, the application of cryptocurrencies has achieved "three doubled growth". Compared to last year, the number of SMEs using cryptocurrencies doubled (34% in 2025 and 17% in 2024), the number of SMEs using stablecoins doubled, and the number of SMEs paying or accepting payments from cryptocurrencies doubled. Looking ahead, demand may only continue to intensify, as more than four-fifths of SMEs believe cryptocurrencies can help solve at least one financial pain point (82%) and are interested in using cryptocurrencies in their business (84%). As the motto says, “As the mainstream market develops, the economy will develop with it.”

Therefore, the future of currency has arrived and has just begun. But obviously, to fully realize the potential of cryptocurrencies, higher regulatory certainty is needed. This is why the future of U.S. cryptocurrency innovation is so important through market structure and stablecoin legislation. Nine out of 10 Fortune 500 executives agree that clear regulation is needed to support innovation, with more than three-fifths of investors citing higher regulatory clarity as the next catalyst for growth in the digital asset industry, and nearly three-quarters (72%) of SMEs say they are more likely to consider using cryptocurrencies in their business if the market structure of cryptocurrencies is clearly defined.

This is Coinbase’s seventh Crypto Status Report, which examines the adoption of cryptocurrencies by businesses, SMEs and investors, and demonstrates the role that cryptocurrencies, blockchain and other Web3 technologies can play in updating the global financial system to benefit businesses and consumers.

The report covers the following:

1. More and more top American companies are beginning to get involved in on- chain business.

2. Small and medium-sized enterprises adopt cryptocurrencies faster.

3. The adoption of stablecoins and other tokenized assets is expanding rapidly.

4. Institutional investors are increasing their exposure to cryptocurrencies.

5. Higher regulatory certainty is needed to unlock the full potential of cryptocurrencies.

1. More and more top American companies are involved in on-chain business

The on-chain business is huge. Among Fortune 500 executives:

-

Six out of 10 people say their company is in the process of on-chain planning.

-

Nearly half (47%) said companies have increased their investment in on-chain technology.

-

The number of on-chain projects per company increased by 67% year-on-year, from 5.8 to 9.7

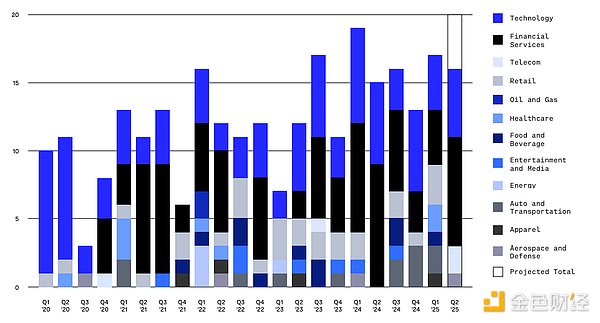

In Fortune 500 companies, on-chain plans and use cases are diversifying:

In the first quarter of 2025, Fortune 100 companies announced 17 unique on-

chain plans, which is on par with the second highest quarterly activity on

record, with a total of 46 unique on-chain plans over the past three quarters

(third quarter 2024 to first quarter of 2025). While financial services and

technology companies remain the most planned industries on the chain, the last

three quarters (third quarter 2024 to first quarter 2025) have shown that

participation in automotive and transportation, retail, food and beverage, and

healthcare companies is also increasing.

In the first quarter of 2025, Fortune 100 companies announced 17 unique on-

chain plans, which is on par with the second highest quarterly activity on

record, with a total of 46 unique on-chain plans over the past three quarters

(third quarter 2024 to first quarter of 2025). While financial services and

technology companies remain the most planned industries on the chain, the last

three quarters (third quarter 2024 to first quarter 2025) have shown that

participation in automotive and transportation, retail, food and beverage, and

healthcare companies is also increasing.

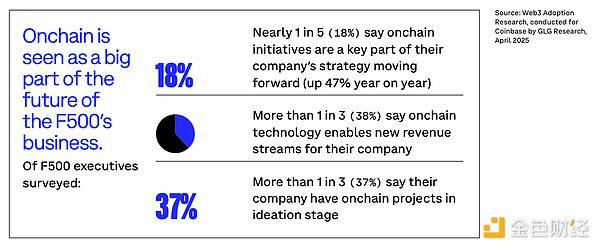

On-chain is the top priority for business

The chain is regarded as an important part of the future business of Fortune 500 companies. Among the Fortune 500 executives surveyed:

-

18% said on-chain plans are a key component of the company's future strategy (a year-on-year increase of 47%).

-

More than a third (38%) say on-chain technology has brought new revenue streams to the company.

