Circle IPO Interpretation: Growth Potential Behind Low Net Profit Rate

Reprinted from panewslab

04/17/2025·13DAuthor: @BlazingKevin_, Movemaker Researcher

In the stage of accelerating clearance of an industry, Circle's choice to go public is hidden behind a seemingly contradictory but imaginative story - net profit margin continues to decline, but still contains huge growth potential. On the one hand, it has high transparency, strong regulatory compliance and stable reserve revenue; on the other hand, its profitability is surprisingly "moderate" - the net profit margin in 2024 is only 9.3%. This apparent "inefficiency" is not due to the failure of the business model, but rather reveals a deeper growth logic: Against the backdrop of the gradual decline of high interest rate dividends and the complex distribution cost structure, Circle is building a highly scalable, compliance-oriented stablecoin infrastructure, and its profits are strategically "reinvested" in market share improvement and regulatory chips. This article will take Circle's seven-year listing path as a clue, from corporate governance, business structure to profit model, and deeply analyze its growth potential and capitalization logic behind "low net profit margin".

1 Seven-year long-term run on the market: a history of the evolution of

crypto-regulation

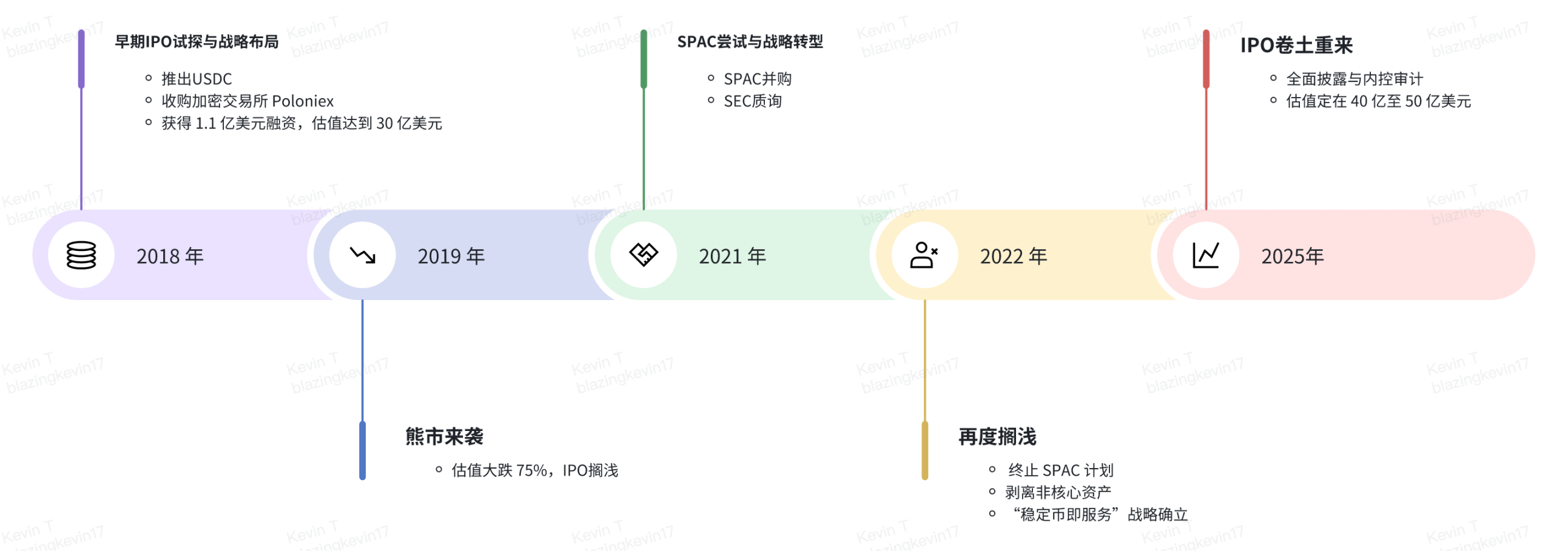

1.1 Paradigm migration of three capitalization attempts (2018-2025)

Circle's journey to list can be regarded as a living specimen for dynamic game between crypto companies and regulatory frameworks. The first IPO test in 2018 is a time when the US Securities and Exchange Commission (SEC) has a fuzzy period for the identification of cryptocurrency attributes. At that time, the company formed a dual-wheel drive of "payment + trading" by acquiring the Poloniex exchange, and received US$110 million in financing from Bitmain, IDG Capital, Breyer Capital and other institutions. However, regulators' doubts about the compliance of the exchange's business and the sudden bear market shock caused the valuation to plummet 75% from US$3 billion to US$750 million, revealing the fragility of the early crypto-enterprise business model.

