Citi's "stablecoin" research report: digital dollar, from crypto-punk to government banks

Reprinted from chaincatcher

04/29/2025·14DOrganize & compile: Web3 Xiaolu

The origins of the public blockchain network can be traced back to the release of the Bitcoin White Paper in 2008 and the birth of the Genesis Block in 2009. However, the conceptual basis of blockchain has actually begun to be gradually constructed as early as the decades since the 1970s. Nevertheless, so far, blockchain has remained relatively limited in its application range in the financial and public sectors.

The open source and decentralized nature of blockchain is rooted in a core concept that mathematics and code can guarantee privacy and freedom . Judging from the origin of its crypto-punk, blockchain is not only a technological innovation, it also has a strong political color, essentially an anti-establishment philosophical idea, representing an opposition to existing institutions (both banks or governments). Crypunk is a group of people who advocate utilizing encryption and privacy enhancement technologies to drive social and political change.

Public key cryptography first appeared in the mid-1970s, while hash functions and Merkle trees were born in the late 1970s. At the same time, the development history of modern Internet is also worth paying attention to. In the 1980s, Arpanet began to adopt the TCP/IP protocol, and by the early 1990s, the World Wide Web was officially born. However, during the booming Internet in the 1990s, the important element of "digital currency Digital Money" was missing.

The Bitcoin white paper released in 2008 proposed to establish a " peer-to-peer electronic cash system ". This concept was gradually implemented in the following years, and the use of Bitcoin increased significantly. As of April 2025, Bitcoin remains one of the dominant cryptocurrencies in the crypto ecosystem, with a market share of up to 64%.

Entering the 2020s, the narrative surrounding blockchain has undergone an almost 180-degree turn. The once anti-establishment movement has now gradually become mainstream . Between 2023 and 2024, "Real World Asset Tokenization (RWA)" has become one of the dominant narratives of the crypto ecosystem. As of the end of March 2025, one of the largest holders of Bitcoin was the US Bitcoin ETF Fund. In addition, other US institutions, including the U.S. government, are also among the top ten Bitcoin holders. In 2025, a few days before the inauguration of the 47th US President, the $TRUMP meme coin was launched on the Solana blockchain.

As a digital currency based on blockchain network, stablecoins have huge development potential. In recent years, the use of stablecoins has shown a rapid growth trend. It is expected that the use of stablecoins may further increase significantly between 2025 and 2030 as regulatory transparency continues to increase (especially in the United States).

In addition, public chains can also bring higher transparency and enhanced trust. Whether in wealthy or poor countries, public institutions are working to improve their trust index, and these characteristics of public chains are exactly what they need urgently. The adoption of blockchain continues to advance with the evolution of regulation and the demands for transparency and accountability.

As the above review of blockchain history in 2025, how should we look forward to the future of stablecoins and blockchain? Citi GPS's latest research report "Digital Dollars - Banks and Public Sector Drive Blockchain Adoption" may give the answer, focusing on two key areas: new financial instruments (such as stablecoins), and modernizing legacy systems.

Therefore, we compiled this in a more detailed way, and its discussion on the GPT moment of the stablecoin is worth learning from.

Coincidentally, two years ago on May Day, we were also compiling Citi GPS's article " Money, Tokens, and Games (Blockchain's Next Billion Users and Trillions in Value) ". The subtitle of the article is Blockchain's Next Billion Users and Trillions in Value.

In the 2023 report, Citi predicts that by 2030, Billion Users will come from: currency, social, gaming. Looking back in 2025, in addition to the flash in SocialFi and GameFi at that time, this gap will be filled by users holding cryptocurrencies or stablecoins, which is also the origin of Citi's 2025 stablecoin research report.

The full text is 18,000 words, the following enjoy:

Key Takeaways

1 Driven by regulatory changes, 2025 has the potential to become the "ChatGPT" moment for blockchain to be used in the financial and public sectors.

2 By 2030, the total supply of stablecoins in circulation may grow to $1.6 trillion under our expected benchmark scenario and $3.7 trillion under our expected optimistic scenario. Even so, if the challenges in application and integration persist, this number could be close to $500 billion.

3 We expect the supply of stablecoins to remain denominated in US dollars (about 90%), rather than the central bank digital currency (CBDC), which will promote its own currencies.

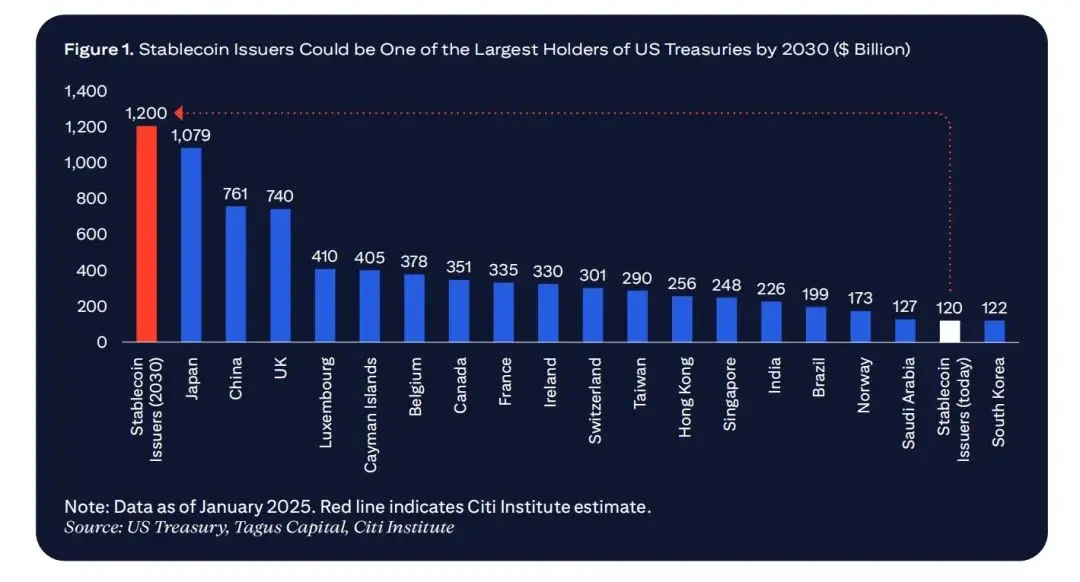

4 The U.S. stablecoin regulatory framework may drive net new demand for U.S. Treasury bonds, allowing stablecoin issuers to become one of the largest holders of U.S. Treasury bonds by 2030.

5 Stablecoins pose a certain threat to the traditional banking ecosystem through deposit replacement. But they may provide new service opportunities for banks/financial institutions.

6 The public sector’s application of blockchain is also gaining increasing attention, thanks to continued attention to transparency and accountability for public spending, reflected in the U.S. government’s DOGE (Department of Government Efficiency) initiative and blockchain pilot projects by central banks and multilateral development banks.