-

More than one-third (37%) say the company has on-chain projects in the conceptual stage.

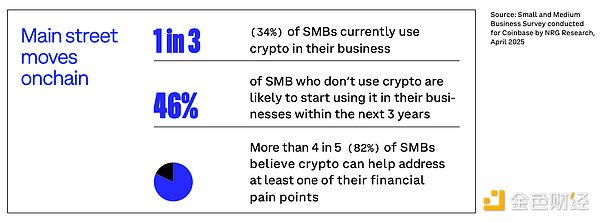

2. Not just large enterprises – small and medium-sized enterprises are

transforming faster to the chain

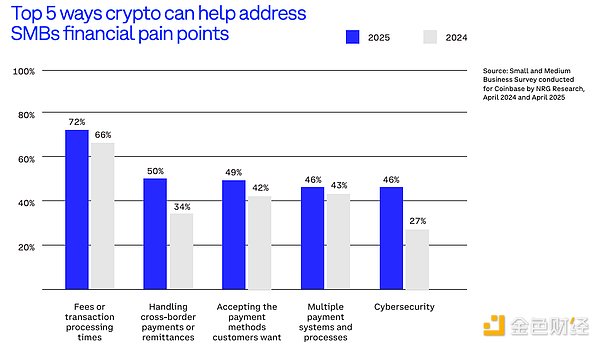

The future of currency is most obvious among small and medium-sized enterprises, which are the backbone of the US economy. On-chain technology, especially payment technology, is extremely attractive to businesses that regard transaction fees and processing time as the primary financial pain points.

-

One third (34%) of SMEs currently use cryptocurrencies in their business.

-

46% of SMEs that are not using cryptocurrencies may start using it in their business within the next 3 years.

-

More than four-fifths (82%) of SMEs believe cryptocurrencies can help solve at least one financial pain point.

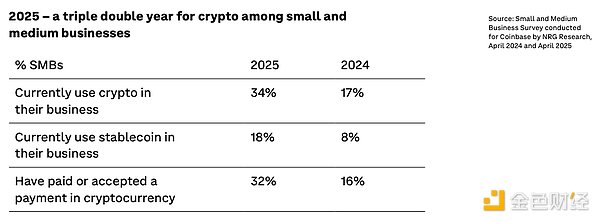

2025 is the year of "three double growth" for cryptocurrencies for small and medium-sized enterprises. Compared to last year, the number of SMEs using cryptocurrencies, the number of SMEs using stablecoins, and the number of SMEs paying or accepting payments from cryptocurrencies have all doubled.

Therefore, it is no surprise that more than four-fifths of SMEs (84%) are

interested in using cryptocurrencies in their business, up from nearly two-

thirds (65%) a year ago.

Therefore, it is no surprise that more than four-fifths of SMEs (84%) are

interested in using cryptocurrencies in their business, up from nearly two-

thirds (65%) a year ago.

Cryptocurrencies help address the major financial pain points faced by SMEs.

82% of SMEs said cryptocurrencies could help solve at least one pain point facing businesses, up from 68% a year ago.

In 2025, more than half (57%) of SMEs believe that adopting cryptocurrency will save businesses money, up from 42% a year ago.

3. The adoption rate of stablecoins and other tokenized assets is

expanding rapidly

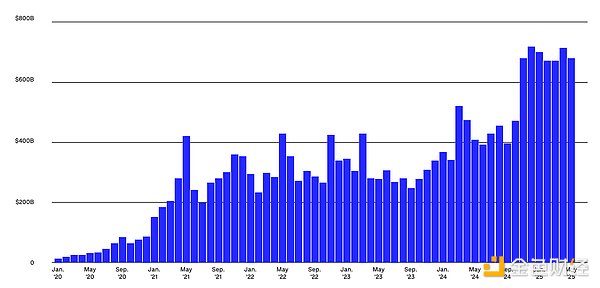

The natural transfer volume of stablecoins has reached an unprecedented level, with the highest two-month transfer volume in history last year. A monthly transaction volume record of $719 billion was set in December 2024, followed by a transaction volume of $717.1 billion in April 2025.

Adjusted monthly stablecoin transfers have surged since the beginning of 2020.

Adjusted monthly stablecoin transfers have surged since the beginning of 2020.

The annual settlement volume of stablecoins has increased significantly since 2019, surpassing the annual settlement volume of the global remittance market and PayPal, and is also close to the settlement volume of Visa.

The number of holders of stablecoins continues to grow, with more than 160 million holdings, which exceeds the total population of the top ten cities in the world, 6 times the population of the New York metropolitan area, and more than X the number of daily active users in the United States. They can circle the earth with hand in hand for 6 circles.

