Arthur Hayes: Stablecoin narrative is hot, and IPO may be a "dead game", but I advise you not to short

転載元: chaincatcher

06/18/2025·6DAuthor: Arthur Hayes

Compiled by: TechFlow

(Any view expressed here is the author's personal opinion and should not be used as the basis for investment decisions or should not be construed as a recommendation or recommendation for conducting investment transactions.)

Given that Circle CEO Jeremy Allaire seems to have no choice but to be in place under the “instruction” of Coinbase CEO Brian Armstrong (the author here is sarcastic, suggesting that it lacks independence and is controlled by Coinbase), I hope that for investors who trade any “stablecoin”-related assets in the open stock market, this article will help you avoid huge risks and losses when the seller imposes worthless assets on retail investors who are unsure of the truth. In this order, I will start discussing the past, present and future of the stablecoin market.

In the capital markets, professional cryptocurrency traders are somewhat unique. If they want to survive and develop, they need to have an in-depth understanding of how funds flow in the global fiat banking system. In contrast, stock investors or foreign exchange speculators do not need to understand how stocks or currencies are settled and transferred, because the brokerage they must use will provide this service silently in the backstage.

First, buying your first bitcoin is not easy; what is the best and safest choice is not clear. For most people, the first step (at least when I started getting involved in cryptocurrencies in 2013) is to buy Bitcoin by sending fiat bank wires directly to another person or paying in physical cash. You will then upgrade to trading on an exchange that offers bilateral markets, where you can trade larger bitcoins at a smaller fee. But depositing your fiat currency into the exchange past/present is not easy or direct. Many exchanges do not have solid banking ties or are in a regulatory gray area in their country, which means you cannot wire funds directly to them. The exchange came up with workarounds, such as directing users to transfer fiat currency directly to local agents, where the agent issues cash vouchers on the exchange; or setting up an adjacent business that appears to be cryptocurrency-free in the eyes of the bank account manager, thereby obtaining an account and guiding users to transfer funds there.

Scammers use this friction to steal fiat currency in various ways. The exchange itself may lie about where the funds are going, and then one day... puff - the website disappears along with the fiat currency you have worked hard to earn. If you use a third-party intermediary to transfer fiat currency inside and outside the crypto capital market, these people may evaporate from the world with your funds at any time.

Because there are risks in transferring fiat currencies in the cryptocurrency capital market, traders must know and trust the cash flow operations of the trading objects in detail. I learned how to handle global payments when funds flowed within the banking systems of Hong Kong, Mainland China and Taiwan (I call this region Greater China).

Understanding how funds flow in Greater China helped me understand how major Chinese and international exchanges (Bitfinex) do business. This is important because all true cryptocurrency capital market innovations take place in Greater China. This is especially true for stablecoins. Why this is important, the reasons will become obvious.

The success story of the greatest cryptocurrency exchange in the West belongs to Coinbase, which opened in 2012. However, Coinbase’s innovations are gaining and maintaining banking relations in one of the most hostile markets to financial innovation—the Pax Americana. Beyond that, Coinbase is just a very expensive cryptocurrency brokerage account, and that’s exactly what it takes to drive its early shareholders to become billionaires.

The reason I wrote another long article about stablecoins is because of the great success of the Circle IPO. It should be clear that Circle is seriously overvalued, but the price will continue to rise. This listing marks the beginning, not the end of this stablecoin fanaticism. The bubble will burst after a stablecoin issuer is launched in a public market (probably in the United States) that will use financial engineering, leverage and amazing acting skills to separate tens of billions of capital from fools. As usual, most people who hand over their precious capital won’t understand the history of stablecoins and cryptocurrency payments, why the ecosystem evolves like this, and what this means for which issuers will succeed. A very reliable, attractive guy will step onto the stage, squirt all kinds of nonsense, waving his (most likely male) hands back and forth, and convince you that the leveraged shit he is peddling is about to monopolize the trillions of stablecoins total addressable market (TAM).

If you stop reading here, the only question you have to ask yourself when evaluating investments in stablecoin issuers is: How will they distribute their products?