The 2021 SPAC attempt maps the limitations of regulatory arbitrage thinking. Although the merger with Concord Acquisition Corp circumvents strict scrutiny of traditional IPOs, the SEC's inquiry on stablecoin accounting treatment hits the nail on the head — requiring Circle to prove that USDC should not be classified as a securities. This regulatory challenge led to a miscarriage of transactions, but unexpectedly drove the company to complete a key transformation: divesting non-core assets (such as Poloniex sold to investment groups for $150 million), establishing the strategic main axis of "stablecoin as a service". From now until today, Circle has fully invested in the construction of USDC compliance and has actively applied for regulatory licenses in many countries around the world.

The 2025 IPO choice marks the maturity of the capitalization path of crypto enterprises. Listing on the New York Stock Exchange not only needs to meet the full disclosure requirements of Regulation SK, but also needs to undergo internal control audits under the Sarbanes-Oxley Act. It is worth noting that the S-1 document disclosed in detail the reserve fund management mechanism for the first time: of the approximately US$32 billion assets, 85% were allocated through BlackRock's Circle Reserve Fund in the overnight reverse repurchase agreement, and 15% were deposited in systemic important financial institutions such as Bank of New York Mellon. This transparent operation essentially builds an equivalent regulatory framework with traditional money market funds.

**1.2 Cooperation with Coinbase: From ecological co-construction to

subtle relationships**

As early as the launch of USDC, the two teamed up to cooperate through the Centre Alliance. When the Centre Alliance was established in 2018, Coinbase held 50% of the equity and quickly opened up the market through the "technical output exchange traffic entrance". According to Circle's 2023 IPO filing, it acquired the remaining 50% stake in Centre Consortium from Coinbase for $210 million in shares, and a re-arrangement has also been made on the share sharing agreement of USDC.

The current share agreement is a clause for dynamic game. According to S-1 disclosure, the two are divided into a certain proportion based on USDC reserve income (the article mentions that Coinbase shares about 50% of reserve income), and the share ratio is related to the amount of USDC supplied by Coinbase. From Coinbase’s public data, it can be seen that the platform holds about 20% of the total USDC circulation in 2024. Coinbase took away about 55% of its reserve revenue with a 20% supply share, placing some hidden dangers for Circle: When USDC expands outside the Coinbase ecosystem, marginal costs will rise nonlinearly.

2 USDC reserve management and equity and holding structure

2.1 Layered reserve management

USDC's reserve management shows obvious "liquidity stratification" characteristics:

- Cash (15%): deposited in New York Mellon and other GSIBs to deal with sudden redemption

- Reserve Fund (85%): Circle Reserve Fund configuration managed by BlackRock

Starting from 2023, USDC reserves are limited to cash balances in bank accounts and Circle reserve funds, and their asset portfolio mainly includes US Treasury securities and overnight US Treasury repurchase agreements with a remaining maturity of no more than three months. The weighted average maturity date of the asset portfolio shall not exceed 60 days, and the weighted average maturity period of the US dollar shall not exceed 120 days.

2.2 Equity classification and stratified governance

According to the S-1 file submitted to the SEC, Circle will adopt a three-tier equity structure after its listing:

- Class A shares: Common shares issued during the IPO process have one vote per share;

- Class B shares: held by co-founders Jeremy Allaire and Patrick Sean Neville, with five votes per share, but the total voting rights limit is 30%, which ensures that the core founding team still has the decision-making leadership even after the company goes public;

- Class C shares: No voting rights, can be converted under certain conditions to ensure that the corporate governance structure complies with the New York Stock Exchange rules.

The equity structure is designed to balance the stability of open market financing with the long-term corporate strategy, while ensuring the executive team’s control over key decisions.

2.3 Distribution of shareholdings of executives and institutions

The S-1 document discloses that the executive team owns a large number of shares, while several well-known venture capital and institutional investors (such as General Catalyst, IDG Capital, Breyer Capital, Accel, Oak Investment Partners and Fidelity) all hold more than 5% of the shares, and these institutions hold more than 130 million shares in total. A valuation of 5 billion IPOs can bring significant returns to them.