As of early May 2025, the supply of stablecoins accounted for nearly 10% of the currency in circulation in the United States. As of the end of May 2025, the total supply of stablecoins has reached US$247 billion, an increase of nearly 54% over the previous year. In April 2025, USDC's market value reached an all-time high of US$62 billion. Circle and Tether, two issuers of USDC and USDT, currently hold more U.S. Treasury bonds than major countries such as Germany, highlighting the increasingly important position of stablecoins in the global financial markets.

Stablecoins can help solve some of the biggest financial pain points

This growth stems from the shared belief of consumers and Fortune 500 and SMEs that stablecoins can help solve some of the biggest financial pain points. 47% of Fortune 500 executives and 82% of SMEs said slow transaction speed and/or high transaction fees were financial pain points, while 31% of Fortune 500 executives and 30% of SMEs said cross-border payment challenges were also financial pain points. Therefore, it is no surprise that 89% of SMEs believe that there is at least one benefit to using stablecoins.

Some examples of stablecoins addressing existing financial pain points:

1. Remittance <br> Pain points: International remittance via wire

transfer can incur large expenses (in many cases, more than 50% of the

remittance amount may be consumed by fees and exchange rates), and it takes a

long time (usually 1-5 working days to complete).

Stablecoin help: Stablecoin directly solves these pain points, it can achieve

nearly instant and low-cost cross-border transfers, bypassing traditional bank

intermediaries.

2. Pay processing fees <br> Pain points: Companies usually incur large

costs due to credit card processing fees, and the fees per transaction may

range from 1.5% to 3.5%. These expenses can erode profit margins, especially

for small and medium-sized enterprises.

Stablecoin Help: Accepting stablecoin payments can bypass traditional credit

card networks, thereby reducing transaction costs.

3. Global salary payment

Pain points: Managing the salary of employees around the world involves

dealing with different regulations, currencies and banking systems.

Stablecoin Help: Paying salaries with stablecoins allows companies to quickly

and safely pay employees and freelancers around the world.

4. Inflation protection <br> Pain points: People in high-inflation

countries face the problem of rapid decline in purchasing power, and it is

difficult to maintain storage or conduct financial planning. The value of

local currencies may fall every day, and gaining stable foreign currencies are

often restricted or strictly controlled by the government, forcing people to

hold depreciated assets or rely on the black market.

Stablecoins Help: Stablecoins provide a solution that provides a digital asset

that maintains stable value, often pegged to the dollar, allowing individuals

to protect their savings from inflation and trade with more reliable means of

store of value.

5. People with insufficient bank accounts and bank accounts

Pain points: Individuals who immigrate or live in areas with limited banking

infrastructure often have difficulty obtaining basic financial services such

as savings accounts, remittances or credit. In many cases, barriers such as

document requirements, high fees or geographical isolation prevent them from

participating in the formal financial system. Even in the United States, the

Federal Deposit Insurance Corporation (FDIC) found that 19 million households

had insufficient bank accounts in 2023 and 5.6 million households had no bank

accounts.

Stablecoins Help: Stablecoins can help bridge this gap, allowing anyone with a

smartphone and internet connection to store value, send money and access to

global financial networks without the need for traditional bank accounts.

This ability to address some of the biggest financial pain points drives interest in businesses of all sizes. Among Fortune 500 executives:

-

7% say their company currently uses or holds stablecoins.

-

Nearly three-ten (29%) said their companies plan to use or are interested in stablecoins, compared with 8% in 2024, a 3.6-fold increase year-on-year.

-

Two-thirds say stablecoins can be part of a solution to provide customers with faster and lower fees to pay.

-

More than half (58%) say regulated stablecoins can reduce costs for companies in areas such as international payments or supplier settlement.

SMEs are also excited about the potential of stablecoins:

-

18% of SMEs currently use stablecoins, more than double the 8% in 2024.

-

36% of SMEs said they received requests from customers, employees, or suppliers/suppliers to use stablecoins (more than double the 17% a year ago).

-

81% of SMEs are interested in using stablecoins in their business, compared with 61% a year ago.

With Circle launching a cross-border remittance network, Ramp launching stablecoin cards, Stripe and Bridge launching "stablecoin financial accounts" in 101 countries, SWIFT enables native stablecoin functionality, Meta re- exploring stablecoins after selling Diem, and realizing Mesh stablecoin settlement through Apple Pay, etc. (to name only a few), stablecoins are beginning to become more and more mainstream, and this is just the beginning of the rise of stablecoins.