7 The main use cases of public sector blockchain include: expenditure tracking, subsidy issuance, public record management, humanitarian aid activities, asset tokenization, and digital identity.

8 While on-chain transaction volumes in the public sector may initially be small and still have high risks and challenges, an increase in public sector interest may be an important signal for the wider use of blockchain.

1. Why is the large-scale adoption of blockchain now?

Why is it said that 2025 may become the "ChatGPT moment" for blockchain to be used in the financial and public fields?

-

The supportive stance of U.S. regulators on blockchain is expected to be a year to change the industry landscape. This could lead to wider adoption of blockchain-based currencies and stimulate other use cases in the U.S. private and public sectors.

-

Another potential catalyst is the ongoing focus on transparency and accountability of public spending.

These changes are built on developments over the past 12-15 months, including the EU’s crypto asset regulatory market (MiCA), the growth in user demand reflected in cryptocurrency ETF issuance, the institutionalization of cryptocurrency trading and custody, and the U.S. government’s establishment of strategic Bitcoin reserves.

While banks, asset management companies, public sector and government agencies have increased their participation in blockchain, they still lag behind some more optimistic expectations. The reality is that digital finance already exists in the fields of consumer and institutional finance, including proprietary databases and centralized systems such as Internet banks. We are now seeing the accelerated convergence of Internet native technologies, currencies, and blockchain and digital native use cases.

The government's adoption of blockchain is divided into two categories: empowering new financial tools and modernizing systems. The system is upgraded by integrating shared ledgers to enhance data synchronization, transparency and efficiency.

Stablecoins are currently the main holders of U.S. Treasury bonds and are beginning to affect global financial flows. The growing popularity of stablecoins reflects the ongoing demand for dollar-denominated assets.

Artem Korenyuk, Digital Assets – Client, Citi

1.1 Stablecoins are on the rise

Stablecoins are cryptocurrencies pegged to stable assets such as the US dollar, and the main catalyst that drives them to gain wider acceptance may be the clarity of U.S. regulation. This can enable stablecoins, as well as blockchains (from a broader perspective) to better integrate into the existing financial system.

Given the dominance of the US dollar in international finance, changes in stablecoins in the United States will affect the broader global system.

The U.S. government seems keen to promote the development of the onshore digital asset industry, one of its priorities for improving innovation and efficiency. In January 2025, the U.S. President’s executive order titled “Strengthening U.S. leadership in the field of digital financial technology” established a digital asset task force responsible for developing a federal regulatory framework for the industry.

Against the backdrop of regulatory-friendly, digital assets are increasingly integrated with existing financial institutions, laying the foundation for the growth of stablecoin usage, and macroeconomic factors such as demand for the US dollar in emerging and cutting-edge markets have also further supported this trend.

According to DefiLlama data, as of the end of March 2025, the total value of stablecoins exceeded US$230 billion, 30 times that of five years ago. This reflects to a certain extent the growth in the total value of cryptocurrencies (1,400% in the five years ended March 2025) and the growth in institutional demand. Our analysis shows that under the benchmark scenario, the total supply of stablecoins could reach $1.6 trillion, with bear and bull market scenarios reaching about $0.5 trillion to $3.7 trillion, respectively.

Treasury Demand: Establishing a US stablecoin regulatory framework will support the demand for US dollar risk-free assets at home and abroad. Stablecoin issuers must purchase U.S. Treasury bonds or similar low-risk assets as an indicator of their possession of secure underlying collateral. Under the benchmark scenario, we expect U.S. Treasury bond purchases to exceed $1 trillion. By 2030, stablecoin issuers may hold more U.S. Treasury bonds than the total amount currently in any jurisdiction.

1.2 Future Challenges

The development of stablecoins also faces resistance and challenges. While the dominance of the dollar may evolve over time, and the euro or other currencies will be driven by national regulations, many non-U.S. policymakers may view stablecoins as tools of dollar hegemony.

The goal of blockchain is to align currency flows with the speed of the Internet and global commerce. Stablecoins can be a key tool to achieve this. The first step is the clarity of legislation and regulation. In addition, legal safeguards are needed.

Ryan Rugg, Digital Assets – Services, Citi

The geopolitical situation remains turbulent. If the world continues to move towards a multipolar system, policymakers in China and Europe will likely be keen to push for central bank digital currencies (CBDCs) or stablecoins issued in their own currencies. Policymakers in emerging and cutting-edge markets will also remain vigilant about the local risks brought about by dollarization.

Stablecoins and central bank digital currencies (CBDCs) are both attempts to create digital currencies, but they differ in terms of technical architecture and governance. The issuer of CBDC is a central bank, while private entities can issue stablecoins. CBDC is usually inspired by the principles of blockchain, but is not based on public chains. Given the demand for the US dollar in wholesale and financial transactions, especially in jurisdictions with high currency volatility, stablecoins may play the role of EuroDollar 2.0.

Therefore, we expect the stablecoin market to remain dominated by the US dollar in the next few years. In the benchmark scenario, we expect that approximately 90% of the stablecoin supply in 2030 will be denominated in US dollars, although lower than the current nearly 100%.

There is a risk of a run for stablecoins and may trigger a spreading effect. In 2023, stablecoins were decoupled about 1,900 times, of which about 600 were large stablecoins. Large-scale decoupling events may suppress liquidity in crypto markets, trigger automatic liquidation, weaken trading platforms' redemption capabilities, and may have a wider spreading effect on the financial system. For example, in March 2023, news of the bank banking in Silicon Valley triggered a massive redemption from USDC.

A recent report from Galaxy Digital noted that Tether provided about $8 billion in funding, accounting for about 25% of the total crypto lending business, and noted that if Tether uses depositors’ funds to issue these loans, it “violates some banking systems and faces serious systemic risks.”

Note: Tokenized deposits are tokenized representations of commercial deposits, and each token is backed by retail or institutional deposits. Deposit tokens are native tokens on the blockchain, which directly represents retail or institutional deposits in the form of tokens. To date, most bank projects can be classified as “tokenized deposits.” Deposit tokens are mostly in pilot or early stages, such as the Guardian project, the Regulated Responsible Network (RLN), or the Helvetia project.

1.3 Does the public sector need blockchain?

Trust and transparency are essential to maintaining public support for governments and institutions.

Trust is the new currency of the government and they need to build confidence and trust with their citizens. Governments can continue to use centralized databases and traditional software solutions, but may miss the fundamental changes brought about by blockchain.

Saqr Ereiqa, Secretary General, Dubai Digital Asset Association

Blockchain introduces a trust-based approach to data management for public sectors. Trust in traditional systems stems from authoritative institutions—such as governments verify their own records—and blockchain allows encryption of proof of authenticity. Trust is rooted in the technology itself.

The immutability of blockchain ensures that information cannot be changed once recorded, thus providing tamper-proof records for sensitive public data such as land registration, voting systems, and financial transactions. While other technologies can also be tamper-free, they usually require a trusted party to execute.

