In-depth analysis Spark: Active Capital Allocation Device in the DeFi Field

転載元: jinse

06/20/2025·2DAuthor: Eren, Four Pillars; Translation: Golden Finance xiaozou

Summary of this article:

In the past, banks relied on physical vouchers and suffered massive bankruptcy due to their inefficient intermediary structure. Today's financial system continues this complexity and operates in an indirect ownership model. As tokenized assets and stablecoins become the new core of global finance, banks are facing a moment of transformation.

Spark's vision is to solve the inefficiency problem of traditional banking and the scalability limitations of the existing DeFi currency market and position it as the most advanced on-chain earnings engine. To achieve this vision, Spark operates Spark Liquidity Layer (SLL)—an automated asset allocation system, and SparkLend—a low-cost, high-liquid lending market.

Spark Liquidity Layer (SLL) acts as an on-chain asset management engine to monitor liquidity status, DeFi protocol yield and reserve levels in real time, and perform automatic rebalancing. Currently, Spark has made strategic capital allocation between DeFi protocols (Morpho, Aave, Ethena) and real-world assets (RWAs, such as BUIDL, Superstate), with assets under management exceeding US$4.1 billion and cumulative income exceeding US$190 million.

SparkLend operates a fixed-rate lending market funded by Sky, achieving high capital efficiency by using sUSDS as collateral. Under this structure, SparkLend's total locked value (TVL) has exceeded US$3.4 billion.

Spark's strategy is not necessarily groundbreaking, but through low-cost fundraising and refined capital deployment, it creates a structural advantage that is difficult to replicate. As demonstrated by sUSDS's stable income payments, its ability to continuously provide high returns helps to create an enabling environment for attracting large-scale capital.

1. You can save and borrow, but it is not a bank

The banking industry is facing a structural turning point again. To understand this moment, it is necessary to review the development history of the bank. Banks were born during the rise of commercial capitalism—the English goldsmiths in the 17th century kept their clients’ gold and issued deposit certificates. These certificates began to circulate as currency and eventually became collateral for credit creation, laying the foundation of the modern banking system. With the establishment of the central bank system, financial institutions have become the core infrastructure for asset custody, credit issuance and payment settlement. The Industrial Revolution prompted the separation of commercial banks from investment banks, and by the end of the 20th century, the functions of banks had extended from physical outlets to digital banks and global financial networks.

Despite the changes in form, the core function of the bank has never changed: as an intermediary that stores excess capital and redistributes it to the demand field, maximizing capital efficiency. However, implementation methods and tools have always continued to evolve with mainstream technologies and financial environment.

Nowadays, when tokenized assets and stablecoins reshape the financial landscape, is the bank itself also at a time when changes must be made?

" Yes, you can save and borrow on Spark. But it's not a bank." —Spark

The Spark protocol introduced in this article presents an on-chain capital configurator optimized for the ever-changing DeFi financial landscape. In subsequent chapters, we will deeply analyze Spark's operating mechanism and explore how it differentiates from the traditional banking model in the dimension of capital efficiency.

2. Banks are the remains of the last century

2.1 Historical backtrack: Paper bill crisis

In the 1960s, Wall Street ushered in great prosperity. Low interest rate environment, attractive dividend returns and increased institutional participation have caused transaction volume to quadruple between 1960 and 1968. However, until 1969, even though the bull market continued, many brokerages were on the verge of collapse. The reason is surprisingly simple: paper infrastructure is overwhelmed.

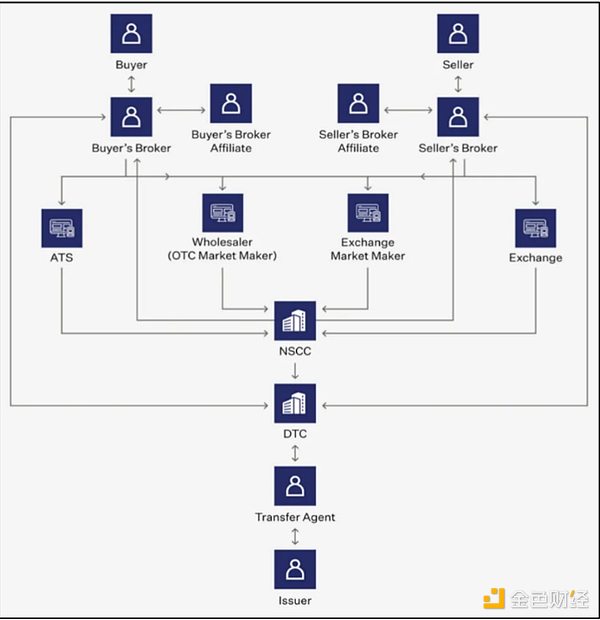

Before the emergence of modern liquidation systems, stock ownership was completed through physical paper vouchers. The seller submits the certificate to the broker, which is transferred to the buyer's broker, and then passes it to the transfer agency of the issuing company. The agent must register for changes in the shareholders' register, cancel old certificates and issue new certificates. This multi-link process may involve up to 68 independent operations, which takes about four working days.