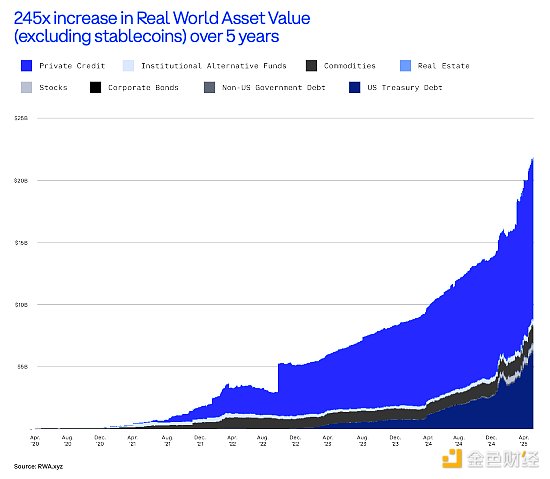

The growth of real-world asset tokenization

Real-world asset tokenization has increased 245 times from US$85 million in April 2020 to more than US$21 billion in April 2025. Private credit accounts for 61% of the total tokenized assets, followed by Treasury bonds (30%), Commodities (7%) and Institutional Funds (2%).

As the industry matures, real-life asset tokenization has expanded to many different business use cases, and this is expected to continue. For example:

1. Treasury bond/cash management tokenization

Pain points: Companies usually deposit idle cash into bank accounts with

little or no income, or rely on manual processes to allocate funds to short-

term Treasury bonds through traditional brokers or funds. This puts them in

the face of opportunity costs, settlement delays and lack of 24/7 liquidity.

For international companies, due to capital controls, counterparty risks and

limited channels for obtaining foreign currency-denominated assets, the

friction is even higher.

Real-world asset use cases: Tokenized Treasury settlement is faster,

programmable, and often provides transparent real-time reporting. Especially

for Web3 native companies and decentralized autonomous organizations (DAOs),

tokenized Treasury bonds provide a way to earn money from Treasury bonds

without transferring funds off-chain.

2. Invoice/account receivable tokenization

Pain points: For many companies, especially small and medium-sized

enterprises, cash flow bottlenecks may cause problems. Traditional invoice

factoring solutions are slow, paperwork is heavy and geographically

restricted. Financing terms are often unfavorable, access is limited, and

liquidity is spread across regional suppliers. This makes it difficult for

growth companies to obtain short-term working capital.

Real-world asset use cases: Tokenizing invoices and accounts receivable

enables businesses to unlock liquidity. It can be segmented and made available

to global investors in real time, improving capital access and driving more

efficient pricing. Smart contracts can automatically track payments and

enforce terms while potentially reducing fraud and management overhead.

3. Private credit tokenization

Pain points: Traditionally, private credit is only open to large institutions and high net worth investors, and its issuance and services are handled manually through opaque, poor liquidity channels and banks. For businesses (especially in underserved areas or industries), obtaining private loans often requires dealing with a decentralized, high-cost financing network, and limited investor coverage. For investors, participating in the private credit market requires a long-term lock-in period and lacks convenient exit options.

Real-world asset use cases: Private credit tokenization enables wider participation by lowering the issuance and investment thresholds, making it easier to utilize retail fund management scale (AUM). This unlocks a deeper and more diverse funding pool for borrowers. In addition, tokenized debt can be traded in the secondary market, providing investors with potential exit liquidity and improving pricing efficiency for issuers.

These are the pain points of scale that can be solved by real asset tokenization. As of April 2025, the scale of private credit tokenization has grown from nearly zero to US$12 billion, with Figure leading the market and accelerating growth - from the fourth quarter of 2024 alone, the market value increased by US$2.5 billion. The tokenized U.S. Treasury bond size grew from less than $500 million in October 2022 to over $6 billion in April 2025. BUIDL and BENJI have become market leaders, holding 54% of the market share and attracting a large amount of capital inflows.

4. Institutional investors are increasing their exposure to

cryptocurrencies

2024 is a bumper year for cryptocurrencies, thanks to interest in new ETF products. Bitcoin and Ethereum ETFs are among the most successful ETFs ever.

The top ten Bitcoin ETFs have attracted a cumulative inflow of US$50 billion, which is twice the cumulative inflow of capital in the first year of the top ten ETFs in history.

Although record ETF trading volume is driven by retail investors (retail investors hold 79% of Bitcoin ETFs), the speed at which institutions adopt Bitcoin ETFs is also setting a record. In the first three quarters after launch, Bitcoin ETFs outperformed other best-performing ETFs in both institutional asset management size (AUM) and number of holders.