Cross-border activities, especially payment of international funds through institutions such as the World Bank or humanitarian aid projects, are important use cases for blockchain. International capital flows may be opaque and it is difficult to effectively verify whether the resource reaches the intended recipient. Blockchain can provide transparency for complex transactions, even in remote or unstable areas where financial institutions are not functioning well.

Building a blockchain with a simple database that is enough to meet demand is like driving a Ferrari to a corner store – expensive, inefficient and unnecessary. If all inputs and outputs are controlled by one entity, there is no real advantage to blockchain. Its true value will only be revealed when the exchange of value that needs to be trusted.

Artem Korenyuk, Digital Assets – Client, Citi

1.4 Expert opinion

A. Digital Trust Revolution

Siim Sikkut was formerly the Chief Information Officer of the Government of Estonia (2017-2022) and is currently a member of the Digital Advisory Committee of the President of Estonia. He is also a managing partner of Digital Nation.

Q: What prompted Estonia to adopt blockchain?

Estonia's digital transformation stems from real needs. As a small country with a population of only a few million, efficiency and productivity are crucial. In the late 1990s, with the rise of the Internet, Estonia began experimenting with digital solutions in the government and banking sectors.

These early initiatives demonstrated significant advantages, allowing the country to operate beyond its land area and resource constraints. This success prompted Estonia to make a strategic commitment to digital innovation. Estonia has adopted an iterative approach to test emerging technologies, identifying which technologies work and promoting successful solutions. This approach has spawned groundbreaking initiatives such as online voting and e-residence, both of which were experimental projects and later gradually became an integral part of Estonia's digital infrastructure. Blockchain follows a similar trajectory. Estonia adopts blockchain not to respond to the crisis, but to ensure efficient digital governance.

Q: How does Estonia use blockchain in government operations? Why?

Estonia mainly uses blockchain to ensure data integrity in government systems. The key challenge is maintaining trust—making sure citizens can trust the security and accuracy of their data. While encryption and cybersecurity help solve confidentiality and availability issues, governments need a solution to verify the integrity of their records.

The key question is: How to trust the system administrator and the log files it provides?

In the early 21st century, Estonia adopted a custom blockchain, KSI (keyless signature infrastructure), as an additional layer of trust. Today, it has been applied to various government databases including the National Health Registration System.

It is worth noting that the blockchain does not store actual records, but records the time and person metadata of access or modification of records. For example, it does not store an individual's blood type, but records when and who accessed or modified the entry. This approach has two key advantages. First, it ensures user privacy and regulatory compliance. Secondly, it is impractical to store large data sets on a chain from a cost and performance perspective.

Q: What potential use cases do you think there are in the future blockchain?

One promising area is digital documentation, where blockchains can enhance the security, transparency and efficiency of welfare, grants and public sector resource allocation. By providing an immutable ledger, blockchain can reduce fraud, strengthen accountability, and ensure seamless verification across institutions.

Another potential use is to manage and protect storage value, especially in government projects that allocate financial aid or subsidies. Tokenization also has potential, especially for government departments involved in fiscal redistribution.

B. Overall digital policy

Julie Monaco is global head of public sector banking at Citibank.

Q: What does a successful national digital policy look like?

Successful national digital policies are not only about technology, but also about vision and goals. It begins with bold leadership and commitment to building an inclusive, people-centered digital economy. Authorizing the Digital Tsar to coordinate priorities in artificial intelligence, data privacy and cybersecurity is key.

It is estimated that strategic investment in digital identity identification systems can unlock access for 1.7 billion people, save 110 billion hours of labor time, and increase 6% of emerging market GDP. According to Juniper Research, 3.6 billion people have registered worldwide and are in a strong momentum. Countries such as Estonia, India and Singapore have demonstrated the infinite possibilities that policy-led innovation can bring.

Q: What role should blockchain play in achieving accountability, transparency and efficiency as part of a successful digital policy?

Blockchain can definitely play a role in successful digital policies, especially in strengthening accountability, transparency and efficiency. It can create untampered records and automate audit trails through smart contracts, which can potentially reduce fraud, improve regulation and build trust in public systems. In terms of efficiency, it can simplify services such as taxation or welfare allocation by reducing bureaucracy.

But it is not a panacea, but if used properly, blockchain can be a powerful tool to help governments operate with greater integrity, responsiveness and efficiency.

2. GPT moment of stablecoins

2.1 How does stablecoins work?

Stablecoins are cryptocurrencies designed to stabilize their value by pegging their market value to underlying assets. The underlying assets can be fiat currencies (such as US dollars), commodities (such as gold), or a basket of financial instruments.

Key components of the stablecoin ecosystem include:

-

Stablecoin Issuer: The entity that issues stablecoins and is responsible for managing its underlying assets, usually holding a value equivalent to the supply of stablecoins in the underlying assets.

-

Blockchain ledger: After the stablecoin is issued to the public, transactions will be recorded on the blockchain ledger. The ledger provides transparency and security by tracking ownership and flow of stablecoins between users.

-

Reserves and collateral: Reserves ensure that each token can be redeemed at its pegged value. For stablecoins secured by fiat currencies, these reserves usually include cash, short-term government bonds and other current assets.

-

Digital Wallet Provider: Provides digital wallets, which can be mobile applications, hardware devices, or software interfaces, allowing holders of stablecoins to store, send and receive their currency.

How do stablecoins maintain their anchor exchange rate?

Stablecoins rely on different mechanisms to ensure their value is consistent with underlying assets. Fiatcoin-backed stablecoins maintain their anchor exchange rate by ensuring that each issued token can be exchanged for an equal amount of fiat currency.

The main stablecoins in the market

As of April 2025, the total circulation of stablecoins has exceeded US$230 billion, an increase of 54% since April 2024. The top two stablecoins dominate the ecosystem, accounting for more than 90% of the market share by value and transaction volume, with Tether (USDT) leading the way, followed by USD Coin (USDC).

In recent years, the trading volume of stablecoins has grown rapidly. Adjusted by Visa Onchain Analytics, stablecoin trading volume reached between $650 billion and $700 billion per month in the first quarter of 2025, about double the level from the second half of 2021 to the first half of 2024. Transactions that support the crypto ecosystem have always been a major use case for stablecoins.

USDT, the largest stablecoin with market capitalization, was launched on the Bitcoin blockchain in 2014 and expanded to the Ethereum blockchain in 2017, thus enabling its application in decentralized finance (DeFi). In 2019, USDT further expanded to the widely used Tron network in Asia due to faster and lower costs. USDT is mainly operated overseas, but times are changing.

We will certainly see more players (especially banks and traditional players) entering the market. USD-backed stablecoins will continue to dominate. Ultimately, the number of participants will depend on how many different products are needed to cover the main use cases – and the number of participants in this market may be more than the credit card network market.