As the transaction volume soared, the liquidation process was completely paralyzed. In the end, billions of dollars in transactions cannot be settled, millions of vouchers are lost, and dividend payments fail. Many brokerages are in a serious liquidity crisis: some misappropriate customer assets to fulfill their contracts, while others fill the gap through open market share repurchase. These operations were acquiesced in a bull market, but when the market turned bearish in the late 1960s, the sharp drop in commission income made institutions unable to bear the accumulated debt pressure. This "paper bill crisis" became the worst financial infrastructure failure after the Great Depression, and ultimately gave birth to the mainstream indirect holding model today.

**2.2 Current situation: Structural chronic diseases of indirect holding

model**

After the paper bill crisis, the capital market abandoned the physical certificate and turned to the indirect holding model. In this system, the legal ownership of securities is no longer owned by an investor individual, but is held by a broker or custodian. Changes in ownership are no longer achieved by modifying the entity voucher name, but rely on bookkeeping updates of the internal ledgers of the intermediary.

Although this system improves transaction efficiency, it also solidifies structural complexity and intermediary control.

First of all, the liquidation process is no longer straightforward. The transactions that could have been completed directly by both buyers and sellers now require the participation of brokers, traders, market makers, exchanges, clearing houses, central custodians and other parties. All parties perform a single function and are separated or overlapped with each other, which only increases the cost of friction. What's more, these intermediary institutions collect handling fees, spreads and data rents in multiple links of the transaction chain.

Secondly, the indirect mode concentrates transaction data flow and control rights at least in the hands of the intermediary, creating information asymmetry and opacity. Since investors are not legal holders, they often cannot view their positions or execution paths in real time. Intermediaries commercialize data through information blockade or paid services.

Under this structure, intermediaries are no longer just service providers, but also economic stakeholders embedded in the transaction structure itself. In the ultimate financial system, the complex structure of intermediation and value grabbing push up transaction costs, and the overall efficiency does not increase but decreases.

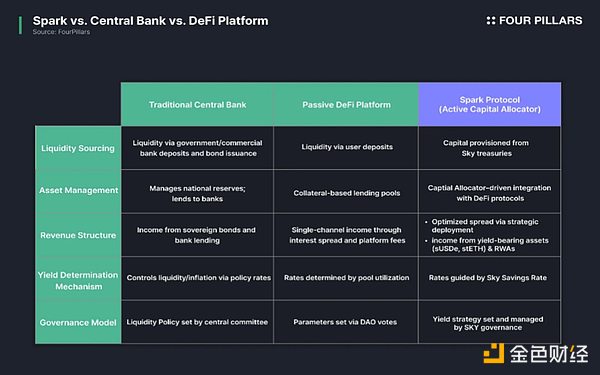

3. Spark in-depth analysis: DeFi 's active capital configurator

Spark was born to solve the problems of systemic inefficiency and opacity in the traditional banking industry. However, the idea of breaking through the limitations of the traditional financial system through DeFi is not a completely new thing. Since the early stage of DeFi development, countless protocols have always pursued common goals such as point-to-point transactions, automated clearing and transparent data access.

However, the existing money market model has structural limitations. They mainly act as intermediaries between borrowers and lenders, but failed to integrate financial hub functions such as yield policy, capital configurator management and risk diversification into a unified system. This makes it difficult to construct a coordinated flow between benefits and borrowing costs, and it is impossible to improve the return on capital. For users, it often means that predictable and sustainable benefits are difficult to obtain.

Spark achieves differentiation by building a unified financial architecture with on-chain capital configurator as the core, and the design simultaneously improves capital efficiency and system stability. Spark obtains low-cost funds from Sky and strategically allocates them to mainstream agreements such as Morpho, Aave, Ethena, BUIDL and SparkLend. These assets are managed independently through off-chain monitoring software to evaluate yield, risk and efficiency in real time. The resulting gains allocate compound interest to sUSDS holders—a interest-generating stablecoin minted using USDS, USDC or DAI through Spark Savings.

This architecture allows Spark to break through the passive role of the traditional currency market and become an active capital configurator across the DeFi ecosystem. This brings stronger liquidity, attracts institutional funds and achieves economies of scale. As of the second quarter of 2025, Spark's total locked position value (TVL) has exceeded US$7.5 billion.