To do a large scale distribution – I mean being able to reach millions of users at affordable costs – issuers have to use a pipeline of cryptocurrency exchanges, Web2 social media giants or traditional banks. If they don’t have distribution channels, there is no possibility of success. If you can't easily verify that the publisher has the right to push products through one or more of these channels, run away!

Hopefully my readers won’t burn their capital this way, because after reading this article, they can think critically about the stablecoin investment opportunities placed before them. This article will discuss the evolution of stablecoin distribution.

First, I will talk about how and why Tether has grown and grown in Greater China, which has laid the foundation for their conquering stablecoin payments in the Global South. Then I will discuss the initial token issuance (ICO) boom and how this creates a real product market fit for Tether. Next I will discuss the first attempt of the Web2 social media giant to enter the stablecoin game. Finally, I will briefly mention how traditional banks will be involved.

Reiterate it, because I know X (platform) makes it difficult to read prose with more than a few hundred characters, and if a stablecoin issuer or technology provider cannot distribute through cryptocurrency exchanges, Web2 social media giants or traditional banks, they shouldn't do it.

Cryptocurrency Banking Business in Greater China

Currently successful stablecoin issuers Tether, Circle and Ethena have the ability to distribute their products through large cryptocurrency exchanges. I will focus on the evolution of Tether and mention Circle slightly to illustrate that it is nearly impossible for any new entrant to replicate their success.

At first, cryptocurrency trading was ignored. For example, from 2014 to the late 2010s, Bitfinex has maintained its title as the largest non-China global exchange. At that time, Bitfinex was owned by a Hong Kong-operated company that had various local bank accounts. This is great for an arbitrage trader like me who lives in Hong Kong, as I can wire funds to the exchange almost instantly. There is a street opposite my apartment in Sai Ying Pun, which contains almost all local banks. I would walk the cash between banks to reduce fees and the time it takes to receive the money. This is very important because it allows me to turn over my capital once a day on weekdays.

Meanwhile, in China, the three major exchanges, OKCoin, Huobi and BTC China, all have multiple bank accounts in large state-owned banks. It only takes 45 minutes to get to Shenzhen by bus. With my passport and basic Chinese ability, I opened various local bank accounts. As a trader in mainland China and Hong Kong, having a banking relationship means you can access all liquidity around the world. I am also very confident that my fiat currency will not disappear. Instead, every time I wired to some Eastern European registered exchanges, I lived in fear because I didn’t trust their banking channels.

But as cryptocurrency awareness increases, banks have begun to close their accounts. Every day you have to check the operational status of each bank and exchange relationship. This is very bad for my trading profits, and the slower the funds flow between exchanges, the less money I can make through arbitrage. But what if you could transfer electronic dollars on the crypto blockchain instead of through traditional banking channels? Then the US dollar—who was the lifeblood of the cryptocurrency capital markets as it is now—can move between exchanges almost for free on 24/7.

Tether’s team worked with the original founders of Bitfinex to create such a product. In 2015, Bitfinex allowed the use of Tether USD on its platform. At that time, Tether used the Omni protocol as a layer above the Bitcoin blockchain to send Tether USD (USDT) between addresses. This is a primitive smart contract layer built on top of Bitcoin.

Tether allows certain entities to wire dollars to their bank accounts, and in return, Tether will mint USDT. USDT can be sent to Bitfinex and used to purchase cryptocurrencies. Wow, that's amazing, why is it exciting to offer this product by a random exchange?

Stablecoins, like all payment systems, become valuable only when a large number of economically significant participants become nodes in the network. For Tether, apart from Bitfinex, cryptocurrency traders and other large exchanges need to use USDT to solve any real problem.

Everyone in Greater China is in the same situation. Banks are closing accounts of traders and exchanges. Plus, Asians want to get the dollar because their own currencies are vulnerable to shock devaluation, high inflation and low domestic bank deposit rates. For most Chinese, access to the US dollar and the US financial market is very difficult, or even impossible. Therefore, the digital dollar version offered by Tether, available to anyone who can access the internet, is super attractive.