Matt Blumenfeld, Global And US Digital Assets Lead, PWC

2.2 Drivers of Stablecoin Adoption

According to Erin McCune, Founder & Principal Consultant, Forte FinTech, the channel factors for stablecoins are as follows:

-

The practical advantages of stablecoins (fast speed, low cost, available 24/7) are creating demand in developed and emerging economies. Especially in countries where instant payments are not yet widely available, small and medium-sized enterprises (SMBs) in these countries are not fully serviced by existing companies, while multinational corporations want to make global capital transfers easier. Cross-border transaction costs in these countries remain high, banking technology is immature, and/or financial inclusion lag.

-

Macro demand (inflation hedging, financial inclusion) is driving stablecoins to be adopted in areas with severe inflation. Consumers in countries such as Argentina, Türkiye, Nigeria, Kenya and Venezuela use stablecoins to protect their funds. Today, more and more remittances are being transferred in the form of stablecoins, and consumers without bank accounts can now use digital dollars.

-

Recognition and integration of existing banks and payment providers is key to the legalization of stablecoins (especially for institutional and enterprise users) and can rapidly expand its scope of use and applicability. Mature and scaled payment network operators and core processors can increase transparency and promote integration with digital solutions businesses and merchants rely on. The clearing mechanism between various stablecoins between banks and non-bank institutions is also crucial to achieving scale. Technology improvements for consumers (easy to use wallets) and merchants (embedding stablecoins acceptance into acquisition platforms accessible via APIs) are removing barriers that once restricted stablecoins to the edge of cryptocurrencies.

-

The long-awaited regulatory clarity will allow banks and the wider financial services industry to introduce stablecoins in retail and wholesale sectors. Transparency (audit requirements) and consistent liquidity management (reliable face value) will also simplify operational integration.

Matt Blumenfeld, Global And US Digital Assets Lead, PWC said the channel factors for stablecoins are as follows:

- User Experience : The global payment landscape is increasingly shifting to real-time digital transactions. But the adoption of each new payment method faces the challenges of customer experience—whether it is intuitive, whether it can see the use cases, and whether the value is clear. Any organization that successfully enhances the customer experience—whether it is for retail users or institutional users—will stand out in their respective fields and become leaders.

The integration with our current payment methods will drive the next wave of application. In terms of retail, this will be reflected in the popularity of bank cards or mobile wallets. Institutional terms, this will be reflected in simpler, more flexible and more cost-effective settlements.

-

Regulatory clarity : After the introduction of new stablecoin regulatory regulations, we can see a serious suppression of innovation and application by regulatory uncertainty on a global scale. The introduction of MiCA regulations, clarity in Hong Kong's regulation and progress in U.S. stablecoin legislation has triggered a surge in activity aimed at simplifying the flow of institutions and consumers' funds.

-

Innovation and efficiency : Institutions must see stablecoins as the driving force for more agile product development, which is difficult to achieve in today’s era. This means providing a simpler, more creative or more attractive medium to enhance traditional bank deposits in the form of, for example, earnings generation, programmability, and composability.

2.3 Potential market for stablecoins

As Forte Fintech Erin McCune pointed out, any forecast of the potential size of the stablecoin market requires caution. There are many factors for market volatility, and our own analysis also shows that the market volatility range is very wide.

We constructed a forecast range based on the following factors that drive the growth of stablecoin demand:

-

Convert some US dollar holdings from paper money and outside the United States from banknotes to stablecoins —U.S. banknotes held overseas are usually a hedge against local fluctuations, and stablecoins are a more convenient way to obtain such hedging. In the United States, stablecoins can be partially used for certain payment functions and held for this purpose.

-

Reconfigure some of the US dollar short-term liquidity held by U.S. and international households and businesses as stablecoins to support cash management and payment operations. Because stablecoins are easy to use (such as 24/7 cross-border payments, etc.), and if regulations allow, stablecoins may partially replace earning assets.

-

Furthermore, we assume that the short-term liquidity substitution trend of EUR/GBP is similar to that of the short-term liquidity of the US dollar, which is held by domestic households and businesses, albeit at a much smaller scale. In the benchmark case, our optimistic scenario for 2030 forecasts that the stablecoin market will still be mainly driven by the US dollar (about 90%).

-

The growth of the public crypto market , where stablecoins are used as facilitators of settlement or monetary acceptance; in part because of the growth in institutional adoption of public crypto assets and the widespread use of blockchain technology. In our benchmark scenario, we assume that the growth trend of stablecoin issuance will continue from 2021 to 2024.

-

Our benchmark scenario for the size of the stablecoin market in 2030 is estimated at $1.6 trillion, the optimistic scenario is estimated at $3.7 trillion, and the pessimistic scenario is estimated at $0.5 trillion.

Note: The stock of total currency (circulating cash, M0, M1 and M2) in 2030 is calculated using the nominal GDP growth rate. The euro zone and the UK may issue and adopt local currency stablecoins. China may adopt the sovereign central bank digital currency (CBDC), and the possibility of using foreign private issuance of stablecoins is less likely. Bear market forecast for non-USD stablecoins in 2030: US$21 billion; benchmark forecast: US$103 billion; bull market forecast: US$298 billion.

2.4 Stablecoin market outlook and use cases

Erin McCune is the founder and chief consultant of Forte Fintech. She has over 25 years of consulting experience in the payment field. Her consulting efforts focus on commercial payments, cross-border transactions, and the intersection of corporate finance, banking and enterprise software. Prior to founding Forte Fintech, she served as a partner at Bain and Glenbrook Partners.

Q: What are the optimistic and cautious outlooks on the recent size of the stablecoin market and the potential factors driving its development?

Predicting the growth of the global stablecoin market requires great confidence (or ego) because there are still many unknowns. Based on this, I put forward the following optimistic and pessimistic predictions:

The most optimistic forecast is that as stablecoins become the daily medium for instant, low-cost, low-friction transactions around the world, the market size will expand by 5-10 times. The relatively optimistic forecast is that by 2030, the value of stablecoins will increase exponentially from the current $200 billion to $1.5 trillion-2.0 trillion, and will penetrate global trade payments, P2P remittances and mainstream banking.

This optimism relies on several key assumptions:

-

Regulatory policies are loose in key areas – not only Europe and North America, but also markets with the largest demand for local fiat currency alternatives, such as sub-Saharan Africa and Latin America.

-

Establish real trust between existing banks and new entrants, as well as broad trust among consumers and businesses in the integrity of stablecoin reserves (e.g., 1 dollar stablecoin = equivalent value of 1 dollar-fiat currency)

-

Reasonable distribution of income throughout the value chain to facilitate cooperation; and

-

Technology that connects old and new infrastructure is widely adopted to promote structural efficiency and scale. For example, merchant acquiring agencies have begun to use stablecoins. For wholesale payment applications, corporate finance and accounts payable (AP) solutions, and commercial banks need to make adjustments. Commercial banks will need to deploy tokenization and smart contracts.