3 Profit model and profit disassembly

3.1 Revenue model and operational indicators

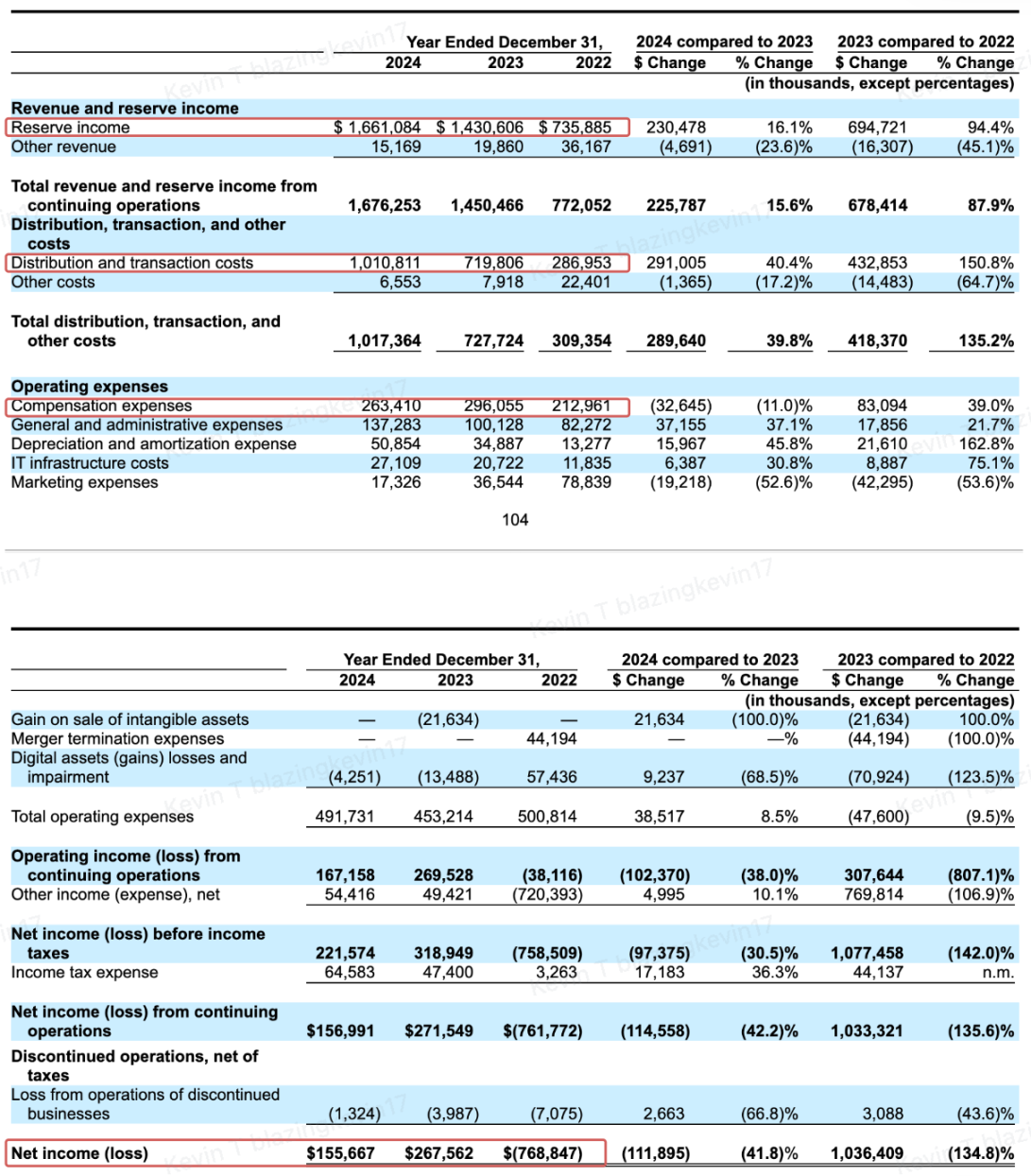

- Source of income: Reserve income is Circle's core income source. Each token of USDC is backed by equal amounts of USD. The reserve assets invested mainly include short-term US Treasury bonds and repurchase agreements, and obtain stable interest income under high interest cycles. According to S-1 data, total revenue in 2024 reached US$1.68 billion, of which 99% (about US$1.661 billion) came from reserve revenue.

- Share with partners: The cooperation agreement with Coinbase stipulates that Coinbase receives 50% of reserve revenue based on the amount of USDC held, resulting in a relatively low revenue actually owned by Circle, which lowers its net profit performance. Although this share ratio has dragged down profits, it is also a necessary price for Circle and its partners to build an ecosystem and promote the widespread use of USDC.