The subsequent chapters will explore the relationship between Sky and Spark, and will deeply analyze SparkLend and Spark Liquidity Layer (SLL) - two core engines that drive the financial stack on the Spark chain.

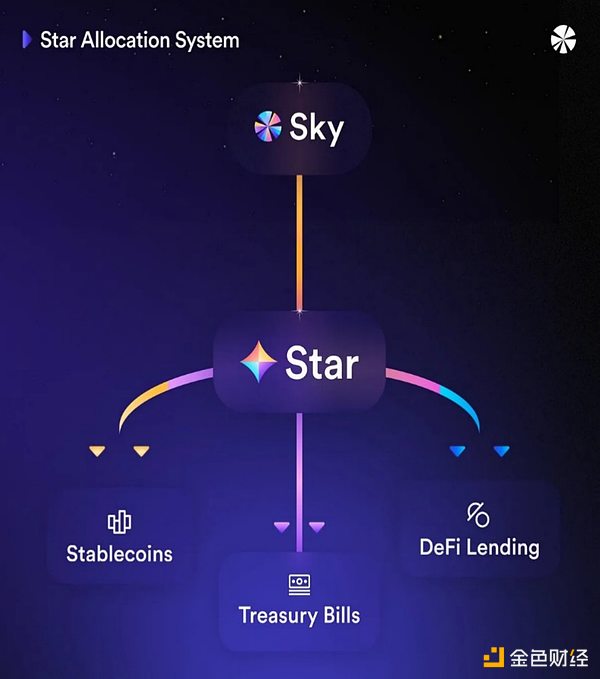

3.1 The first star

Spark plays the Star role in the Sky (formerly MakerDAO) ecosystem and is put into operation as the first Star - the autonomous unit in Sky 's vast Star ecosystem. Sky is a decentralized, reserve-backed agreement that has issued USDS (formerly DAI) and managed interest rate policies since 2017. As an important part of the asset allocation diversification and revenue generation strategy, Sky launched the "Star Plan", and Spark, as the first Star, has the mission of deploying funds to on-chain and off-chain assets (including RWA) to obtain profits.

Although Spark operates independently, its capital structure and strategic direction are still deeply bound to Sky. For example, the initial funds supporting the Spark lending market and capital allocation engine are directly derived from Sky. Therefore, Spark's borrowing interest rates, fee structure and income flow are essentially related to Sky reserves. To understand Spark's architecture, we must first analyze the operating mechanisms of SSR and USDS.

3.1.1 SSR and Spark Savings System

Sky Savings Rate (SSR) is the base deposit interest rate set by Sky Governance, representing the annualized rate of return on USDS deposits. Unlike the variable interest rates commonly found in the DeFi field that fluctuate according to liquidity conditions, SSR is determined through governance voting.

Specifically, the Sky risk management team will propose an SSR adjustment plan based on market conditions and agreement revenue. These proposals were reviewed by the community and approved by on-chain voting. The mechanism gives Sky the ability to flexibly adjust interest rate policies based on the macroeconomic environment rather than short-term liquidity pressures.

The source of SSR is Sky protocol revenue, which is generated by RWA investments (such as U.S. Treasury bonds) and DeFi deployments through Spark. This clearly shows the linkage between Sky and Spark: Spark is not only a revenue enhancement engine in the DeFi ecosystem, but also a key source of revenue that supports Sky SSR. In fact, Sky currently earns more than $400 million in reserves every year, of which 25% comes from SparkLend and SLL, and the rest comes from RWA strategies such as vaults.

As a source of income, the Spark Savings system acts as the front-end

interface for users. Users can deposit USDS or USDC and obtain sUSDS/sUSDC in

return. These interest-generating assets will automatically compound interest

based on SSR. This means that the value of sUSDS continues to grow in real

time, reflecting cumulative returns. Currently, the total deposit amount of

Spark savings system has exceeded US$3.1 billion.

As a source of income, the Spark Savings system acts as the front-end

interface for users. Users can deposit USDS or USDC and obtain sUSDS/sUSDC in

return. These interest-generating assets will automatically compound interest

based on SSR. This means that the value of sUSDS continues to grow in real

time, reflecting cumulative returns. Currently, the total deposit amount of

Spark savings system has exceeded US$3.1 billion.

3.1.2 USDS and Spark PSM: Multi-chain anchor stable redemption system

As mentioned earlier, USDS is a stablecoin issued by Sky. Spark forms a deep correlation with USDS by expanding its application scenarios: it serves as a conversion gateway for converting USDS into an interest-generating stablecoin sUSDS, and also serves as the allocation layer for deploying USDS to the lending market and on-chain assets. This process not only generates benefits, but also helps consolidate the anchoring stability of USDS.