The Bitfinex / Tether team went with the flow. Jean-Louis van der Velde, who has served as Bitfinex since 2013, has worked for Chinese automakers. He understands Greater China and works to make USDT the preferred dollar bank account for Chinese people with crypto-minded minds. Although Bitfinex has never had a Chinese executive, it has built a huge amount of trust between Tether and the Chinese cryptocurrency trading community. Therefore, you can be sure that the Chinese trust Tether. And in the Global South, overseas Chinese control the situation, as the Imperial citizens discovered in this unfortunate trade war, so the Global South is banked by Tether.

Just because Tether has a large exchange as its founding distributor does not guarantee success. The market structure has changed so much that trading altcoins against the US dollar can only be done through USDT. Let’s move forward to 2017, at the height of the ICO boom, Tether has truly solidified its product market fit.

ICO baby

August 2015 was a very important January as the People's Bank of China (PBOC) shocked the RMB against the US dollar, and Ethereum (the native currency of the Ethereum network) began trading. The macro and micro stages are transformed simultaneously. It was a legendary thing and ultimately drove the bull market from that time to December 2017. Bitcoin soared from $135 to $20,000; Ethereum rose from $0.33 to $1,410.

When printing money, the macro environment is always favorable. Because Chinese traders are marginal buyers of all cryptocurrencies (then referred to as Bitcoin only). If they feel that the RMB is unstable, Bitcoin will soar. At least that was the case at that time.

The impact depreciation of the People's Bank of China has exacerbated capital flight. Bitcoin had fallen from its all-time high of $1,300 before the bankruptcy of Mt. Gox in February 2014 to a low of $135 on Bitfinex earlier in the month, when Zhao Dong, the largest off-market bitcoin trader in China, suffered the largest margin call on Bitfinex at the largest ever, with a sum of 6,000 bitcoins. The rise was driven by the claim that China's capital flight; from August to October 2015, BTCUSD more than tripled.

The microscope is always the most fun place. The surge in altcoins really began when the Ethereum mainnet and its native currency, Ethereum, went online on July 30, 2015. Poloniex is the first exchange to allow Ethereum trading, and it was this vision that pushed it to the lead role in 2017. Interestingly, Circle went bankrupt when it bought Poloniex almost at the top of the ICO market. Years later, they sold the exchange to the noble Excellency Justin Sun for huge losses.

Poloniex and other Chinese exchanges are leveraging the new altcoin market by launching pure cryptocurrency trading platforms. Unlike Bitfinex, it does not need to connect to the fiat banking system. You can only deposit and withdraw cryptocurrencies to trade other cryptocurrencies. But this is not ideal, because traders instinctively want to trade altcoins/USD pairs. How can exchanges like Poloniex and Yunbi (Yunbi) (formerly the largest ICO platform in China) provide these trading pairs without the ability to accept fiat currency deposits and withdrawals? USDT is on the stage!

USDT can be moved on the network using the ERC-20 standard smart contract after it is launched on the Ethereum main network. Any exchange that supports Ethereum can also easily support USDT. Therefore, pure cryptocurrency trading platforms can provide altcoins/USDT trading pairs to meet market demand. This also means that digital dollars can flow seamlessly between major exchanges (such as Bitfinex, OKCoin, Huobi, BTC China, etc.) - places where capital enters the ecosystem - and more interesting and speculative places (such as Poloniex and Yuncoin) - places where gamblers play.

The ICO craze gave birth to the behemoth that later became Binance. CZ (Zhao Changpeng) resigned from his position as chief technology officer of OKCoin a few years ago due to a personal dispute with CEO Star Xu. After leaving CZ founded Binance with the goal of becoming the world's largest altcoin exchange. Binance has no bank account, and until today I don’t know if you can deposit fiat currency directly into Binance without using some payment processors. Binance uses USDT as its banking channel and quickly becomes the preferred place to trade altcoins, and the rest is history.

From 2015 to 2017, Tether achieved product market fit and established a moat against future competitors. Due to the trust of the Chinese trading community in Tether, USDT is accepted in all major trading venues. It is not used for payment at this time, but it is the most effective way to transfer digital dollars both inside and inside the cryptocurrency capital market.