- Other income: In addition to reserve interest, Circle also increased revenue through enterprise services, USDC Mint business, cross-chain handling fees, etc., but contributed less, with only US$15.16 million.

**3.2 The paradox between revenue growth and profit shrinkage

(2022-2024)**

There are structural motives behind surface contradictions:

- Converging from multiple to single core: From 2022 to 2024, Circle's total revenue increased from US$772 million to US$1.676 billion, with an annual compound growth rate of 47.5%. Among them, reserve revenue has become the company's core source of income, with revenue accounting rising from 95.3% in 2022 to 99.1% in 2024. This increase in concentration reflects the successful implementation of its "stablecoin-as-a-service" strategy, but it also means that the company's reliance on changes in macro interest rates has increased significantly.

- Distribution spending surges to compress gross profit margins: Circle's distribution and transaction costs have risen sharply in three years, jumping from US$287 million in 2022 to US$1.01 billion in 2024, an increase of up to 253%. This type of cost is mainly used for USDC's issuance, redemption and payment clearance settlement system expenditure. As USDC's circulation expands, this expenditure increases rigidly.

- As such costs cannot be significantly compressed, Circle's gross profit margin quickly fell from 62.8% in 2022 to 39.7% in 2024. This reflects that although its ToB stablecoin model has scale advantages, it will face systemic risks of profit compression during the interest rate down cycle.

- Profits turned losses into profits but slowed marginally: Circle officially turned losses into profits in 2023, with net profit reaching US$268 million and a net profit margin of 18.45%. Although the profit trend continued in 2024, after deducting operating costs and taxes, the disposable income was only US$101,251,000. After adding 54,416,000 non-operating income, the net profit was US$155 million, but the net profit margin has declined to 9.28%, a year-on-year decrease of about half.

- Cost rigidization: It is worth noting that the company's investment in general administrative expenditure (General & Administrative) in 2024 was as high as US$137 million, a year-on-year increase of 37.1%, and has increased for three consecutive years. Combined with its S-1 disclosure information, this expenditure is mainly used for license application, auditing, legal compliance team expansion, etc. around the world, which confirms the cost rigidity brought by its "compliance priority" strategy.

Overall, Circle completely got rid of the "exchange narrative" in 2022, achieved a profit turning point in 2023, and successfully maintained profits in 2024 but the growth rate slowed down. Its financial structure has gradually moved closer to traditional financial institutions.

However, its high reliance on revenue structure of US Treasury spreads and transaction scale also means that once the interest rate downward cycle or the USDC growth slows down, it will directly impact its profit performance. In the future, if Circle wants to maintain sustainable profits, it needs to seek a more stable balance between "reducing costs" and "expanding incremental growth".

The deep contradiction lies in the shortcomings of the business model: when USDC is an "cross-chain asset" enhances its attributes (on-chain transaction volume of US$20 trillion in 2024), its currency multiplier effect will actually weaken the issuer's profitability. This is similar to the dilemma of traditional banking.

3.3 Growth potential behind low net profit margins

Although Circle's net profit margin continues to be under pressure due to high distribution costs and compliance expenditures (net profit margin in 2024 was only 9.3%, down 42% year-on-year), multiple growth momentums are still hidden in its business model and financial data.

The continuous increase in circulation volume drives steady growth in reserve revenue:

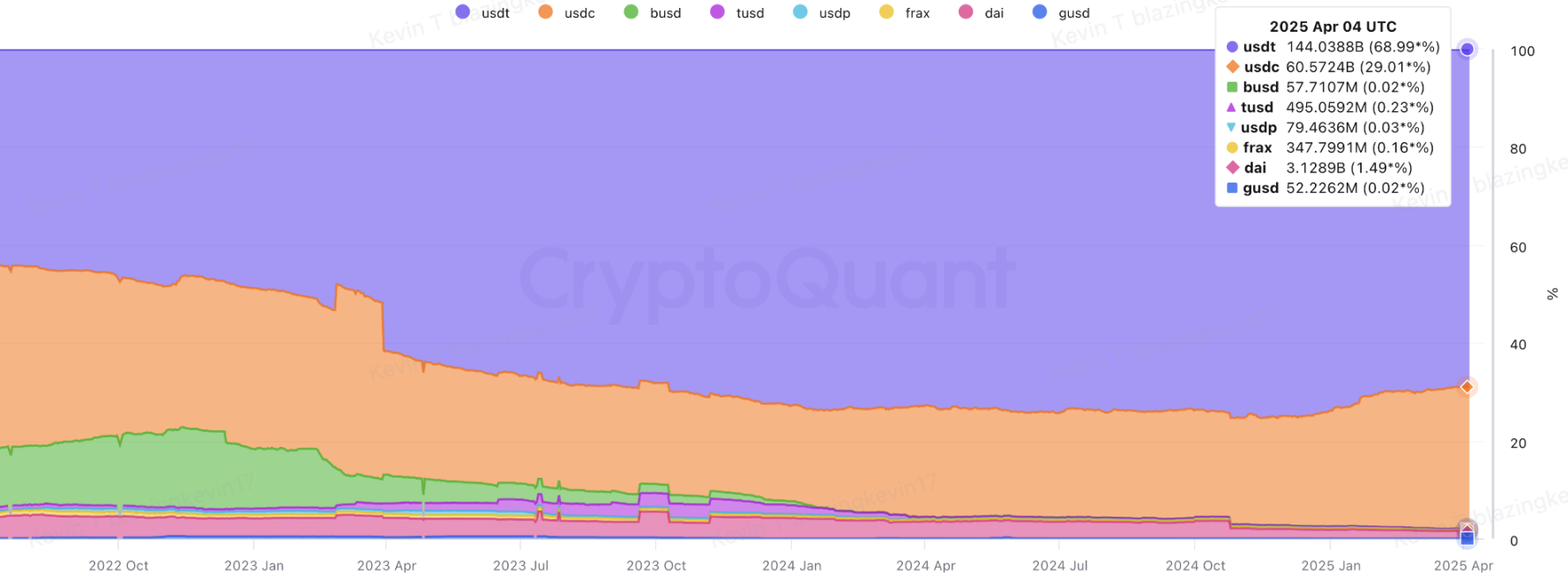

According to CryptoQuant, as of early April 2025, USDC's market value exceeded US$60 billion, second only to USDT's US$144.4 billion; by the end of 2024, USDC's market share had increased to 26%. On the other hand, USDC's market capitalization growth remained strong in 2025. USDC's market value has increased by US$16 billion in 2025. Considering that its market capitalization was less than US$1 billion in 2020, the compound annual growth rate (CAGR) from 2020 to April 2025 has reached 89.7%. Even if USDC growth slows for the remaining eight months, its market value is expected to reach US$90 billion by the end of the year, and the CAGR will rise to 160.5%. Although reserve income is highly sensitive to interest rates, low interest rates may stimulate USDC demand, and strong scale expansion can partially offset the risk of downside rates.

Structural optimization of distribution costs: Although the high share payment is paid to Coinbase in 2024, this cost is nonlinear with the growth of circulation. For example, the partnership with Binance paid only $60.25 million in one-time fees, which drove its platform's USDC supply from $1 billion to $4 billion, with a unit customer acquisition cost significantly lower than Coinbase. Combined with the S-1 file, Cirlce’s cooperation plan with Binance can expect Cirlce to achieve market capitalization growth at a lower cost.

Conservative valuation unpriced market scarcity: Circle's IPO valuation is between US$4-5 billion, based on adjusted net profit of US$200 million, with P/E between 20 and 25x. It is similar to traditional payment companies such as PayPal (19x) and Square (22x), which seems to reflect the market's positioning of "low growth and stable profitability", but this valuation system has not yet fully priced its scarcity value as the only pure stablecoin target for the US stock market. The only target for the sub-track usually enjoys a valuation premium, which Circle did not calculate in it. At the same time, if the stablecoin-related bill is successfully implemented, offshore issuers need to significantly adjust their reserve structure, and the existing compliance structure can be directly translated to form a "regulatory arbitrage end dividend." Corresponding policy changes can bring significant market share improvements to USDC.

The market value trend of stablecoins is resilient compared to Bitcoin: the market value of stablecoins can remain relatively stable when the price of Bitcoin falls sharply, demonstrating its unique advantage in crypto market fluctuations. As the market enters a bear market stage, investors often seek safe-haven assets and the stability of the growth of stablecoins' market value, making Circle a "safe haven" for funds. Compared with companies such as Coinbase and MicroStrategy that rely heavily on market conditions, Circle, as the main issuer of USDC, relies more on the trading volume of stablecoins and the interest income of reserve assets, rather than directly affected by crypto asset price fluctuations. Therefore, Circle has stronger risk resistance and higher profit stability in bear markets. This makes Circle likely to play a hedging role in the portfolio, providing investors with a certain protection umbrella, especially when the market fluctuates violently.