Spark also plays a key role in maintaining USDS price stability through the anchor stability module ( PSM ). This module supports instant redemption of zero slippage between multiple chains such as Ethereum, Base and Arbitrum. For example, when a user redeems sUSDS as USDC, PSM will use the fund pool reserves to complete 1:1 redemption in the background to ensure that the user obtains USDC liquidity instantly.

By supporting large-scale redemption and seamless transfer of cross-chain assets, Spark PSM has effectively alleviated the slippage problem and liquidity separation between the network. This is crucial to maintaining the price balance of stablecoins during periods of volatile or high redemption demand.

Here are the detailed operating mechanisms of Spark PSM:

Reserve allocation: Large-scale USDC reserves from Sky are injected into PSM contracts deployed in support chains such as Base and Arbitrum.

sUSDS redemption USDC: When a user redeems USDC with sUSDS, PSM destroys sUSDS and releases equivalent USDC from the reserves. The exchange rate is calculated based on the accumulated SSR income determined by the Sky Cross- chain Savings Rate Oracle (for example, 1 sUSDS=1.05 USDC).

USDC casting sUSDS: When the user deposits USDC, PSM casts a new USDS at a fixed ratio of 1:1.

All redemptions are executed at a price of $1 anchor, completely eliminating slippage and minimizing market volatility risks. Currently Spark maintains USDC/USDS liquidity of over US$100 million on the Base chain through PSM. Relying on the US$1.3 billion USDC reserves held by Sky, Spark plans to expand its multi-chain redemption infrastructure to more networks to support seamless capital flows and ensure USDS anchoring stability, while helping SLL achieve scale expansion of cross-chain liquidity allocation.

3.2 SparkLend: Lending Agreement

SparkLend is a lending protocol built on Aave v3 fork. It deeply integrates Spark liquidity layer (SLL) and the Sky ecosystem to specifically optimize large-scale borrowing needs. Relying on the low-cost USDS liquidity offered by Sky, the agreement is designed to provide highly competitive borrowing rates.

Like other over-collateralized lending agreements, SparkLend allows users to deposit assets to earn income, or provide collateral to borrow assets. The borrowing interest rates of each asset are algorithmically adjusted according to the capital utilization rate: the interest rate increases when borrowing demand rises, and the interest rate decreases when demand decreases. This inertia-based interest rate model realizes the autonomous balance of liquidity in the capital pool. (Special note: USDS adopts a fixed interest rate mechanism, and its interest rates are directly linked to SSR, which will be described in detail below.)

Although SparkLend is structurally similar to other DeFi lending markets, it has unique advantages through deep binding with Sky and customized mortgage settings:

First, SparkLend strictly limits the types of supported collateral assets to enhance stability and reduce volatility risks. For example, SparkLend on the Ethereum main network only supports high-liquid assets such as ETH, stETH, WBTC, USDC, USDS and sUSDS. Each asset is subject to the conservative loan value ratio (LTV) and loan ceiling set by Spark risk parameters. By streamlining the scope of collateral assets, SparkLend effectively reduces the risk of chain liquidation or collateral failure during severe market fluctuations, and strengthens the overall stability of the agreement.

Secondly, SparkLend adopts a customized interest rate model directly linked to SSR for the USDS market. Unlike most borrowing costs that fluctuate with short-term liquidity, the agreement provides USDS borrowing with fixed SSR rates set by Sky Governance. This ensures that users receive predictable and continuously low-cost USDS borrowing services.

Third, SparkLend directly receives liquidity injection from Sky vault. In practice, this means that SparkLend's USDS funding pool continues to receive the USDS supply from Sky's newly minted. These funds can be withdrawn or resupplied dynamically according to the requirements of the agreement. What is more noteworthy is that when a user deposits USDS to SparkLend, the system will automatically convert it to sUSDS, allowing the user to obtain both the double returns of lending income and SSR rewards.

By deeply integrating Sky's architectural advantages, SparkLend has created a

highly predictable and capital-efficient lending market. The adoption of a

fixed interest rate mechanism based on SSR in the USDS market effectively

reduces uncertainty and supports long-term funding planning. More importantly,

since sUSDS continues to generate returns when it is collateral, users can

maximize capital efficiency without sacrificing returns.

By deeply integrating Sky's architectural advantages, SparkLend has created a

highly predictable and capital-efficient lending market. The adoption of a

fixed interest rate mechanism based on SSR in the USDS market effectively

reduces uncertainty and supports long-term funding planning. More importantly,

since sUSDS continues to generate returns when it is collateral, users can

maximize capital efficiency without sacrificing returns.