By the late 2010s, it was difficult for exchanges to maintain bank accounts. Taiwan, China, has become the de facto cryptocurrency banking center of all the largest non-Western exchanges that control most of the liquidity of cryptocurrency transactions around the world. This is because several Taiwanese banks allow exchanges to open U.S. dollar accounts and somehow maintain agency relationships with large U.S. currency center banks, such as Wells Fargo. However, this arrangement began to collapse as agent banks asked these Taiwanese banks to expel all cryptocurrency customers, otherwise they would lose their chances of entering the global dollar market. As a result, by the end of the 2010s, USDT became the only way to transfer USD on a large scale in the cryptocurrency capital market. This consolidates its position as a dominant stablecoin.

Western participants, many of whom raise funds for narratives with cryptocurrency payments, scramble to create Tether’s competitors. The only large-scale survivor is Circle's USDC. However, Circle is at a clear disadvantage because it is a Boston-based U.S. company with no connection to the core of cryptocurrency trading and use—Greater China. Circle Unspecified information was/is still: China = terrible; United States = safe. This information is funny because Tether has never had a Chinese executive, but it was/is always associated with the Northeast Asian market and is now the global south.

Want to join social media

Stablecoin fanaticism is not new. In 2019, Facebook (now known as Meta) decided it was time to launch its own stablecoin, Libra. The appeal is that Facebook can provide U.S. dollar bank accounts to the entire world except China through Instagram and WhatsApp. This is what I wrote about Libra in June 2019:

The event horizon has passed. With Libra, Facebook has begun to get involved in the digital asset industry. Before I start analyzing, let me clarify one thing; Libra is neither decentralized nor censor-resistant. Libra is not a cryptocurrency. Libra will destroy all stablecoins, but who the hell cares. I don't shed tears at all of the projects that somehow are believed to have valued by a little-known sponsor and run on the blockchain.

Libra may cause commercial banks and central banks to decline. It may reduce their utility to a stupid regulated digital fiat currency warehouse. And these institutions should do this in the digital age.

The stablecoins offered by Libra and other Web2 social media companies could have stolen the limelight. They have the largest number of customers and have almost complete knowledge of their preferences and behavioral information.

Ultimately, American political institutions acted to protect traditional banks from real competition in the payments and forex fields. That's what I said at that time:

I have no good feelings for U.S. Rep. Maxine Waters' stupid remarks and actions on the U.S. House Financial Services Committee. But the outbreak of concerns she and other government officials stem from altruistic feelings towards their subjects, but from fear of subverting the financial services industry, an industry that allows them to fill their pockets and maintain their positions. The speed at which government officials has hastily condemned Libra tells you that the project contains some potential positive value for human society.

That was then, but now the Trump administration will allow competition in the financial markets. Trump 2.0 has no good impression of banks that disqualify his entire family platform during the administration of US President Biden. Therefore, social media companies are reviving plans to embed stablecoin technology natively into the platform.

This is good news for social media company shareholders. These companies can completely swallow up the revenue streams of traditional banking systems, payments and forex. However, this is bad news for any entrepreneur who creates a new stablecoin, as social media companies will build everything they need to support their stablecoin business internally. Investors in new stablecoin issuers must be wary of promoters boasting about working with or distributing through any social media company.

Other technology companies are also joining the stablecoin trend. Social media platforms X, Airbnb and Google are all having early discussions on integrating stablecoins into their business operations. In May, Fortune magazine reported that Mark Zuckerberg's Meta - a failed attempt on blockchain technology in the past - has been discussing with cryptocurrency companies introducing stablecoins for payments.

– Source: Fortune Magazine

My article "Libra: Zuck Me Gently"

Extinction of traditional banks

Like it or not, banks will not be able to continue to earn billions of dollars in annual revenue to hold and transfer digital fiat currency, nor will they earn the same fees when conducting forex transactions. I recently talked about stablecoins with members of a large bank and they said “we’re done.” They believe that stablecoins are unstoppable and prove it with the situation in Nigeria. I didn’t know how much USDT has penetrated the country before, but they told me that one-third of Nigeria’s GDP is done with USDT, even though the central bank is very serious about trying to ban cryptocurrencies.