The Ethereum ETF attracted a net inflow of $3.5 billion, and in the first quarter after its launch, its institutional AUM and holders outpaced other best-performing ETFs.

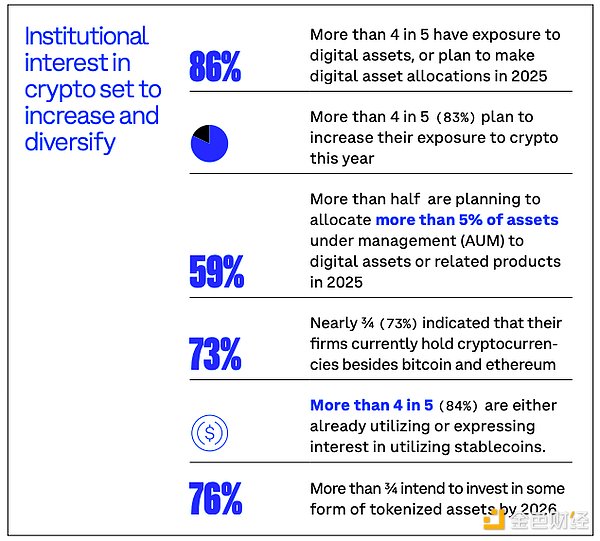

In 2025, this interest is expected to increase and diversify. In January 2025, in a survey of 352 institutional investor decision makers in partnership with EY-Parthenon:

More than four-fifths (86%) of institutional investors already hold digital

assets or plan to allocate digital assets in 2025.

More than four-fifths (86%) of institutional investors already hold digital

assets or plan to allocate digital assets in 2025.

More than four-fifths (83%) of institutions plan to increase their exposure to cryptocurrencies this year.

More than half (59%) of institutions plan to allocate more than 5% of asset management scale (AUM) to digital assets or related products by 2025.

Nearly three-quarters (73%) of institutions say their companies currently hold cryptocurrencies other than Bitcoin and Ethereum.

More than four-fifths (84%) of institutions have been using or expressing interest in using stablecoins.

More than three-quarters of institutions intend to invest in some form of tokenized assets by 2026.

V. Higher regulatory certainty is needed to unlock the full potential of

cryptocurrencies

So far, this report has shown that the future of the currency is not only coming, but its prospects are brighter than ever. However, to unlock this potential, it is key to increase regulatory certainty around cryptocurrencies, Web3 and blockchain technologies in the United States.

-

Nine out of 10 Fortune 500 executives agree that the United States needs to establish clear regulatory rules for cryptocurrencies, blockchain or Web3/on-chain fields to support innovation.

-

More than half (54%) of Fortune 500 executives said concerns about regulation are a barrier to the adoption of on-chain technology.

-

Two-thirds (67%) of Fortune 500 executives said regulatory uncertainty is a barrier their companies face when adopting stablecoins.

-

Nearly three-quarters (72%) of SMEs said they were more likely to consider using cryptocurrency in their business if there was a clear cryptocurrency market structure (i.e. rules and regulations for commercial use).

-

Three-fifths (57%) of investors rank higher regulatory clarity as the next catalyst for growth in the digital asset industry.

Cryptocurrency legislation is also active at the state level. More than 131 different bills on Bitcoin and cryptocurrencies have been passed or are considering in 38 states. While many new laws are exciting, such as Arizona ensuring unclaimed cryptocurrency properties can be held in native form, and New Hampshire and Texas create strategic bitcoin reserves, some states are considering new regulatory regimes that will create conflicting consumer protection requirements for cryptocurrencies. Federal market structure legislation is needed to provide common legal and regulatory clarity benchmarks to protect consumers and encourage innovation regardless of the consumer’s postal code.

The United States needs to cultivate a growing talent demand rather than continue to lose talent overseas.

To win the battle for crypto talent, higher regulatory certainty is also needed. Since the launch of Ethereum in 2015, the number of cryptocurrency developers has increased by 39% per year. Given the growth that cryptocurrencies are experiencing and will continue to experience, this is a very needed talent.

However, although the U.S. still has 39% of developers (as of November 2024), its share has dropped by half since 2015. India is the second largest contributor, accounting for 12%, and has a significant growth.

Among Fortune 500 executives, concerns about available trusted talent are now the main obstacle to adoption. Half of SMEs say they may look for candidates familiar with cryptocurrencies the next time they fill a financial, legal or IT/technology position. Clear cryptocurrency rules are key to keeping developers in the United States and the key to the United States continuing to lead the world in cutting-edge technological innovation.

The future of currency has arrived and it has just begun. But if the United States wants to lead the way forward, we need clear rules.