As of the second quarter of 2025, SparkLend's total locked-in value (TVL) has exceeded US$3.4 billion, and the Ministry of Finance holds approximately US$1.8 billion in assets. It is worth noting that SLL, the capital allocation engine of Spark's core, has generated cumulative revenue of over US$190 million, of which SparkLend accounts for 62% (about US$120 million), becoming the largest single source of income in the Spark ecosystem.

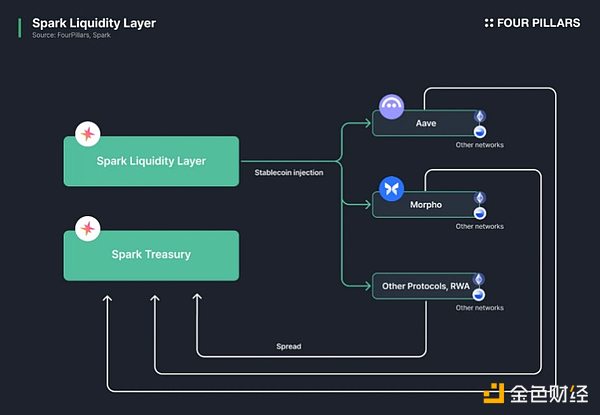

3.3 SLL (Spark Liquidity Layer): On-chain Capital Allocation

3.3.1 SLL operation mechanism

SLL is the core system that defines Spark as a "DeFi active capital

configurator". It serves as Spark's on-chain capital allocation engine,

obtains low-cost liquidity from Sky and deploys it to multiple chains and

multiple DeFi protocols. The proceeds generated through these deployments will

flow back to the Sky treasury, meaning that SLL is both a source of funding

for USDS and sUSDS returns and the economic foundation that supports SSR

payments.

SLL is the core system that defines Spark as a "DeFi active capital

configurator". It serves as Spark's on-chain capital allocation engine,

obtains low-cost liquidity from Sky and deploys it to multiple chains and

multiple DeFi protocols. The proceeds generated through these deployments will

flow back to the Sky treasury, meaning that SLL is both a source of funding

for USDS and sUSDS returns and the economic foundation that supports SSR

payments.

The functions of SLL are not limited to capital allocation. It integrates with off-chain monitoring software to continuously observe cross-chain liquidity status, earnings performance of external DeFi protocols, and Sky's reserve level. Based on these indicators, SLL will automatically rebalance liquidity in real time. For example, if the deposit surge in PSM on the Base chain results in insufficient USDC balance, the system will bridge additional USDC from the Ethereum main network through CCTP; if there is idle USDC on the Layer2 network, some funds will be withdrawn and reconfigured to the main network.

SLL operates through three core components:

Sky Configuration Vault: This vault serves as a credit tool that allows astral bodies including Spark to cast USDS with Sky's collateral. Currently, USDS (formerly DAI) has been issued through Spark Vault. These funds acquired at low cost are then used by SLL for strategic capital allocation across DeFi.

SkyLink: a native cross-chain bridge developed by Sky, which supports the transfer of USDS and sUSDS between connected networks. This allows SLL to quickly and securely automate cross-chain fund transfers without relying on intermediaries. For the transfer of external stablecoins such as USDC, SLL uses Circle's Cross-chain Transfer Protocol (CCTP) to ensure efficient liquidity routing.

Spark PSM: As mentioned earlier, the Spark anchor stability module supports instant zero slip redemption between USDS, sUSDS and USDC on each chain. During the rebalancing process, it helps SLL perform price-biased asset conversions, maintain anchor stability and minimize liquidity losses.

Spark uses this infrastructure to deploy billions of dollars between various

DeFi protocols and asset types. All deployments are completely transparent,

and users can view real-time information such as asset configuration,

SparkLend total lock value and protocol-level returns through the Spark data

center.

Spark uses this infrastructure to deploy billions of dollars between various

DeFi protocols and asset types. All deployments are completely transparent,

and users can view real-time information such as asset configuration,

SparkLend total lock value and protocol-level returns through the Spark data

center.