They went on to point out that regulators are unable to stop it because adoption is bottom-up rather than top-down. When regulators notice and try to do something, it is too late, because adoption is already prevalent among the people.

Although there are people like them in the senior positions of every large traditional bank, the banking organism does not want to change because it means the death of many of its cells—that is, employees. With less than 100 employees, Tether can leverage blockchain technology to perform key functions of the entire global banking system. For comparison, consider JP Morgan, the world's best-run commercial bank, employs just over 300,000 people.

Banks are facing a crucial moment – adaptation or death. But complicating their efforts to streamline a bloated workforce and deliver the products the global economy needs is prescriptive regulation on how many people must be hired to perform certain functions. For example, my experience at BitMEX trying to open a Tokyo office and get a cryptocurrency trading license. The management team considers whether it should open a local office and obtain a license to conduct some limited types of cryptocurrency transactions outside our core derivatives business. The cost of compliance regulation is the problem because you can’t leverage technology to meet the requirements. The regulator stipulates that for each compliance and operational function listed, you must hire someone with the right level of experience. I don't remember the exact number, but I believe that it takes about 60 people a year, each making at least $80,000, a total of $4.8 million per year to perform all the prescribed functions. All of this work could have been automated with less than $100,000 per year for SaaS vendor fees. And I add that there will be fewer mistakes in doing this than hiring people who are prone to errors. Oh…and you can’t fire anyone in Japan unless you close the entire office. oops!

Banking regulation is designing employment creation plans for overeducation populations, which is a global issue. They are overeducated in nonsense, not on what is actually important. They are just high-paying checkboxers. While bank executives are tempted to cut their workforce by 99% and increase productivity as a regulated agency, they can’t do it.

Stablecoins will eventually be adopted in limited form in traditional banks. They will run two parallel systems, the old slow and expensive system, and the new fast and cheap system. To what extent they are allowed to truly embrace stablecoins will be decided by prudent regulators in each office. Remember that JPMorgan is not an organism, but that JPMorgan instances in each country are subject to different regulation. Data and people are often not shared among instances, which hinders company-wide technology-driven rationalization. Good luck, bastard bankers, regulation protects you from the shock of Web2, but will confirm that you die in Web3.

These banks certainly won’t cooperate with third parties in technology development or stablecoin distribution. All of this they will do internally. In fact, regulators may explicitly prohibit cooperation. Therefore, for entrepreneurs who have established their own stablecoin technology, this distribution channel is closed. I don't care how much proof of concept a particular issuer claims is being conducted for traditional banks. They will never lead to bank-wide adoption. So if you are an investor, if stablecoin issuer promoters claim they will work with traditional banks to bring their products to market, run away quickly.

Now that you understand the difficulties new entrants face in getting mass distribution for their stablecoins, let's discuss why they're going to try this impossible anyway. Because being a stablecoin issuer is extremely profitable.

USD interest rate game

The profitability of a stablecoin issuer depends on the amount of available net interest income (NIM). The issuer's cost basis is the fees paid to the holder, and the income comes from the returns of cash invested in Treasury debt (such as Tether and Circle) or some kind of cryptocurrency market arbitrage (such as spot holding arbitrage transactions, such as Ethena). The most profitable issuer, Tether, does not pay any fees to USDT holders or depositors and earns all NIM based on the yield level of short-term Treasury bills (T-bills).

Tether is able to retain its entire NIM because it has the strongest network effect and its customers have no alternative to other U.S. dollar bank accounts. Potential customers won't choose other dollar stablecoins, as USDT is accepted throughout the global South. A personal example is how I pay for my ski season in Argentina. I ski in the Argentina countryside for a few weeks each year. When I first went to Argentina in 2018, payment would be a hassle if the supplier did not accept foreign credit cards. But by 2023, USDT took over and my guide, driver and chef all accepted USDT as a payment. This is great because I can’t pay with pesos even if I think; bank ATMs only offer up to $30 equivalent pesos per transaction, and charge a 30% handling fee. It's a fucking crime - long live Tether. It’s great for my employees to receive digital dollars stored in cryptocurrency exchanges or their mobile wallets and can be easily used to purchase domestic and international goods and services.