In a pessimistic scenario, the use of stablecoins remains limited to crypto ecosystems and specific cross-border use cases (mainly poor liquidity currency markets, which currently account for only a small part of global GDP). Geopolitical factors, resistance to digital dollarization and widespread adoption of CBDC will further hinder the growth of stablecoins. In this case, the market value of stablecoins may stabilize between $300 billion and $500 billion , and have limited roles in the mainstream economy.

The following factors will lead to more pessimistic scenarios:

-

If one or more major stablecoins experience reserve failure or decoupling events, this will seriously undermine the trust of retail investors and businesses.

-

The friction and cost associated with using stablecoins for daily shopping—whether it is the inability of remittance recipients to buy groceries, pay tuition and rent, or the inability of businesses to easily use funds to pay wages, inventory, etc.

-

Retail CBDCs have not yet gained attention, but stablecoins may not be very suitable in areas where digital cash alternatives in the public sector can scale.

-

In areas where stablecoins are increasingly receiving attention and local fiat currency correlations are further weakened, central bank governors may respond by strengthening supervision.

-

If the stablecoins supported by full reserves are large enough, this could "take up" a large number of security assets to support them, potentially limiting economic credit.

Q: What are the current and future use cases of stablecoins?

As with any other payment method, the relevance and potential growth of stablecoins must be considered based on specific use cases. Some use cases have received widespread attention, while others remain at the theoretical stage or are obviously impractical. Here are the use cases (from large to small) that contribute to stablecoin transaction volumes in the current (or near future):

-

Cryptocurrency trading : Individuals and institutions use stablecoins to trade digital assets is currently the largest use case, accounting for 90% to 95% of stablecoin transaction volume. This type of activity is largely driven by algorithmic trading and arbitrage. In the maturity stage, trading (retail + DeFi activity) may still account for about 50% of stablecoin usage, given the continued growth of the crypto market and its reliance on stablecoin liquidity.

-

B2B Payment (Company Payment) : According to Swift, the vast majority of traditional agency bank transaction amounts can reach their destination within minutes via Swift GPI. But this mainly occurs between centralized monetary banks, between highly liquid currencies, and during bank business hours. There are still many problems of inefficiency and unpredictability, especially when conducting operations in low- and middle-income countries. Businesses that use stablecoins to pay overseas suppliers and manage capital operations may occupy a considerable share of the stablecoin market. Given that global B2B capital flows are as high as tens of trillions of dollars, even if a small part of them turn to stablecoins, in the long run, it may be equivalent to 20% to 25% of the total stablecoin market size.

-

Consumer Remittances : Despite the steady shift from cash to digital currencies, pressure from regulators and focused efforts of new entrants, overseas workers’ remittances to family and friends in China are still expensive (5% of the average $200 transaction: 5 times higher than the G20 target). With lower fees and faster speeds, stablecoins are expected to hold a significant share of the remittance market of about $1 trillion. If the promised immediacy and significantly reduced costs are achieved, stablecoins may occupy 10% to 20% of the market share under high adoption rates.

-

Institutional Trading and Capital Markets : Use cases for stablecoins to be professional investors or tokenized securities settlement transactions are expanding. Large amounts of capital flows (foreign exchange, securities settlement) can start using stablecoins to accelerate settlement. Stablecoins can also simplify the financing process for retail purchases of stocks and bonds, which is currently usually achieved through batch automatic clearing house processing. Large asset management companies have begun to pilot stablecoin settlement for funds, laying the foundation for their widespread use in the capital market. Given the huge payment flows among financial institutions, even modest adoption may account for about 10% to 15% of the stablecoin market.

-

Interbank liquidity and capital: Banks and financial institutions that use stablecoins in internal or interbank settlements account for a small proportion, but may have a huge impact (maybe less than 10% of the total market size). Leading industry player JP Morgan has launched a blockchain project with more than $1 billion in daily transactions, which shows great potential despite the lack of transparency in regulation. This area is likely to grow significantly, although it may overlap with the institutional uses mentioned above.

2.5 Stablecoins: Bank card, central bank digital currency (CBDC) and

strategic autonomy

We believe that stablecoin usage may grow and these new opportunities will create space for new entrants. The current duopoly pattern of issuers may continue in the offshore market, but the onshore market in each country may provide new players with a platform to join.

正如过去10~15年银行卡市场的演变一样,稳定币市场也将发生变化。 Stablecoins have some similarities with the bank card industry or cross-border banking business.所有这些行业都具有强大的网络/平台效应和强大的强化循环。更多商家接受某个值得信赖的品牌(Visa、Mastercard 等),会吸引更多持卡人使用该卡。稳定币也具有类似的使用循环。

在较大的司法管辖区,稳定币通常不受金融监管,但这种情况在欧盟(MICA,2024)和美国(正在进行)正在发生变化。更严格的金融监管需求,以及对合作伙伴的高成本要求,可能会导致稳定币发行商的集中化,就像我们在信用卡网络中看到的那样。

最终,拥有少数几家精选的稳定币发行商对更广泛的生态系统有利。

虽然一两家主要参与者可能看起来很集中,但过多的稳定币会导致碎片化、不可替代的货币形态 。稳定币只有在具备规模和流动性的情况下才能蓬勃发展。

Raj Dhamodharan,Executive Vice President, Blockchain & Digital Assets, Mastercard

然而,政治和技术的不断发展,导致信用卡市场(尤其是在美国以外的地区)的差异性加剧。同样的情况会不会也发生在稳定币上?

许多国家已经开发了自己的国家卡计划,例如巴西的Elo(2011年)、印度的RuPay(2012年)等等。许多国家卡计划的推出是出于国家主权的考虑,并受到当地监管变化和国内金融机构政治鼓励的推动。它们还实现了与新的国家实时支付系统的整合,例如巴西的Pix 和印度的UPI。国际卡计划虽然近年来持续增长,但在许多非美国市场失去了市场份额。在许多市场,技术变革导致了数字钱包、账户到账户支付和超级应用的兴起。所有这些都导致了信用卡市场份额的下降。

正如我们在信用卡市场看到国家级计划的激增一样,我们很可能会看到美国以外的司法管辖区继续专注于开发自己的中央银行数字货币(CBDC),将其作为国家战略自主的工具,尤其是在批发和企业支付领域。

OMFIF 对34 家央行的调查显示,75% 的央行仍计划发行CBDC。预计未来三到五年内发行CBDC 的受访者比例已从2023 年的26% 增长到2024 年的34%。与此同时,一些实际实施问题也日益凸显——31% 的央行推迟了发行时间表,理由是立法和希望探索更广泛的解决方案。

CBDC 项目始于2014年,当时中国人民银行(PBoC)开始研究数字人民币。巧合的是,Tether 也诞生于这一年。近年来,在私人市场力量的推动下,稳定币发展迅速。