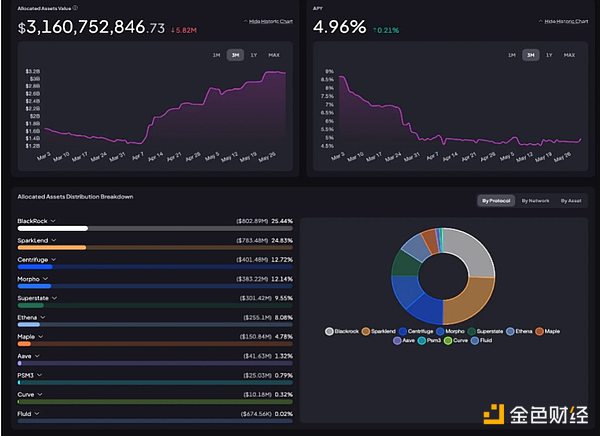

The latest data shows that the current total DeFi policy configuration exceeds US$3.1 billion. Among them, BlackRock (through BUIDL) holds US$800 million, and SparkLend holds US$900 million, ranking among the top two major configuration directions. Spark injects liquidity into BUIDL to obtain treasury bond endorsement income, while creating additional income through deposit interest on the self-operated lending platform SparkLend.

SLL's revenue sources are highly diversified: it does not rely on a single channel, but can organically combine the stable returns of real assets with DeFi native high-yield strategies. In the RWA field, Spark provides liquidity for tokenized treasury products such as Superstate, Centrifuge, and Maple. These positions generate reliable returns based on US government bonds; in the DeFi field, it cooperates with agreements such as Ethena, Morpho, and Aave to pursue higher potential returns through holding direct exposure to synthetic interest-generating assets such as sUSDe, and through the deployment of complex strategies of Morpho vaults.

This multi-pronged strategy has enabled SLL to generate more than $190 million in revenue. Among them, SparkLend contributes about 62%, proving that Spark has built an internal income engine that does not rely on external protocols. Morpho Vault has become the second largest contributor with a 29% return, which verifies Spark's effective performance of the "DeFi Central Bank". The following will explore how Spark integrates with a wider protocol and expands its role in the ecosystem.

4. How SLL leverages the DeFi ecosystem

4.1 Integrated Aave Agreement Lending Market

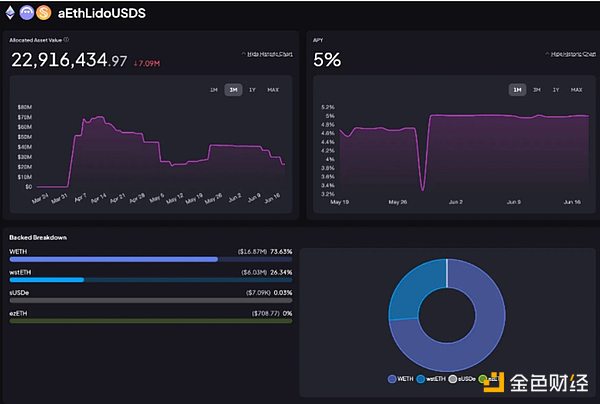

Through SLL, Spark provides USDS liquidity to Aave 's Lido market, enabling users to borrow and borrow with assets such as WETH and wstETH as collateral. In the process, Spark plays the role of liquidity providers and earns loan proceeds. Currently, approximately US$20 million worth of ETH assets are deployed in the Aave market, generating a cumulative revenue of US$400,000.

One of the core advantages of SLL integration is its ability to stabilize stablecoin lending rates between the Aave Core market, the Prime market and the Base market. When lending rates in a particular market rise, SLL dynamically rebalances liquidity to narrow interest rate differences. This mechanism not only improves the predictability and stability of interest rates within Aave's ecosystem, but also allows Spark to obtain sustainable returns through active liquidity supply.

4.2 Integrated Morpho protocol lending market

Spark uses the Morpho protocol to maximize liquidity supply benefits. Liquidity is directly injected into the MetaMorpho vault to build a diversified lending market. Currently, approximately US$400 million USD and US$500 million DAI have been deposited into the Spark-managed vault.

Most USDC liquidity is configured to the cbBTC/USDC market, and users can

borrow USDC using cbBTC (Coinbase encapsulated BTC). Through this market,

Spark has earned revenue from USDC it deploys, generating approximately $1.5

million in revenue over the past year.

Most USDC liquidity is configured to the cbBTC/USDC market, and users can

borrow USDC using cbBTC (Coinbase encapsulated BTC). Through this market,

Spark has earned revenue from USDC it deploys, generating approximately $1.5

million in revenue over the past year.

DAI liquidity is deployed on Morpho’s lending platform Morpho Blue, which operates with Pendle-based PT-USDS and other Ethena-based assets. With this configuration, users can borrow DAI using USDe or sUSDe as collateral. Because Ethena provides revenue for USDe through Delta hedging strategies and RWA returns, this pairing can create diversified revenue strategies for DAI. Spark earns borrowing income by supporting these high-yield mortgage pools, and related positions generate cumulative revenue of approximately $50 million.