Tether's profitability is the best advertising for social media companies and banks to create their own stablecoins. Neither category has to pay for deposits, as they already have a rock-solid distribution network, meaning they capture all NIMs. Therefore, this could become their huge profit center.

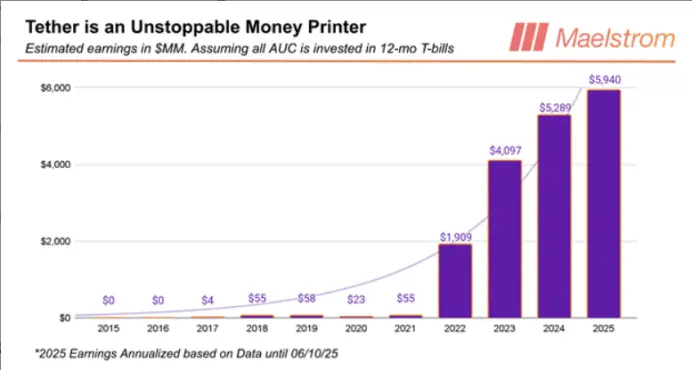

Tether makes more money every year than this chart estimates. This figure assumes that all AUCs (Assets Managed) are invested in twelve-month short-term Treasury bills. The point is to show that Tether's earnings are highly correlated with U.S. interest rates. You can see a huge jump in earnings from 2021 to 2022, as the Fed raises interest rates at its fastest pace since the early 1980s.

This is a table I posted in the article Dust on Crust Part Deux, which uses 2023 data to clearly show that Tether is the world's highest profitable bank.

Distribution of stablecoins can be very expensive unless you are affiliated with a proprietary exchange, social media company, or traditional bank. The founders of Bitfinex and Tether are the same group. Bitfinex has millions of customers, so out of the box, Tether has millions of customers. Tether does not have to pay for distribution because it is partly owned by Bitfinex and all altcoins are traded with USDT.

Circle and any other stablecoins that appear thereafter must pay distribution fees to the exchange in some form. Social media companies and banks will never work with third parties to build and operate their stablecoins; therefore, cryptocurrency exchanges are the only option.

Cryptocurrency exchanges can build their own stablecoins, just like Binance tries to BUSD, but in the end many exchanges think building a payment network is too difficult and distracting from their core business. The exchange requires the issuer's equity or part of the issuer's NIM before it can be allowed to trade its stablecoins.

But even so, all cryptocurrency/USD pairs are likely to be paired with USDT, which means Tether will continue to dominate the market. That's why Circle had to please Coinbase. Coinbase is the only major exchange not on the Tether track, as Coinbase’s clients are primarily Americans and Western Europeans.

Before U.S. Commerce Secretary Howard Lutnik favored Tether and provided banking services to him through his company Cantor Fitzgerald, Tether had been slammed by Western media as some kind of foreign-made scam. The existence of Coinbase relies on the favor of American political institutions, and it must find an alternative. So Jeremy Allaire posed and accepted Brian Armstrong's request.

The deal goes like this: Circle pays 50% of its net interest income to Coinbase in exchange for distribution throughout the Coinbase network. Yachtzee is available! !

The situation for new stablecoin issuers is very serious. There is no open distribution channel. All major cryptocurrency exchanges either own issuers or work with existing issuers Tether, Circle and Ethena. Social media companies and banks will build their own solutions.

Therefore, a new issuer must transfer a considerable portion of its NIM to depositors in an attempt to pry them out of other stablecoins with higher adoption. Ultimately, that's why at the end of this cycle, investors lose money on almost every publicly listed stablecoin issuer or technology provider. But that won't stop the party from going on; let's dive into why investors' judgment is blinded by the huge profit potential of stablecoins.