相比之下,CBDC 在很大程度上仍处于官方试点阶段。少数几个启动了国家级CBDC 项目的小型经济体,并没有看到太多的自然用户增长。然而,近期地缘政治紧张局势的加剧,可能会增加人们对CBDC 项目的兴趣。

2.6 稳定币与银行:机遇与风险

稳定币和数字资产的采用为一些银行和金融机构提供了新的业务机会,以推动收入增长:

银行在稳定币生态系统中的作用

银行有很多机会参与稳定币的开发,继续充当货币流动的枢纽。这可以是直接作为稳定币发行人,也可以是作为支付收付/支付解决方案的一部分,围绕稳定币的结构化产品,一般的流动性提供,或以更间接的方式发挥作用。

随着用户追求更具吸引力的产品和更佳的体验,我们已经看到存款从银行体系中流出。借助稳定币技术,银行有机会创造更好的产品和体验,同时将存款保留在银行体系中——用户通常更希望存款在银行体系中得到安全保障。

Matt Blumenfeld,Global and US Digital Assets Lead, PwC

在系统层面,稳定币可能产生与“狭义银行”类似的影响,而且关于此类机构的优缺点,政策争论由来已久。 The transfer of bank deposits to stablecoins may affect banks' ability to lend.这种放贷能力的下降可能会抑制经济增长,至少在系统调整的过渡期内是如此。

正如国际货币基金组织2001 年第9 号论文所总结的那样,出于对信贷创造和增长的担忧,传统的经济政策反对狭义银行业务。卡托研究所2023 年报告及其他类似机构也提出了反对意见,他们认为“狭义银行业务”可以降低系统性风险,而信贷和其他流动则会适应。

三、公共部门对于区块链的看法

信任和透明度是区块链在公共部门的核心优势。区块链具有巨大的潜力,可以取代现有的中心化系统,从而提高运营效率、增强数据保护并减少欺诈。

虽然公共部门的链上交易量最初可能小于私营部门,但公共部门日益增长的兴趣对于区块链的普遍应用至关重要。

3.1 公共支出与财政

区块链技术有望通过提高透明度、效率和问责制来改变政府服务的公共支出和财政,同时显著减少对手动和纸质流程的依赖。通过整合政府机构和外部合作伙伴之间的财务和非财务报告, 区块链能够实时追踪支出 。

这应该能够降低腐败风险,同时增强公众对公共机构的信任。区块链记录的不可篡改特性确保交易的可追溯性和可验证性,从而简化审计流程并加强问责制。区块链还能实时监控财政拨款,并提供数据驱动的洞察,以评估公共支出的影响。

智能合约的使用 可以通过自动化投标、评估和合同授予流程,提高招标流程的效率。这减少了人工干预,提高了合同授予的透明度,从而解决了人工选择中常见的偏见和偏袒问题。合同付款也可以按里程碑分阶段进行,确保仅在项目里程碑达成时才发放资金。

通过将区块链集成到会计系统中,可以简化税收征管和合规流程,实现税务计算的自动化并向政府汇款。由于所有交易都永久记录在区块链上,逃税变得更加困难,从而加强了税收征管。

基于区块链的数字债券还可以通过自动支付利息,实现更快、更透明地发行。它还允许部分所有权,从而扩大投资者的参与度。在债券期限内实时跟踪债务工具,可以进一步提高问责制和投资者信心。

除了提高效率和问责制之外,基于区块链的政府服务数字化还可以减少每年用于合同、记录和交易的大量纸质文件。例如,迪拜的“无纸化战略”旨在通过将所有服务(包括签证申请、账单支付和执照续期)数字化,减少每年产生的数十亿张纸张,这些服务现在将通过区块链技术安全地进行交易。

3.2 公共部门资金和拨款的发放

传统的政府和公共部门资金和拨款发放流程通常涉及大量人工工作——处理表格、验证索赔以及管理现金流。区块链提供了一种更有效的替代方案,可以简化流程,增强数据安全性和完整性。使用区块链还可以提高透明度,确保资金公平分配,减少腐败和欺诈的机会。区块链还可以降低运营成本,提高记录保存和对账的效率。

加密散列数据被整合到区块链系统中,以增强交易信息的完整性并避免未经授权的访问。智能合约还可以通过编程预先定义的条件(例如验证资格标准)来自动化和保护分配流程。

区块链技术在很多方面都非常适合跨境使用,世界银行于2024 年9 月启动的“资金链”倡议就是一个很好的例子。该倡议目前已在摩尔多瓦、菲律宾、肯尼亚、孟加拉国、毛里求斯和莫桑比克开展了9 个项目。

FundsChain——世界银行用于资金拨付追踪的区块链

世界银行负责每年拨付数十亿美元的资金,并确保资金用于其预期用途。由于在多个国家开展了众多项目,追踪和核实资金使用情况传统上是一个耗时的手动过程。虽然一些任务已经实现自动化,但大部分监管工作仍然需要大量劳动力。FundsChain 计划旨在提高资金分配流程的透明度和效率。

世界银行与安永合作开发了一个基于区块链的平台,旨在实时追踪资金流向和支出情况。FundsChain 提供强大的资金拨付追踪功能,使利益相关者能够实时查看资金,提高透明度并增强信心,确保资金真正到达预期受益人手中,最终使世界银行能够支持借款国的反腐败改革议程。

代币在资金入账时生成。这些代币会被记入每个实体的数字钱包。通过智能合约实现交易自动化,效率得以提升;通过在区块链上存储和公证上传的资源,安全性和数据完整性也得到进一步增强。共识算法用于验证交易并防止超支。

目前,这种监督是通过合同要求借款人提交支出报告并收集其他支持文件来实现的。这可能是一个高度手动、劳动密集且耗时的过程,需要大量的协调工作、时间和成本。通过FundsChain,所有项目利益相关者(包括借款人、供应商、审计师和最终受益人)都可以看到资金的去向、使用方式和时间,从而实现端到端的透明度,所有交易均记录在链上,使利益相关者能够实时监控资金流向。

世界银行使用私有区块链构建FundsChain,是因为他们希望掌控该平台及其未来的发展。鉴于其公共部门使命的敏感性,他们不希望依赖第三方供应商。他们还希望确保其使用的任何平台都能与其他多边开发银行的平台互操作,从而实现无缝集成。

3.3 公共记录管理

区块链技术为公共记录管理提供了一个强大而安全的平台,确保关键数据的真实性、完整性和可访问性。通过利用不可篡改的账本,区块链可以保持记录的完整性、准确性和防篡改性,从而增强公众对政府系统的信任。

与集中存储记录的传统数据库不同,区块链上的数据分布在多个节点的网络中,即使单个节点发生故障,数据仍然可访问,并降低了网络攻击导致数据泄露的风险。对记录的任何修改都会被加密并记录时间戳,从而创建可审计的线索,在保护公民数据的同时增强问责制。区块链还提高了记录的可访问性和可用性,因为记录可以在需要时轻松检索和访问。