In Morpho Blue's Ethena integration market, Spark accepts Pendle's principal tokens (PT-sUSDe and PT-USDe) as collateral and provides DAI liquidity accordingly. This lending structure is established by Spark's Sky funds to the Pendle position allocation DAI (as described in this governance post), allowing users to borrow DAI with PT-sUSDe mortgages and obtain fixed income collateral to achieve efficient capital lending.

This strategy allows users to earn staking income from sUSDe, and to obtain enhanced fixed income through PT, while unlocking additional liquidity for leverage operations. For Spark, this approach improves capital allocation flexibility and optimizes protocol-level returns.

4.3 Direct holding of Ethena assets

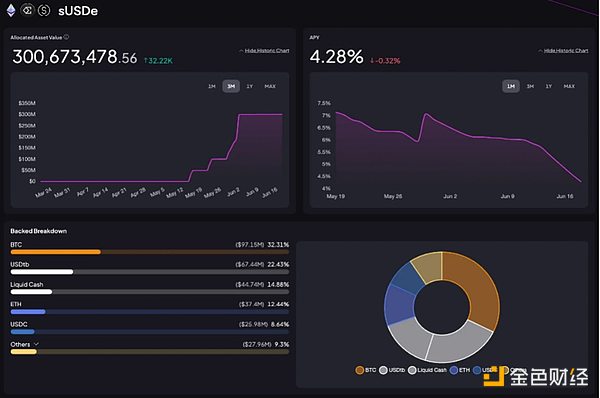

Spark is expanding its direct holdings in Ethena 's USDe and sUSDe through SLL. The agreement plans to allocate up to $1.1 billion in funds for this strategy, and currently holds approximately $300 million in USDe and sUSDe in the capital configurator. These high-yield assets achieved an average annualized rate of return of 18% in 2024, and will work with existing holdings such as USDC, USDS and sUSDS to increase the overall returns of SLL.

Unlike indirect exposure through lending markets such as Morpho, this strategy allows Spark to directly obtain Ethena's profit distribution without intermediary participation. This allows Spark to significantly reduce external dependencies while maximizing potential returns. As of now, the strategy has generated approximately $1.5 million in cumulative returns.

5. How Spark builds a moat

As described above, Spark has built a unified financial hub through SparkLend and SLL, solving the limitations of traditional banks and traditional DeFi currency markets. But where does Spark's competitive moat come from? The answer lies in its deep integration relationship with Sky, its competitive advantage of interest-generating stablecoins, and its operational efficiency achieved through SLL.

5.1 Low-cost funds based on SSR

Spark 's core strengths stem from Sky's huge capital base and the low-cost funding structure it provides. As of now, Sky holds about US$11 billion in collateralized assets, corresponding to US$8.3 billion in USDS liabilities, maintaining an over-collateralized ratio of about 131%. This means that there is US$2.7 billion in excess collateral assets, which not only consolidates the financial robustness of the Sky ecosystem, but also provides a capital operation basis for astral bodies such as Spark.

These low-cost funds from Sky are efficiently allocated to SparkLend and SLL. SparkLend provides stable fixed interest rates through SSR, laying the foundation for long-term retention of users; while SLL enables Spark to operate configurators with extremely high capital efficiency and rely almost no external liquidity.

The income generated by the rate of return difference and interest-generating asset exposure is returned to Sky's SSR module as the financial pillar, and the other part is retained as agreement revenue. This structure allows Spark to keep capital costs to a minimum while maintaining a stable income base, which has fundamental advantages in sustainability and asset efficiency compared to traditional DeFi protocols.

5.2 Forward loop between sUSDS and SparkLend

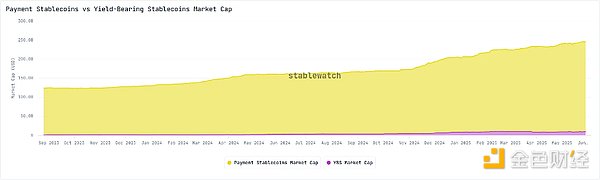

Interest-generating stablecoins have become an effective tool to improve the capital efficiency of the stablecoin market. Since the end of 2023, the market has grown rapidly, with a scale of about US$10 billion as of the second quarter of 2025, and its market value has nearly tripled its growth in the past year.

In this rapidly growing field, Sky's sUSDS shows strong competitiveness in revenue distribution. According to Stablewatch data, sUSDS has allocated more than $82 million in revenue so far, second only to Ethena's sUSDe in the cumulative payment income ranking.