Narrative has three business models that are responsible for creating cryptocurrency wealth beyond merely holding Bitcoin and other altcoins. They are mining, operating exchanges and issuing stablecoins. In my own example, my wealth comes from BitMEX (a derivatives exchange) I own, and Maelstrom (my family office) has the largest position and the asset that produces the most absolute returns is Ethena, the issuer of USDE stablecoins. Ethena has grown from zero to the third largest stablecoin in less than a year in 2024.

The unique feature of the stablecoin narrative is that it has the largest and most obvious total addressable market (TAM) for traditional finance (TradFi) fools.

Tether has proven that an on-chain bank that simply holds people’s funds and allows them to move back and forth can become the highest profitable financial institution ever. Tether succeeded in the face of legal battles initiated by governments at all levels of the United States.

What would happen if U.S. authorities at least were not hostile to stablecoins and allowed them to have some freedom of operation when competing with traditional banks in terms of securing deposits? Profit potential is crazy.

Now considering the current setup, U.S. Treasury staff believe the stablecoin AUC (assets managed) could grow to $2 trillion. They also believe that the dollar stablecoins may be the tip of advancing/maintaining the dollar hegemony, and are also buyers who are insensitive to the price of Treasury debt.

Wow, this is a major macro tailwind. As a delicious reward, remember that Trump has grudges against big banks because they disqualified him and his family from the platform after his first presidency. He has no intention of preventing the free market from providing a better, faster and safer way to hold and transfer digital dollars. Even his sons jumped into the stablecoin game.

That's why investors salivate over investable stablecoin projects. Before we continue to discuss my predictions about how this narrative will translate into a money burning opportunity, let me define the criteria for investable projects.

The issuer in question can be listed in some form on the U.S. public stock market. Secondly, the publisher offers products with mobile digital dollars; don't have that kind of foreign shit, this is "Murica". That's all, as you can see, there are a lot of blank spaces to get creative.

The most obvious publisher to the road to destruction is to IPO and start a party is Circle. They are an American company and are the second largest stablecoin issuer by AUC.

Circle is seriously overestimated at this stage. Remember Circle gave 50% of its interest income to Coinbase. However, Circle's market value is 39% of Coinbase. Coinbase is a one-stop cryptocurrency finance store with multiple profitable business lines and tens of millions of customers around the world. Circle is good at fellatio, and while it is a very valuable skill, they still need to improve their skills and take care of their stepsons.

Should you short Circle? Absolutely not! Maybe if you think the Circle/Coinbase ratio is unreasonable, you should buy Coinbase. Although Circle is overvalued, when we look back on the stablecoin fanatic a few years later, many investors will expect them to just hold Circle. At least they can still have some capital left.

The next wave of listing will be the imitator of Circle. Relatively speaking, these stocks are more overvalued than Circle in price/AUC ratio. Absolutely, they can never surpass Circle in revenue generation.

Promoters will boast of meaningless traditional financial qualifications, trying to convince investors that they have the relationship and ability to subvert traditional banks’ position in the global dollar payments space by working with them or leveraging their distribution channels. The scam will succeed; the publisher will raise a lot of fucking money. For those of us who have been in the trenches for a while, it would be hilarious to watch those clowns in suits and ties trick the public into investing in their shit companies.

After this first wave, the scale of the scam depends entirely on the US's stablecoin regulatory regulations. The greater the freedom issuer has in supporting stablecoins assets and whether or not it can pay benefits to holders, the more financial engineering and leverage it can be used to cover up shit. If you assume a light or contactless stablecoin regulation, you might see a repeat of Terra/Luna, where a certain issuer creates some sort of scam-free algorithmic stablecoin Ponzi scheme. Issuers can pay high returns to holders, which come from applying leverage to certain assets.

As you can see, I have relatively little to say about the future. There is no real future because the distribution channels of new entrants are closed. Dispel this idea.

But don't short. These new stocks will make shorts lose all their money. The macroscopic and microscopic are synchronized. As Chuck Prince, former Citibank CEO, said when asked if his company was involved in subprime mortgages: "When the music stops, things get complicated when it comes to liquidity. But as long as the music is still playing, you have to get up and dance. We are still dancing."

我不确定Maelstrom 会如何跳舞,但如果有钱可赚,我们就会去赚。