各国政府正在探索用于公共记录管理的区块链解决方案。例如,新加坡的OpenCerts是一个区块链平台,它使教育机构能够颁发和验证防篡改的学历证书。这有助于降低文件伪造的风险,并简化凭证验证。

区块链可以推动显著改进的另一个领域是土地所有权和房地产管理。该领域往往受到记录保存碎片化、流程过时和腐败的困扰。在公共部门腐败猖獗的国家,欺诈风险尤其高。例如,格鲁吉亚已将其土地所有权登记系统整合到比特币区块链中,改进了房地产相关交易的验证,同时提高了安全性和服务效率。

在机构诚信薄弱的国家,有机会通过去中心化的账本来提高透明度,并恢复公众对公共机构的信任。这些账本可审计、对公众透明,并由各方维护,且各方有不串通的动机。

Artem Korenyuk,Digital Assets – Client, Citi

3.4 人道主义援助

在危机期间,有效的协调至关重要,因为多个实体使用不同的系统提供食品、医疗保健和住所方面的援助。区块链可以通过提供统一的共享账本来简化项目设计、资源分配和数据共享,从而避免重复工作并确保援助能够送达最需要的人。实时、可验证的交易记录还能促进援助机构、政府和非政府组织之间的合作,从而缩短整体响应时间。

除了协调之外,区块链还有潜力重塑危机众筹,提供一个透明且去中心化的资金调动机制。通过利用数字货币,区块链可以收集捐款并将其直接转移到经过验证的受益人,无需中介机构,从而降低成本并减少延误。智能合约的使用可以进一步实现基于预定条件的资金支付自动化。

确保人道主义供应链的完整性是区块链可能帮助解决的另一个关键挑战。通过实现端到端可追溯性,区块链使援助机构能够追踪人道主义物资的来源、流动和使用情况。这打破了数据孤岛,防止了腐败,并确保援助物资有效地送达受灾社区。它还能实现实时库存跟踪,帮助各组织更快地应对物资短缺,并避免出现物流瓶颈。

联合国难民署(UNHCR) 使用Stellar 区块链分发人道主义援助,这是区块链在公共部门影响的一个引人注目的例子。UNHCR 实施区块链技术来简化财政援助的发放流程,并成功地将其应用于乌克兰、阿根廷和世界其他地区。区块链的一个关键优势是通过整体数字化转型工作显著节省了成本。

区块链还带来了更高的透明度。在许多危机情况下,流离失所者可能无法获得传统的银行服务。通过使用基于区块链的钱包,援助受助人无需依赖第三方即可接收和使用资金。

Denelle Dixon, CEO and Executive Director, Stellar Development Foundation

3.5 资产代币化

代币化有望通过代币以数字化方式代表现实世界和金融资产,从而释放价值,提高效率、透明度和可及性。在公共部门,代币化可应用于金融资产和实物资产。

政府可以对债务工具进行代币化,提高债券发行效率,并让更广泛的投资者能够参与其中。同样,自然资源和基础设施资产(例如道路、桥梁和公用事业)也可以以数字代币的形式呈现,从而实现更高效地追踪、管理和融资。

除了投资可及性和部分所有权模式之外,代币化还能帮助金融机构和公共机构简化运营,降低效率低下和系统性风险。通过智能合约实现的自动化可以最大限度地减少中介机构,提高流动性,并增强公众对公共资产管理的信任。

一些机构已经探索了区块链在数字债券中的应用。例如,欧洲投资银行(EIB) 于2021 年发行了其首笔基于区块链的数字债券,金额为1 亿欧元。此次发行与法国银行合作,使用区块链进行数字债券的登记和结算。

2022 年,欧洲投资银行启动了Venus 项目,使用央行货币以批发型CBDC 的形式在私有区块链上发行了其首笔以欧元计价的数字债券。同样,瑞士卢加诺市在2023-24 年间,利用瑞士国家银行的批发型CBDC,利用分布式账本技术(DLT)/区块链技术完成了三笔债券发行。

Promissa – 代币化本票

许多国际金融机构,包括多边开发银行(MDB),其资金部分来源于被称为本票的金融工具,其中大多数仍以纸质形式存在。虽然现行系统框架为成员国向世界银行等公共机构缴纳认购款和会费提供了操作控制,但未偿付本票的托管可以数字化,以应对运营挑战并进一步提高效率。

Promissa 项目由国际清算银行创新中心、瑞士国家银行和世界银行共同发起,旨在构建一个数字代币化本票的原型平台。Promissa 项目探索使用分布式账本技术(DLT) 简化本票管理,并在本票的整个生命周期内为所有交易对手提供单一真实信息来源。这将使成员国央行能够全面了解其与多边开发银行的未偿票据,反之亦然。

多边开发银行间的本票数量巨大:例如,世界银行最大的两家机构——国际复兴开发银行(IBRD)和国际开发协会(IDA),自成立以来都拥有大量成员国承诺的本票。虽然Project Promissa项目旨在重新构想一个“单一事实来源”平台解决方案,以简化成员国与多边开发银行之间本票的管理,但未来可以通过整合代币化或现有的支付系统,将其扩展到与此类本票相关的支付。

3.6 数字身份

单一的数字身份可以作为公共和私人交易的有效证明,增强存储安全性和便捷性。基于区块链的数字身份(ID) 提供了一种去中心化、防篡改的身份验证机制,从而降低了欺诈和身份盗窃的风险。

数字身份将基本服务扩展到服务匮乏的社区和那些没有官方证件的人群,例如流离失所者。由于近8.5 亿人缺乏官方身份证明,数字身份证可以通过使用生物识别和社区验证等替代数据赋予个人权力。

区块链的不可篡改特性为每笔交易创建了透明的记录,创建了可验证的数字审计线索,从而增强了安全性和问责制。其去中心化的架构和强大的加密协议可以保护个人数据免遭泄露和欺诈。

此外,自主主权身份确保个人拥有对其信息的所有权和控制权,并根据需要选择性地共享数据。零知识证明等先进技术能够在不泄露敏感信息的情况下验证身份属性。

瑞士楚格市就是一个早期的例子,该市基于以太坊区块链的自主数字身份证,为居民提供单一、可验证的电子身份,适用于各种应用。楚格市的区块链数字身份项目于2017年启动,由于复杂性和可用性有限等一系列因素,迄今为止应用有限。

2023年,巴西推出了基于区块链的新国民身份证。新的数字身份证可以通过移动设备使用面部识别和二维码访问。这些身份证存储在名为b-Cadastros的私有区块链上,由巴西国有IT服务公司构建,旨在提高公共机构之间数据共享的安全性和可靠性。

3.7 公共部门区块链应用面临的挑战

区块链为政府服务带来巨大潜力,带来诸多优势,例如透明度、安全性和效率。然而,区块链的大规模应用也面临着以下所述的重大挑战。

制定标准化协议和实践将有助于公共区块链在银行和政府中获得更广泛的认可和信任。促进公共部门和私营部门之间的合作可以推动创新,并确保区块链解决方案满足所有利益相关者的需求。