The key factor behind this performance is Sky's interest rate competitiveness. The annualized yield provided by sUSDS is usually maintained in the range of 5% to 8%, which is comparable to the average 6% yield level of sUSDe during the same period. This attractive interest rate continues to drive sUSDS deposit demand, thereby optimizing Spark's financial structure.

5.2.1 Improve capital capacity through sUSDS demand

sUSDS is an interest-generating token obtained by a user after depositing USDS into the SSR. As sUSDS demand grows, more USDS is deposited into SSR, prompting Sky's Ministry of Finance to expand its asset size and increase its SDS issuance. After the expansion of the Ministry of Finance, Sky can provide Spark with more low-cost funds, further enhancing Spark's SSR-based lending capabilities. This basis allows SparkLend to provide borrowing rates below market level, consolidating its interest rate competitive advantage.

5.2.2 Expand SparkLend demand through sUSDS mortgage

SparkLend accepts sUSDS as collateral, allowing users to continuously obtain SSR returns while maintaining asset liquidity. This dual advantage of income and liquidity forms a strong incentive to use SparkLend.

When SparkLend motivates users to mortgage loans with sUSDS, and sUSDS realizes its effectiveness through SparkLend, a closed loop of mutual reinforcement is formed. The increase in user sansUSDS pushes up the total lock-in value of SparkLend, thereby expanding the agreement lending capacity, allowing SparkLend to issue more loans and generate more revenue.

Ultimately, the feedback mechanism formed between sUSDS and Spark built a virtuous cycle: more sUSDS deposits expanded Spark's Ministry of Finance assets, improved Spark's ability to obtain low-cost funds, and enabled SparkLend to provide more competitive loan interest rates, increase fund utilization and increase agreement revenue. After these returns flow back to SSR, they can provide a more attractive annualized rate of return, further stimulate sUSDS demand and complete the closed loop of the cycle.

**5.3 Balance the high returns and low risks of DeFi and traditional

finance**

With the integration of real-world assets (RWA) and crypto assets with traditional financial systems, the boundaries between DeFi and TradFi continue to disappear. Spark aims to achieve the dual goals of high returns and low risks by balancing DeFi native returns with RWA basic returns.

5.3.1 DeFi native income

In the money market field, Aave has become an important participant; Ethena also performed strongly in the interest-bearing stablecoin track. How does Spark compete? It adopts a capital configurator-driven strategy to avoid direct confrontation.

At present, DeFi is increasingly showing the characteristics of "Fat DeFi" - the protocol focuses more on improving composability. Spark adapts to this trend through SLL: inject liquidity into vaults such as Morpho, directly obtain interest-generating assets from protocols such as Ethena, and strategically connect to Aave's deep liquidity pool and huge user base. This multi-channel strategy has significantly improved Spark's capital efficiency.

5.3.2 RWA Income

While the open source nature of DeFi allows code to be easily copied, the most rugged moats often come from non-programmatic advantages. This is exactly the deep integration of Spark with traditional finance - other protocols may replicate the technical architecture, but it is difficult to replicate its revenue structure.

Spark's Tokenization Grand Prix program is proof of this. The plan marks an important milestone in the integration of DeFi and TradFi: Sky promised to invest $2 billion to buy the most competitive tokenized US short-term Treasury products, ultimately attracting proposals from 39 institutions including BlackRock, Janus Henderson, Superstate, etc. SLL selected the best to buy BUIDL, USTB and JTRSY.

The assets acquired by Sky are all low-volatility, high-liquidity short-term U.S. Treasury bond endorsements, and meet the requirements of European and American securities regulatory. This has built a compliance framework for institutional funds to enter DeFi and has strengthened the anchoring stability and liquidity defense capabilities of USDS for a long time.

Spark's core advantage lies in integrating DeFi's flexible return strategy with RWA's stability through SLL: on the one hand, it improves returns through interaction with external DeFi protocols, and on the other hand, it reduces volatility by allocating real assets such as US Treasury bonds. In the process, Spark redefined the relationship between DeFi and traditional finance—thinking it as a "reward-stable" spectrum of continuity rather than two areas of separation.

6. Spark 's future development

Spark's development direction is very clear: it aims to become the most leading scale income engine in the DeFi field, and is clearly committed to breaking through the inefficiency and opacity of the traditional banking industry and the scale limitations of the traditional currency market.

Although Spark's strategy may not be novel at first glance, it has achieved competitive interest rates and stable returns by reducing capital costs and accurately managing interest-generating assets exposure. More importantly, combining the large-scale funding provided by SSR with the capital configurator model spanning DeFi/TradFi has formed a structural moat that is difficult to replicate. As the capital market continues to migrate to the chain, Spark is very likely to develop into an on-chain capital hub. This development path deserves continuous attention.