4 Risks - Stable Coin Market Scale

4.1 The network of institutions is no longer a solid moat

- The double-edged sword of interest binding: Although Coinbase splits 55% of reserve revenue, its share of USDC is only 20%. This asymmetric share stems from the legacy agreement of the Centre Alliance in 2018, which in disguise led to the cost of Circle paying $0.55 for every $1 new revenue added, significantly higher than the industry average.

- Ecological lock-in risk: The advance payment agreement signed with Binance exposes imbalance in control of the channel. If the leading exchanges collectively request renegotiate terms, it may trigger a vicious cycle of "spike up distribution costs."

4.2 Two-way impact of the progress of the stablecoin bill

- Pressure for localization of reserve assets: The bill requires issuers to hold 100% of reserves (cash and cash equivalents) and give priority to using federal or state chartered deposit institutions in the United States as custodians, while Circle currently only 15% of cash is stored in domestic institutions such as Bank of New York Mellon. If the compliance adjustment is made, hundreds of millions of dollars in one-time fund migration costs may be incurred.

5 Thoughts and summary--the strategic window for breakers

5.1 Core advantages: Market card position in the era of compliance

- Dual Compliance Network: Circle has built a regulatory matrix covering the United States, Europe and Japan, an institutional capital that traditional companies such as PayPal are difficult to replicate. After the implementation of the "Pay Stablecoin Payment Act", its compliance costs to revenue are expected to significantly reduce, forming a structural advantage.

- Cross-border payment alternative: Through the "USDC instantaneous settlement" service launched in cooperation with Wise, it has significantly reduced the cross-border payment costs of enterprises. If a portion of the annual settlement volume of SWIFT is penetrated, it can bring considerable new circulation, completely offsetting the impact of the decline in interest rates.

- B2B Financial Infrastructure: In Stripe's e-commerce payment system, the proportion of USDC settlement has increased significantly, and its automatic fiat currency conversion protocol can greatly save foreign exchange hedging costs for enterprises. This expansion of the "embedded finance" scenario has gradually enabled USDC to gradually break away from its purely media attributes and evolve into a value store function.

**5.2 Growth Flywheel: The Game between Interest Rate Cycle and Economy

of Scale**

Emerging market currency substitution: In some areas with high inflation, USDC has accounted for a portion of the US dollar's foreign exchange transactions. If the Fed rate cut leads to accelerate the depreciation of the local currency, this "digital dollarization" process may significantly drive the growth of circulation.

Offshore USD Return Channel: By cooperating with BlackRock to explore tokenized asset-related projects, Circle is converting some offshore USD deposits into on-chain assets. The value of this "fund pipeline" is not reflected in the current valuation.

- RWA Asset Tokenization: The tokenized asset services launched after the acquisition of related technology companies have achieved initial management scale, and the annualized management fee revenue is considerable.

- Interest rate buffer period: The current federal funds rate is still at a high level. Circle needs to accelerate internationalization to push circulation to a key threshold before the expectation of interest rate cuts is fully priced, so that the scale effect can cover the downward impact of interest rates.

- Regulatory window period: Before the final implementation of the "Pay Stablecoin Act", we will use our existing compliance advantages to seize institutional customers, sign exclusive settlement agreements with many top hedge funds, and build exit barriers.

Deepening of enterprise service suite: Packaging compliance APIs and on-chain audit tools into "Web3 Financial Services Cloud", charging traditional banks for SaaS subscription fees, and opening up the second curve of non-reserve income.

Under the appearance of Circle's low net profit margin, it is essentially the "profit for scale" strategy it actively chose during the strategic expansion period. When USDC circulation exceeds US$80 billion, RWA asset management scale and cross-border payment penetration achieve breakthroughs, its valuation logic will undergo a qualitative change - from a "stable currency issuer" to a "digital dollar infrastructure operator." This requires investors to reevaluate the monopoly premium brought by their network effects from a 3-5-year cycle perspective. At the historic intersection between traditional finance and crypto economy, Circle's IPO is not only a milestone in its own development, but also a touchstone for the revaluation of the entire industry's value.

Reference article:

https://www.sec.gov/Archives/edgar/data/1876042/000119312525070481/d737521ds1.htm#rom737521_10 https://www.bloomberg.com/opinion/newsletters/2025-04-02/stablecoins-are-growing-up?embedded-checkout=true

jinse

jinse