Ricardo Correia,Partner, Bain & Company

-

缺乏信任 :许多区块链解决方案仍处于实验阶段,未经测试,这使得在生态系统中建立信任变得困难。有必要提高整个生态系统的认知度并培养相关技能。这需要时间和投资。

-

互操作性和可扩展性 :如果要在国家或全球范围内采用区块链解决方案,它们需要具备互操作性和可扩展性,以处理大量交易。目前正在努力制定区块链的全球标准,使其在不同市场获得广泛认可。

-

转型挑战 :彻底改造现有基础设施可能极具挑战性,需要投入大量的时间和资源。实际收益证据不足、区块链技术被认为不成熟以及复杂的遗留系统的存在进一步阻碍了新的投资。

-

监管问题 :区块链的去中心化特性给大规模应用带来了挑战,因此需要建立监管框架,以认可区块链的法律性质、存储文档的有效性以及发行的金融工具。监管不明确减缓了区块链的采用。

-

应对滥用风险 :虽然难以量化非法使用的加密货币规模,但据估计,2024 年非法地址接收了510 亿美元的加密货币,比上一年增长了11%。然而,作为所有链上交易量的百分比,这个数字通常不到1%。

变革阻力与公众认知

实施区块链通常意味着对现有系统的彻底改革,这可能会改变公职人员工作的方方面面,包括他们的日常工作。虽然有些人可能将区块链视为改善行政流程的积极变革,但许多人往往会抵制它,因为他们认为区块链是一种威胁。

公众认知也起着至关重要的作用。区块链有时会与投机性的加密货币市场和模因币联系在一起,掩盖了其底层技术在现实世界中的优势。这可能会加剧人们的怀疑,从而减缓其在公共部门的主流应用。

Saqr Ereiqat, Secretary General, Dubai Digital Asset Association

四、附录

4.1 稳定币监管:GENIUS Act 与STABLE Act

本节重点介绍美国国会目前正在审议的两项主要稳定币立法。这两项立法都旨在建立一个监管框架,将稳定币纳入主流金融生态系统。

《引导和建立美国稳定币国家创新法案》(GENIUS Act)提出了一种双管齐下的监管方法,根据稳定币发行人的市值水平进行监管。

总市值低于100 亿美元的稳定币发行人可以选择接受州级监管机构的监管(如果州级监管制度与联邦监管框架基本相似)。市值超过100 亿美元门槛的发行人将接受联邦监管。银行和非银行机构均可在获得监管机构批准的情况下发行稳定币。

该法案概述了发行人的义务,包括1:1 储备支持、披露和赎回程序、每月储备构成报告和证明、审慎标准以及一系列消费者保护措施。

第二项立法是《2025 年稳定币透明度和问责制促进更佳账本经济法案》(STABLE Act)。该法案在允许发行稳定币的公司类型方面与《GENIUS 法案》有很多相似之处,并且对发行人维持1:1 储备的要求类似(但在储备构成方面有所不同),在信息披露、每月证明等方面也有类似的要求。与《GENIUS 法案》不同,该法案不以100 亿美元的市场门槛来区分发行人。

鉴于这些法案将赋予某些稳定币发行人选择加入州级监管制度的能力,它们可能会造成监管套利风险,即一些州可能会引入不太严格的制度来吸引稳定币发行人。州级监管制度的差异可能会使银行难以与受多种不同监管制度约束的发行人开展业务。

虽然这两项法案都为银行提供稳定币支付服务打开了大门,包括提供托管服务、私钥或支付稳定币的储备支持,但确保立法提供适当的非法融资保护措施,将是使银行能够充分利用此类机会的关键。

这两项法案都将在颁布之日起18 个月后(具体日期待定)或联邦银行监管机构发布最终实施条例之日起120 天后生效,以较早者为准。这两项法案都必须经过协调程序,由众议院和参议院全体就同一版本的立法进行投票,然后才能通过成为法律。在此过程中,法案仍有可能在实质内容上发生修改。

4.2 公有链vs. 私有链

在探索基于区块链的基础设施时,必须权衡私有链和公有链之间的利弊。公有链是无需许可的网络,允许任何人参与、验证交易和访问数据。这种开放性使其成为实现可访问性和透明度的强大工具,但也在监管执行和可扩展性等领域带来了挑战。

这与公有云计算和托管的现状类似。银行和金融机构监管机构曾担心存储在公有云中的数据的安全性和控制权。这次,人们对公有链也抱有类似的担忧。银行需要采取适当的控制措施和风险缓解措施,制定规则手册,并就此进行相关教育。

Biser Dimitrov, Digital Assets – Technology, Citi

-

去中心化且不受任何权威约束:公有链往往独立于任何单一实体运行,从而降低了政府过度干预、审查或单方面操纵的风险。治理通常是去中心化的,通过工作量证明(PoW) 或权益证明(PoS) 等共识机制实现。

-

透明度和可审计性:公有链确保交易被永久记录并公开访问。这种透明度增强了问责制,减少了腐败,并有助于增强对金融体系的信任。

-

互操作性和开放可访问性:在公有链上发行的稳定币可用于多种应用程序和服务,无需进行自定义集成。它们还促进了全球可访问性,任何有互联网连接的人都可以访问和使用它们。

-

安全性和弹性:公有链的去中心化特性,由庞大的节点网络和加密机制保护,使其与私有系统相比,更能抵御单点故障、网络攻击和中心化攻击。

另一方面,公有链可能并不适合所有用例:

-

可扩展性和交易吞吐量:公有链可能在交易吞吐量方面存在困难,尤其是在处理大量交易时,这会导致交易处理速度变慢且费用更高。这使得它们不太适合处理大容量、实时的金融交易。

-

缺乏隐私和匿名性:由于所有交易都是公开可见的,公有链可能并非处理敏感金融或其他政府数据的理想选择。匿名性可能因区块链的类型而异。

-

监管合规挑战:公有链的匿名性使得反洗钱(AML) 和“了解你的客户”(KYC) 法规的执行变得困难。政府可能难以追踪非法金融活动或有效执行金融政策。

-

定制化程度有限:虽然在公链上发行的稳定币提供了成熟的框架,但它们在针对特定用例定制解决方案方面灵活性有限。

政策制定者和风险管理者可能还需要考虑其他问题:(1) 正常运行时间和可靠性,以及(2) 在与公链相关的代币中识别出最可信的代币。对一些人来说,这与人们对加密货币的负面看法有关(因为它最初与非法活动联系在一起)。

无论是私营还是公共部门,银行和大型机构传统上都依赖于专有的内部部署技术。开源和云技术需要时间才能渗透到这些机构中。公链、无需许可的区块链的整合将是一个挑战——但在监管和政策变革的支持下,变革正在进行中。

panewslab

panewslab